Moody’s Investors Service has released its housing affordability report on Australia, which revealed that affordability in the two major capitals – Sydney and Melbourne – has deteriorated despite lower interest rates, although the picture nationally is unchanged. The outlook for Sydney purchases is also dire:

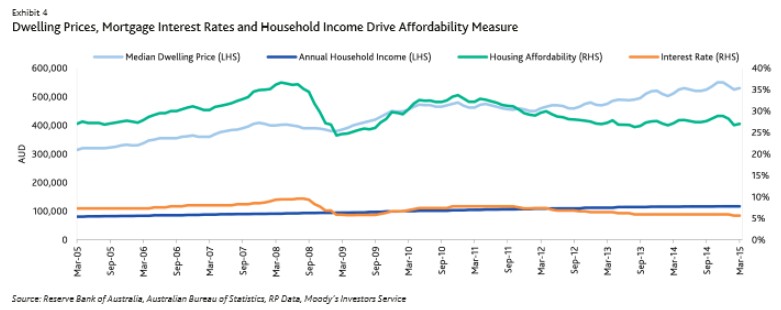

Moody’s Australian Housing Affordability Measure — which measures the share of income needed, on average, to make monthly mortgage loan repayments – was steady on the national level over the year to 31 March 2015. However, the measure deteriorated for Sydney and Melbourne, Australia’s two biggest cities.

Nationally, Australian households with two income earners needed, on average, 27% of household income to make mortgage loan repayments as of 31 March 2015, unchanged from March 2014 (Exhibit 1). At the national level, low mortgage interest rates — after the Reserve Bank of Australia’s (RBA) cut the official cash rate by 25 basis points to a record low 2.25% in February 2015 — helped to offset rising house prices and relatively flat income levels.

In Sydney, however, Moody’s Australian Housing Affordability Measure deteriorated to 35.1% as of 31 March 2015, from 32.8% in

March 2014. Median dwelling prices in Sydney rose 11.7% over the year to 31 March 2015 (Exhibit 2). The affordability measure for Melbourne also deteriorated, to 28.2% as of 31 March 2015 from 27.5% in March 2014. A higher affordability measure indicates a higher proportion of household income is needed to make monthly mortgage repayments.

On the other hand, the affordability measure improved significantly over the year in Perth, to 21.9% from 24.6%. Median dwelling prices in Perth – where the economy is exposed to significant declines in prices for key commodities, such as iron ore – declined by 4.8% in the year to 31 March 2015. Affordability also improved in Brisbane, to 23.4% from 24.4%, over the year, while it was steady in Adelaide at 22.1%…

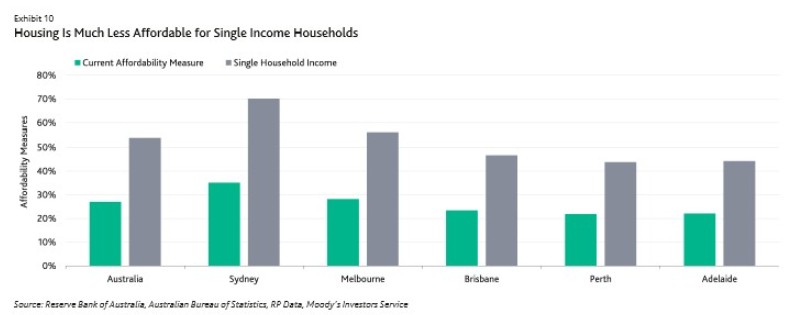

Moody’s Australian Housing Affordability Measure is calculated assuming a household has two income earners. If the household has only one income earner, Sydney’s affordability measure would be above 70%. Using 70% of income to service monthly mortgage repayments is not sustainable…If we use post-tax — instead of pre-tax income — to calculate monthly average household income, the Moody’s Housing Affordability Measure would be 6 percentage points higher on a national basis. And the affordability measure for Sydney would increase — that is deteriorate — the most (+7.8 percentage points), while the measure for Adelaide would increase the least (+ 4.6 percentage points).

It is worth pointing out that Moody’s housing affordability measure for Australia fundamentally differs from the way that it measures affordability in the US.

Advertisement

As noted above, Moody’s measures measures affordability in Australia by assuming a household has two income earners and counts pre-tax income only. This compares to the way it measures housing affordability in the US, whereby it assumes a medium family income, which is obviously much lower than assuming two income households.

Why Moody’s has chosen to present affordability in a more favourable light in Australia than really exists is curious.

In any event, a typical single income earner has virtually no chance of purchasing a home in Sydney, since the buyer would need to sacrifice 70% of pre-tax earnings to cover their mortgage – a virtual impossibility. Here’s a chart from Moody’s showing how hard it is for a single earner households to purchase a home across Australia:

Advertisement

In short, Sydney housing affordability sucks despite record low mortgage rates.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.