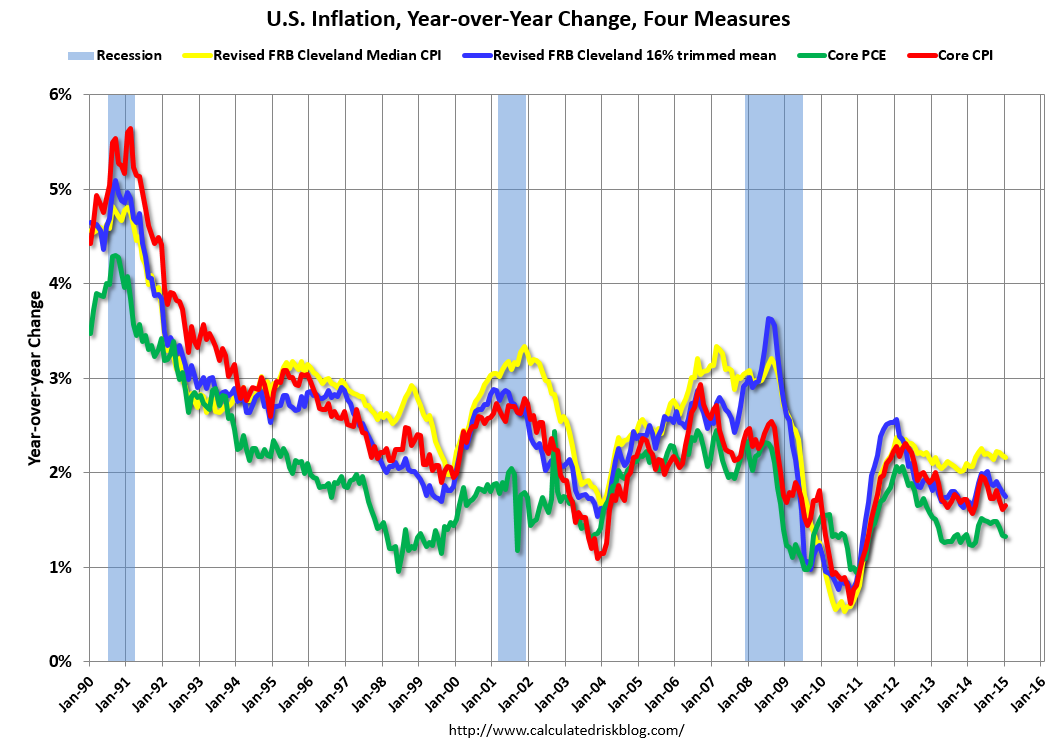

Markets appeared to take fright at US inflation Friday night but for no obvious reason. Headline CPI is above the Fed’s target but has been for months. More significant are the analytical measures, from the Cleveland Fed (chart from Calculated Risk):

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.6% annualized rate) in March. The 16% trimmed-mean Consumer Price Index also rose 0.2% (2.2% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report.

Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers rose 0.2% (2.9% annualized rate) in March. The CPI less food and energy also rose 0.2% (2.8% annualized rate) on a seasonally adjusted basis.

The median CPI is above the Fed’s 2% ceiling and core and trimmed mean had a firmer month but are hardly tearing the roof off. The Fed’s preferred measure is the PCI in green, which is chronically weak.

Stocks were pounded and short end bonds sold but the long end rallied and the US dollar hardly moved. I go with the latter. There is nothing here to bring forward rate hikes.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.