By Lindsay David, cross-posted from the Australia: Boom to Bust Blog

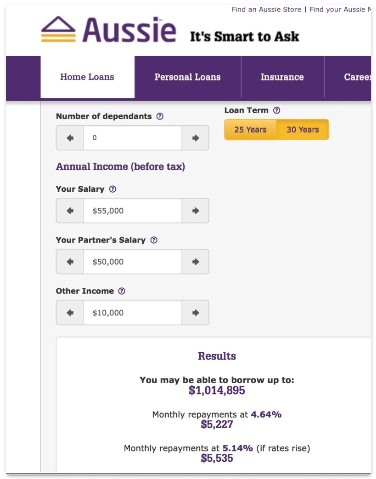

Ever been on an Australian home lenders website and tested their ‘how much can I borrow’ calculator? Aussie Home Loans seems fine lending $1.014 million to a household with a “pre tax” income of $115,000 (or almost 9x income).

Image source (www.aussie.com.au)

Aussie may want to consider changing its online calculator to measuring how much a homebuyer can borrow based on ‘after tax income’ to be able to give adequate buffers for homebuyers to not get themselves in a horrible financial situation should there be a job loss.

According to taxcalc.com.au, net income after tax for the hypothetical couples (as per the image above) $55,000 and $50,000 income would be $44,736 and $41,356 respectively. Plus adding $10,000 of other income, that would total $96,272 per year or $8,022 per month. This would mean relative to net income after tax, the homebuyer household would hold a loan more than 10x its annual income.

Now you don’t need to be a brain surgeon to know if one of the joint owners of a $1.014 million loan lose their job– they will earn less in income than what the monthly repayments would be. In the meantime, the hypothetical couple would be left with $2,749 per month to cover the bills and all other living expenses whilst both hold their jobs. Based on Australia’s high cost of living, I guess that means no vacation for a very long time.

The more Australian’s that get tied up into this national household debt ponzi, the harder it will be for the Australian economy to eventually recover from a severe downturn in the housing market. Not that our regulators over at APRA seem too concerned. It’s time for APRA to properly regulate how much a household can borrow relative to their net income after tax, not just the deposit.