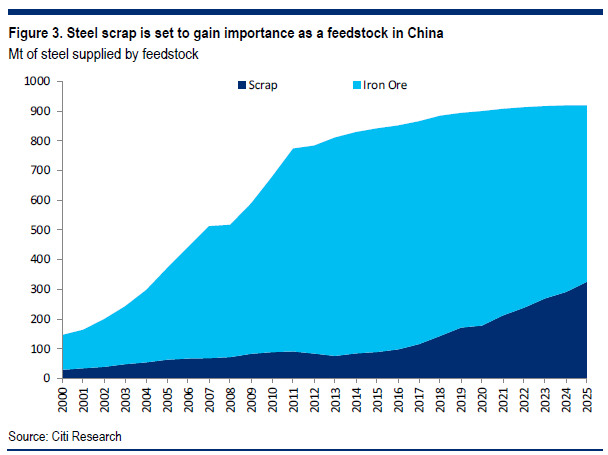

The long-term threat of steel scrap to Chinese iron ore demand remains underestimated, and this point was the greatest area of pushback from last year’s iron ore book (Global Iron Ore – Vive La Différence!). However, as Chinese steel demand has slowed even faster than forecast, the medium and longer term threat posed by scrap to iron ore demand has actually increased.

China’s scrap ratio is currently only around 10%, compared with around 60% in the rest of the world. However, the availability of scrap in China is increasing rapidly, as the material used during the rapid growth in consumption of machinery, autos and appliances in early 2000s, is converted to scrap. Moreover, the government is encouraging setting up of collection centers, and though the government cancelled tax exemption for steel scrap recycling in 2011, we expect supportive policies in the future.

While low iron ore prices encourage continued iron ore usage, they also put downward pressure on scrap prices. Moreover, although low steel prices will make some recycling uneconomic, leading to low recovery rates, scrap usage will nevertheless grow substantially. At the same time, with steel production growth having slowed, the proportion of scrap in raw material feed is likely to rise significantly.

Initially this growth in scrap supply is expected to come via greater usage by BoF based steel plants, but in the 2020s we also expect increasing numbers of EAF steel mills to be built.

Another feather in the Citi cap. This is the first time I’ve seen a sensible measure of the rise of steel scrap usage in China to meet that of MB. It’s actually a little more aggressive than the MB outlook. We see 300mt tonnes of scrap in 2030. Having said that, the anti-pollution push is likely to push arc-furnaces especially.

The Citi outlook is bearish enough but take a moment to consider if the forecasts of Professor Ross Garnaut and Chinese steel researchers are met. They see 700mt tonnes in total steel production output by 2030. If 300mt tonnes of that comes from scrap and China preserves 200mt of iron ore mining capacity (equal to 130mt of steel) then total import demand for iron ore will be…wait for it…around 400mt. That is, roughly 40% of last year!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.