It has been amazing watching the transformation of Shane Oliver, chief economist of AMP, over the past seven years.

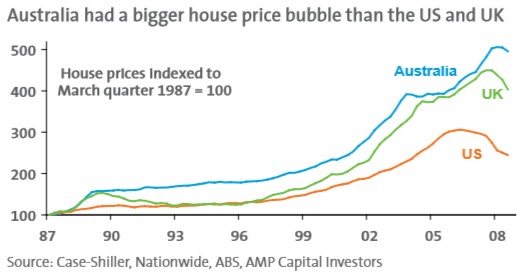

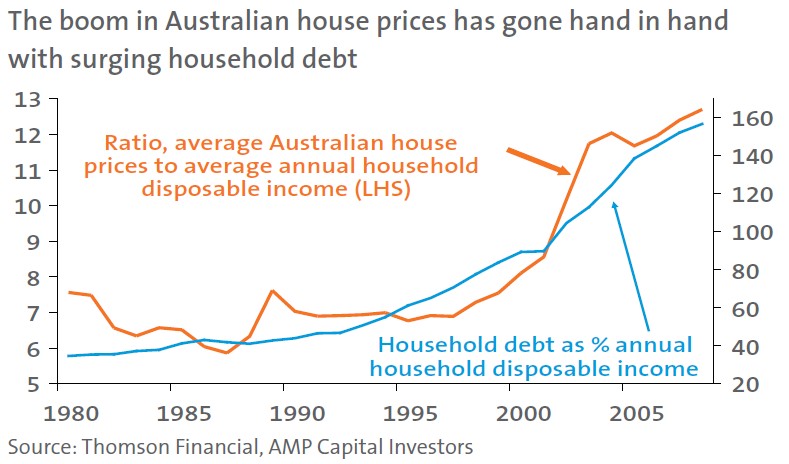

In 2008, Oliver released well-argued research arguing that Australian housing was a “bubble”, and that the combination of excessive housing debt and inflated housing values were Australia’s “Achilles heel” (see below charts).

Since that time, however, Oliver has taken an opposing view, going to great pains to argue why Australian housing is not a bubble, despite valuations and debt levels being even worse today.

Oliver has even argued against changes to housing taxes, claiming that they would be viewed as “unAustralian” and, in the case of negative gearing, might even be undesirable, repeating the lie that it would push-up rents:

It is unlikely the government would move on negative gearing, Mr Oliver says, and he was not convinced it would be a good idea given the backlash Paul Keating suffered when he tried to do it in the 1980s.

“Last time it happened, investor interest dissipated overnight and rental rates started to shoot up [in some capital cities],” he says.

As noted earlier by Houses & Holes, Oliver is at it again, today defending the bubble once more:

Of the warnings, AMP Capital senior economist Shane Oliver says he’s “heard it all before”. Although he agrees that house price ratios to rents and GDP are “very high” – “I wouldn’t say grossly” – he says the Australian housing market is “significantly undersupplied”.

There have been imminent crashes coming since 2003. “Despite warnings of a crash around the corner – or a bloodbath – it hasn’t happened and it probably won’t.

“Regulators keep a close eye on the banks and they’re tightening things up right now.

“There’d need to be a spike in unemployment – you’d have to get forced selling and it’s hard to see forced selling on large scale in Australia, particularly with Australians ahead on their loans.

“We’ve got record low interest rates – you might expect every city would be booming, but only Sydney is.

“It’s not as if Australians are wheeling the ATM into their homes and withdrawing … they’re being quite restrained. I can’t see a bloodbath,” Mr Oliver said.

One has to ask Shane the question: if Australian housing was a “bubble” in 2008, then why isn’t it now?

- Mortgage debt levels are currently at record highs against incomes and GDP.

- House prices currently are at record high levels, and continue to shoot higher against incomes.

- Investor participation is currently at all time highs.

- Rental growth is at decade lows and still falling.

- Income growth is currently at record low levels.

- Population growth is falling just as dwelling construction booms.

I should also mention that the economy is facing its biggest structural adjustment since the early-1990s recession, given the massive unwinding of the mining capex boom and the closure of the automotive industry in 2017.

How is this situation in any way sustainable and not indicative of a housing bubble?