From Morgan Stanley:

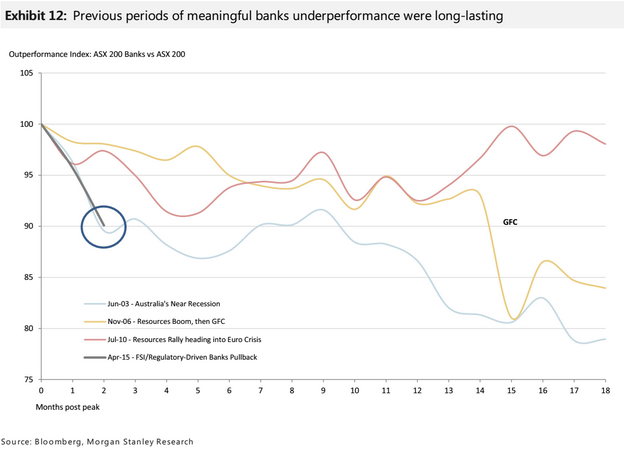

Banks – After The Fall? The Australian Banks sector has underperformed the ASX 200 over thelast two months by ~10% as higher capital and tighter regulation seeearnings and dividend profiles flatten.Whileyield remains a support, weremain cautious with an UW sector bias: not only does capital/regulation remain a longer term issue but consensus earnings outlook fails to carry any slack should theeconomic backdrop deteriorate.

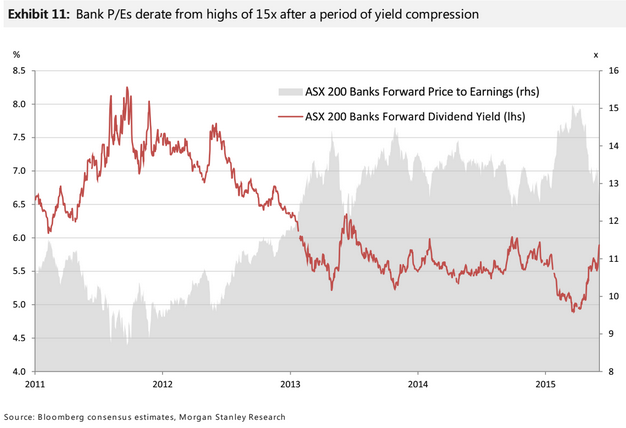

The recent re-rating has really only reversed the bounce from the last few rate cuts:

So, are the banks in for a sustained period of under-performance? The only factor in the bank’s favour is more rate cuts, again boosting the yield trade, so I would not count them out yet (not least because it is the single most important valuation driver). But MS’s reasons are a pretty compelling description for why they’ve seen their peaks for the cycle:

There’s plenty of time to climb into the great Australian bank short that is ahead. Lot’s of hedgies, for instance, wait for share prices to really roll over before they pile in. Others accumulate a strategic position on spikes.

Either way, what was a near perfect environment for high bank valuations over the past few years has soured materially.