Chris Weston, Chief Market Strategist at IG Markets

With all the talk of a bubble in the Australian housing market I thought it would interesting to look at it through the eyes of an overseas investor.

When one looks at price outside of the traditional base currency it adds a whole new dimension to the market.

We know overseas money has been increasingly making its way into the Australian housing market, with figures of 15% of the national housing supply being purchased by Chinese investors alone in 2014. It won’t surprise anyone then that the bulk of those purchases have been centred on the Melbourne and Sydney markets, with estimates of closer to 25% of supply being purchased (Source: Credit Suisse).

Focusing solely on Chinese investors; we are seeing a huge shift to diversify and re-allocate the domestic household portfolio. We have already seen Chinese investors lift their exposure to Chinese equities to around 20%, from around 5% at the trough in 2005, of total assets – assisted by a government and central bank keen to push the stock market higher (through a raft of market friendly initiatives) in a bid to increase the real wealth effect and I would not be surprised to see this percentage closer to 30% in the next two years. Investments in deposits have traditionally held a 60% weighting within the average Chinese household portfolio, but this figure should be closer to and even below 50% in 2016. Chinese investors want returns, and deposits providing even an 8-9% yield don’t cut it these days.

Property investment has always commanded a keen interest, so it’s interesting that we are now hearing of investors taking profits in the domestic equity market after the sensational move higher and using the profits to buy property again in tier 1 cities. This is being supported by increasing signs of stability in housing, with residential sales value data improving 30.4% y-y in May from 16.0% in April. However, as we have seen since 2013 there is also a keen interest for geographical diversification with the Sydney and Melbourne property markets favoured.

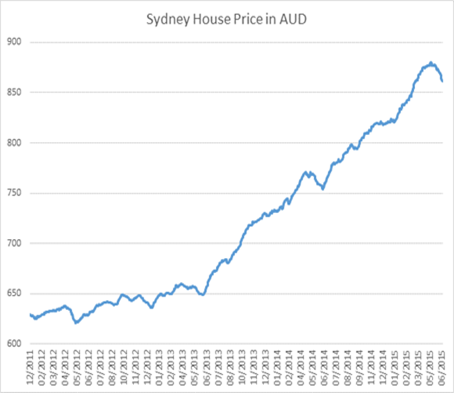

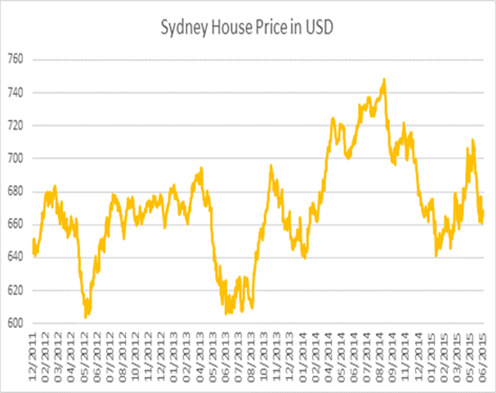

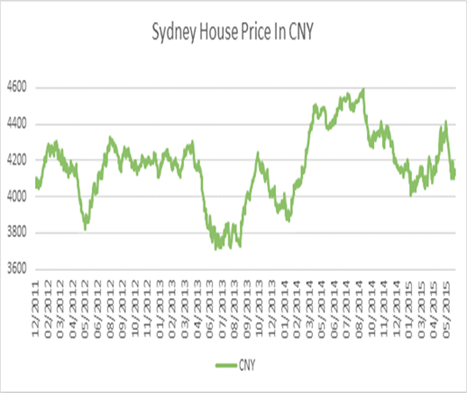

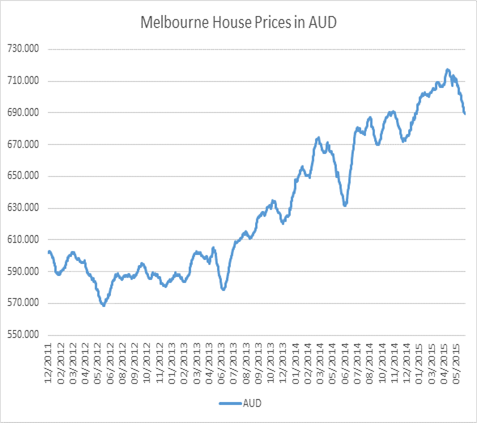

If we look at property prices then in AUD terms (see below charts) one can clearly see the rampant trend higher since late 2012, which supports the arguments of those who believe markets like Sydney have ‘bubble’ like qualities. However, when adjusting price into US dollars or Chinese yuan and looking at the adjusted prices through the eyes of an unhedged investor you can see that things don’t look so frothy. Of course, this doesn’t take into consideration variables such as price-to-income ratios or other affordability measures, but it does show that either foreign investors feel there is strong upside to the AUD, or that capital appreciation of the property will outweigh any FX exposure.

Hedging solution

One way Chinese investors could look at hedging their exposure is through AUD/CNH spot contracts. I’ve looked at offshore yuan (CNH) given the capital controls in China, however the 30-day correlation between AUD/CNY and AUD/CNH is currently 99.7%, so effectively there is little difference for the hedge.

There is a charge for holding the position overnight, but this is a market-related charge based on interest rate differentials. Still, over the last two years an investor who would have purchased an A$1 million property in Melbourne and chosen to hedge the position would have paid around A$12,000 in funding charges (based on current interest rate differentials). However, they would have made around A$210,000 on the currency trade, given moves lower in AUD/CNH in the last two years. In this regard the investor would have seen a net benefit of around A$198,000.

Sydney house prices in AUD, USD and CNY since 2012

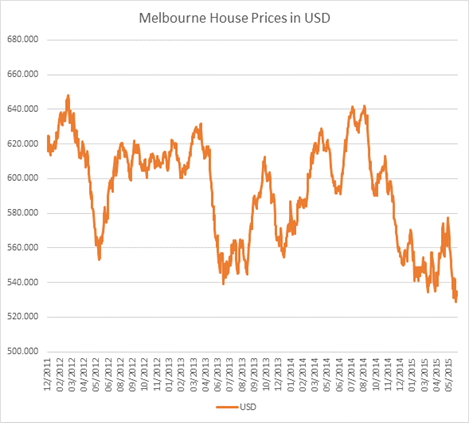

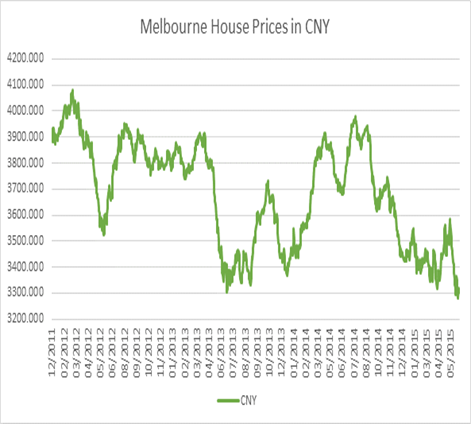

Melbourne house prices in AUD, USD and CNY since 2012

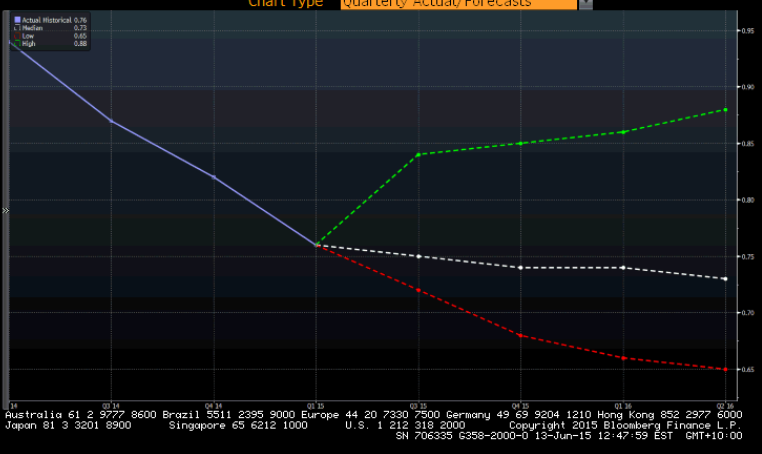

My personal view is Chinese buyers are generally quite bullish on the AUD, although the geographical diversification is an interesting component. Having recently been to Shanghai, Hangzhou and Beijing the majority of traders I spoke to felt AUD/USD and AUD/CNY would bounce from current levels after a strong fall over the last four years. This view is in contrast to my own and the consensus who believe AUD/USD (I’ve looked at AUD/USD due to the limited number of AUD/CNY forecasts) should be closer to $0.7300 by mid-2016. One investment house even has $0.6500 as its base case, a level some 8% below the AUD’s post float average. Taking this view out by a further six months and Morgan Stanley, for example, are even forecasting we could see $0.6200 by year end – not great when house price momentum (in all G10 currencies except NZD) is waning.

(Bloomberg chart showing AUD/USD forecasts – the white line is the median forecast)

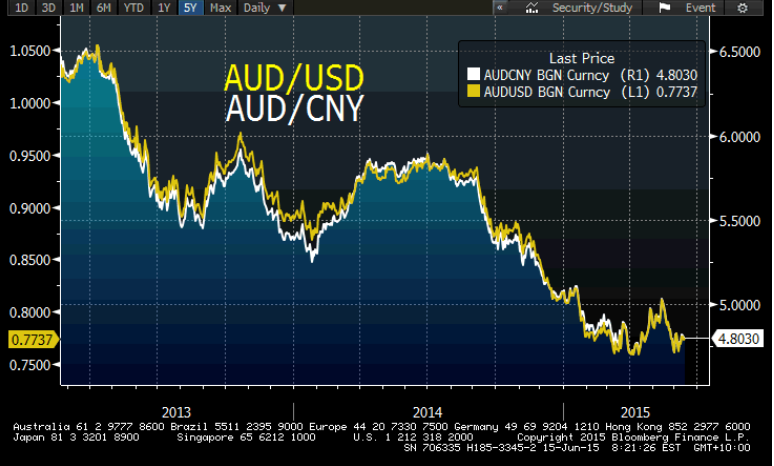

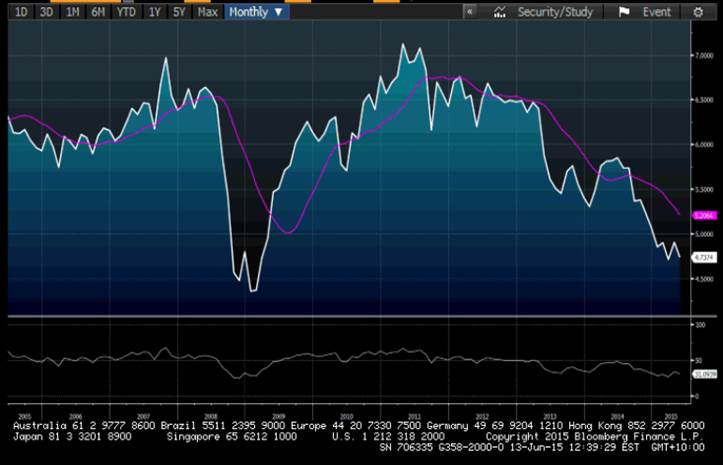

In my opinion there is a high probability is that we see the PBoC maintaining stability in USD/CNY over the coming 12-months, despite some huge catalysts such as Fed normalising policy and a potential inclusion of the CNY into the IMF’s Special Drawing Rights basket (SDR). However, as detailed I feel AUD/USD and AUD/CNY will naturally be very closely correlated (see Bloomberg chart below).

If we look at AUD/CNY, it’s fairly clear judging from the longer-term monthly chart that the trend is down and using regression analysis we can see even at spot prices the pair is not yet even one full standard deviation from the mean. The trend, as they say is your friend and while none of the traditional oversold readings are flashing red it doesn’t really feed into a view that the AUD/CNY (or AUD/USD) is ‘cheap’ or due for a technical bounce. This should be a major consideration for those exposed to a weakening AUD, which according to Credit Suisse is growing by the day with estimates of a further $60 billion in further purchases of Aussie real estate from Chinese investors over the coming six years.

Looking at Melbourne property prices adjusted for the strength in USD or CNY, one can see that property prices are actually at multi-year lows.

Taking price in isolation it isn’t thematic of a ‘bubble’ from an overseas perceptive and if you had a nominal AUD exposure you would have potentially even lost money. Of course most don’t buy a property with a two-year view in mind so there are clearly going to be many gyrations in the currency markets over the years, especially when the Reserve Bank of Australia come to raising rates. However, these charts do prove that having an ability to mitigate the negative effects in the currency market can by hugely beneficial.

What percentage of foreign investors are choosing to hedge investments is unclear, but one would suspect it is very low, with only the sophisticated or wealthy looking to do so. Still, this is something that should get more focus especially if the AUD really does catch up with the terms of trade.

IG offer the pair for a 25 point spread, relative to many of the local banks who will offer for a market spread well in excess of 500 pips.