A journalist friend has today informed me that Dr Tulip was also the author of an RBA research paper, released in December 2014, which argued that the mining boom boosted real per capita household disposable income by 13% over the decade to 2013, with positive impacts on housing:

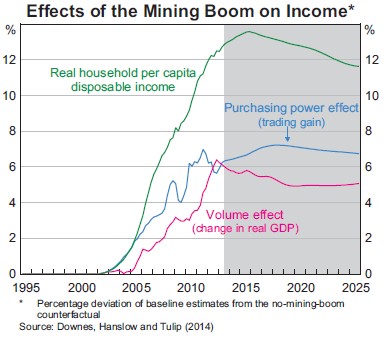

The world price of Australia’s mining exports more than tripled over the 10 years to 2012, while investment spending by the mining sector increased from 2 per cent of GDP to 8 per cent. This ‘mining boom’ represents one of the largest shocks to the Australian economy in generations…

The effect of the mining boom on overall living standards can be gauged by the difference in real household disposable income per capita, which is estimated to have been about 13 per cent higher in 2013 than it would have been without the boom…

The increase in household disposable income has involved a surge in demand for housing. However, whereas most other elements of consumption are supplied elastically, the supply of housing is relatively fixed in the short run. Thus, the mining boom results in a substantial reduction in vacancy rates and an increase in rents…

Here’s a question for Dr Tulip: given that the mining boom juiced household incomes by 13%, what does he think will happen to household incomes now that the mining investment boom is unraveling and commodity prices and the terms-of-trade are crashing?

Shouldn’t the stiff headwinds facing household incomes – which will likely result in zero real growth for the foreseeable future – also be factored into his model, thereby lowering expected house price appreciation and making Australian homes overvalued?