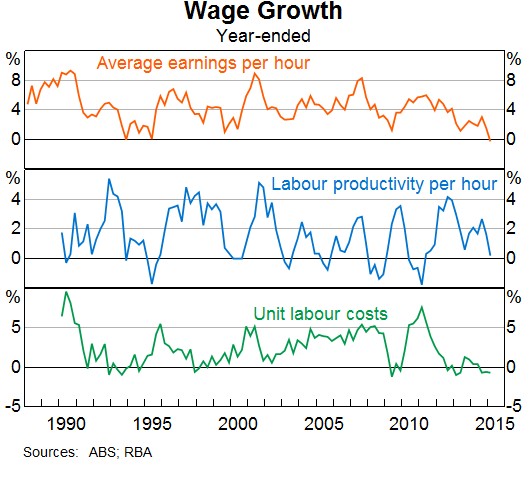

The behaviour of wages during the current episode has been comparable to the experience around the 1990s recession. This is true of nominal wage growth and growth in the cost of the labour required to produce a unit of output – so-called unit labour costs. The decline in real wage growth has also been of a similar magnitude to the early 1990s.

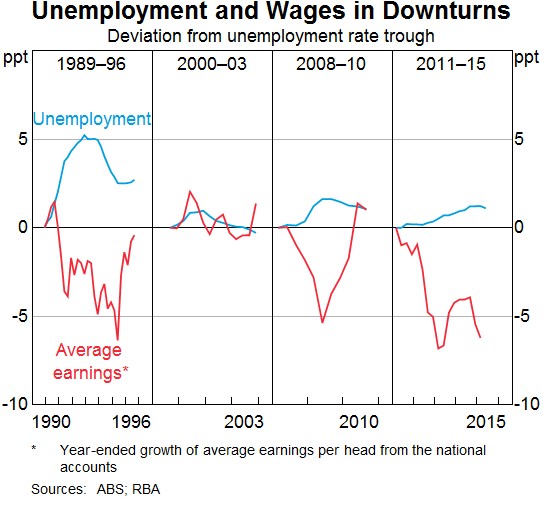

While we would normally expect wage growth to decline after a period of subdued labour demand, the decline over recent years has been larger than suggested by historical experience. In particular, although the unemployment rate has increased by much less than during the early 1990s recession, the decline in wage growth during the two episodes has been similar…

Whatever the reason for the very low growth in labour costs, wage flexibility has assisted with the labour market adjustment. Changes in relative wages act as an incentive for labour to move. Strong increases in wages in the resource sector (in both domestic and foreign currency terms) helped to attract the labour needed to undertake the substantial increase in mining investment (including from overseas). All of these things are now adjusting in the other direction… In addition, low wage growth across the economy has enabled firms to employ more labour than would otherwise have been the case.

…the low wage growth of recent years is perhaps best viewed as a response to the spare capacity that has built up in the labour market over time. If wage growth had not been so responsive, it is likely that employment would have been less and the unemployment rate higher than we’ve seen. So even though low wage growth works to constrain the growth of incomes for those who are employed, it also supports incomes by encouraging more employment than otherwise.

As I noted on Wednesday, wages growth will need to remain low for Australia to regain its competitiveness (as measured by unit labour costs above). Without such slow wages growth, trade-exposed local firms would continue to shutter, slashing employment.

Advertisement

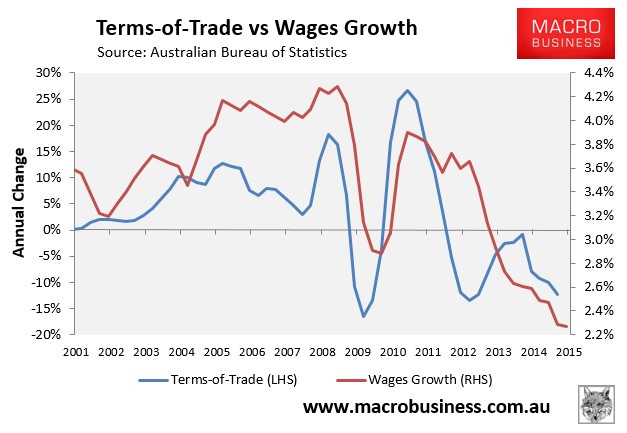

In any event, low wages growth is all but inevitable in the period ahead given the terms-of-trade is falling, and is thus dragging down nominal GDP and national disposable income:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.