Deloitte Financial services has released a new report, “Mythbusting Tax Reform” , which among other things argues that the 50% capital gains tax (CGT) discount, implemented in 1999 by the Howard Government, is too generous and has helped fuel negatively geared property investment. Deloitte, therefore, calls for reform of CGT – either by re-introducing indexing, as occurred pre-1999, or by reducing the CGT discount to, say, 33%:

Yes, negative gearing is being over-used at the moment, but that’s due to 1. Record low interest rates and easy access to credit 2. Heated property markets, and 3. Problems in taxing Australia’s capital gains. Or, in other words, negative gearing is a symptom of other things, rather than a cause of problems in its own right…

At this point you might be asking yourself an obvious question: why would losing money on something be a good investment? A loss is still a loss, isn’t it? What’s the upside in that? That’s where the discount on capital gains comes in: Among tax factors, it is the favourable treatment of capital gains that is the main culprit…

So for those who think that housing prices in Australia are still good value – and so have the potential to generate further good capital gains – negative gearing makes sense…

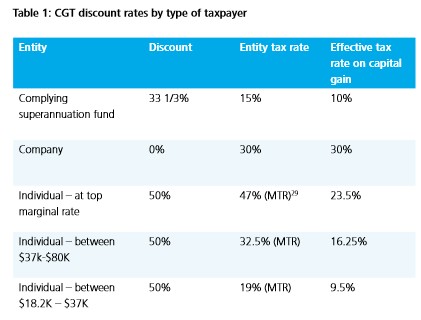

The original capital gains tax (CGT) regime adopted in 1985 allowed for inflation effects to be netted out of taxable gains, while the current system – largely still that adopted after the 1999 Ralph Review – switched instead to simply discounting the tax rates applied to capital gains. As shown in Table 1:

The basic idea is very much right. There should be more generous treatment of capital gains than of ordinary income, because that helps to encourage savings (and hence the prosperity of Australia and Australians), and because the greater time elapsed between earning income and earning a capital gain means it is important to allow for inflation in the meantime.

But we’ve got the detail wrong:

• Table 1 shows there are really big incentives for some taxpayers (such as high income earners) to earn capital gains, versus little incentive for others (such as companies)

• The discounts Australia adopted back in 1999 assumed inflation would be higher than it has been – and so they’ve been too generous.

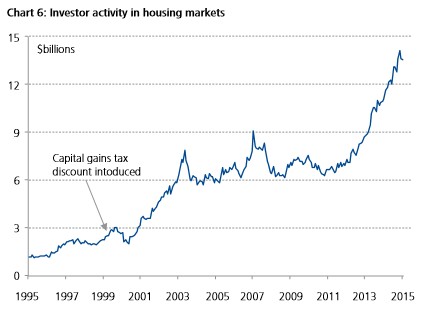

By the way, ‘overdoing it’ on the CGT discount doesn’t just come at a cost to taxpayers. It hurts the economy too. As the discount does not target particular sectors or types of assets, it provides stimulus to invest in both productive and unproductive assets. That’s part of the reason why Chart 6 shows an enormous leap in investor activity in housing markets since the discount was introduced.

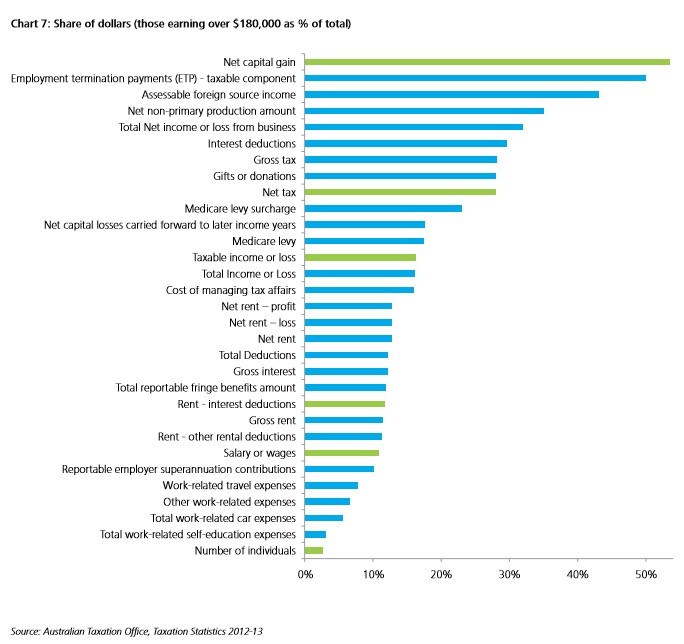

It is also part of the reason why Chart 7 shows that those who earn more than $180,000 a year account for a much bigger share of net capital gains…

So, what should we do about that?… either we go back to some form of indexing for inflation, or we cut back on the generosity of the existing tax discount…

These are just two different ways of doing the same thing. The advantage of indexation is that it rewards ‘patient capital’. But indexation can exacerbate a ‘lock in’ effect, restricting the movement of capital at a time when the wider tax reform debate wants to encourage capital to move…

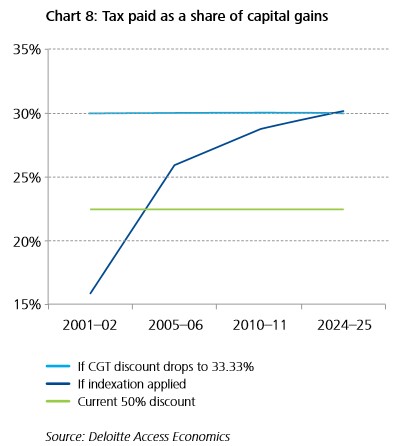

Assume an asset was bought at 30 June 2000 and that its value has grown in line with national income.

Chart 8 maps out estimates of tax paid under three alternatives – the current system, a return to an indexation regime, or moving to a smaller CGT discount:

• The current 50% discount is generous relative to the indexation option – inflation has been low, whereas capital gains have been great, so you would have to have held an asset for some years before the effective tax rates under these two alternatives equalised

• The discount could be cut to, say, 33.33%. This would ‘add back’ some of the incentive for long term rather than short term saving that low inflation has eroded. It would also help tackle the difference in tax rates applied to income and capital gains from different sources. For example, income earned from bank deposits is taxed at a person’s full marginal rate, while income earned from capital gains is taxed at half the person’s marginal rate.

Our conclusion? The current CGT discount is too generous, to the extent that it undermines the very principles of this nation’s progressive personal income tax system. It’s time for a change. Reform of the concession is long overdue.

It’s worth pointing-out that Deloitte’s conclusions are supported by the Australian Treasury, who noted the following in its Tax White Paper discussion paper:

Negative gearing does not, in itself, cause a tax distortion, but it does allow more people to enter the market than those who might have had the equity alone to do so. Purchasers can make bigger investments in property by borrowing, in addition to using their own savings. This behaviour is encouraged by the CGT discount, as larger investments can result in greater capital gains and therefore benefit more from the CGT discount.

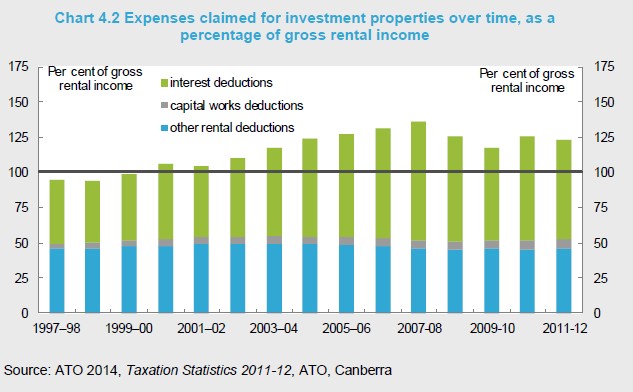

…investment properties constitute a substantial proportion of the total value of negatively geared assets. Chart 4.2 shows that deductions claimed for investment properties as a proportion of gross rental income have increased over the last 15 years and are now greater than gross rental income.

The potential tax advantage comes on the income side from the taxation of the capital gain earned from the asset. If the individual realises a capital gain when selling the property, only 50 per cent of this income is included in their taxable return.

Advertisement

Other analysis released last year by the Australian Treasury also noted that high income earners have been the main beneficiary of CGT concessions, with around half of all net capital gains income reported by those earning above $180,000:

Taxable net capital gains income tends to be received by individuals at the higher end of the income distribution. Around half of total taxable net capital gains income reported for 2011-12 was received by taxpayers whose other taxable income was above $180,000 (the top tax rate threshold). For the 2011-12 year the average statutory rate of tax on taxable net capital gains income was 30.9 per cent, compared to the overall average rate of around 22.2 per cent.

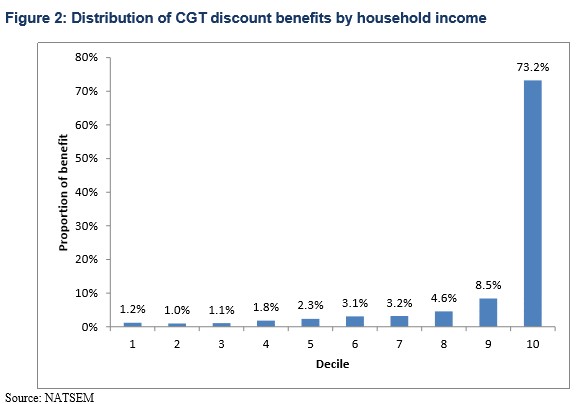

The Australia Institute has also found that nearly three quarters (73.2%) of the CGT discount went to the top 10% of income earners:

Advertisement

Finally, the Parliamentary Budget Office has estimated that cutting the CGT discount to 40% would provide a four-year Budget saving of $2.3 billion, whereas cutting the discount to 25% would save $5.7 billion over four years, and removing it altogether would save the Budget $10 billion.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.