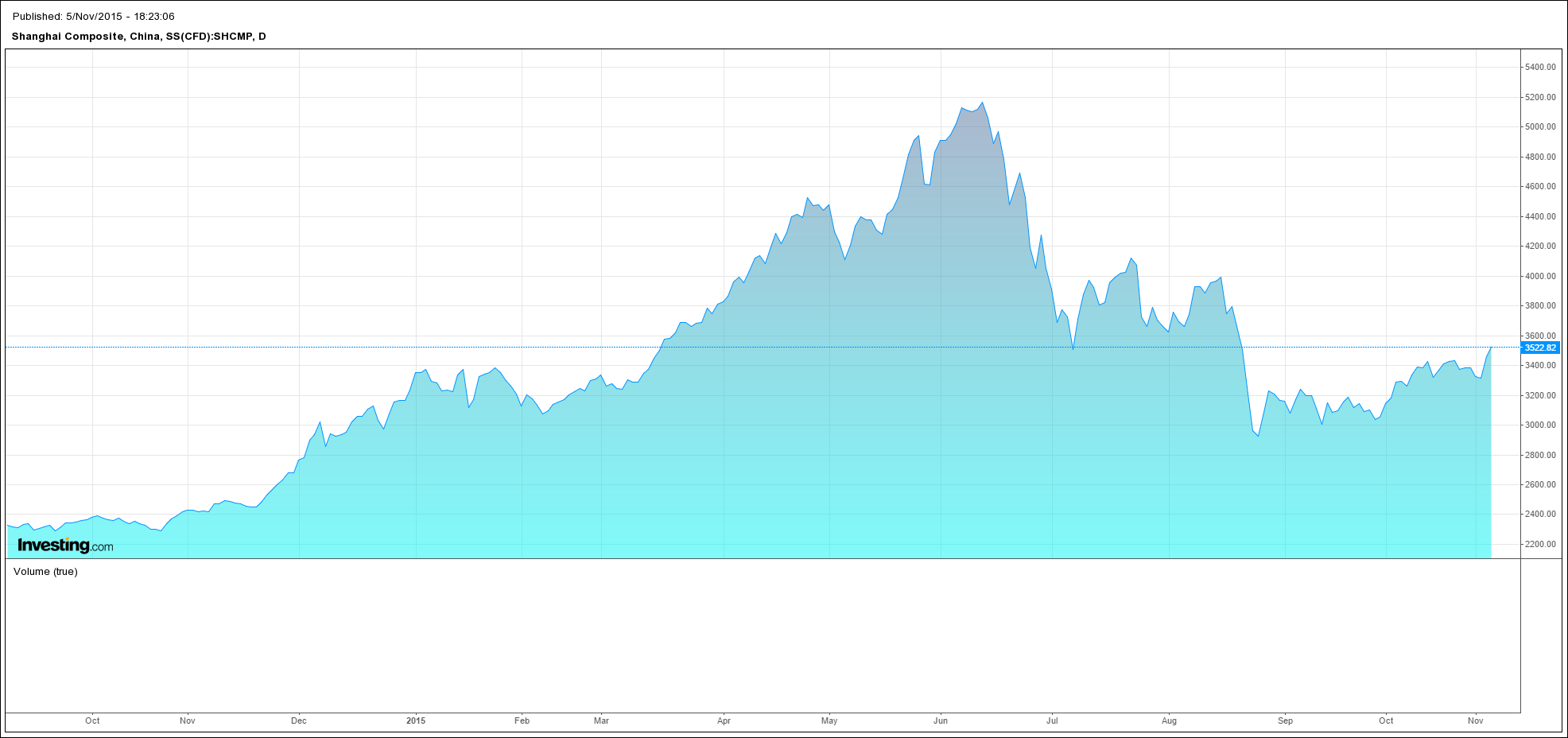

Shanghai is in new bullshit market, apparently, after rising more that 20% from its lows:

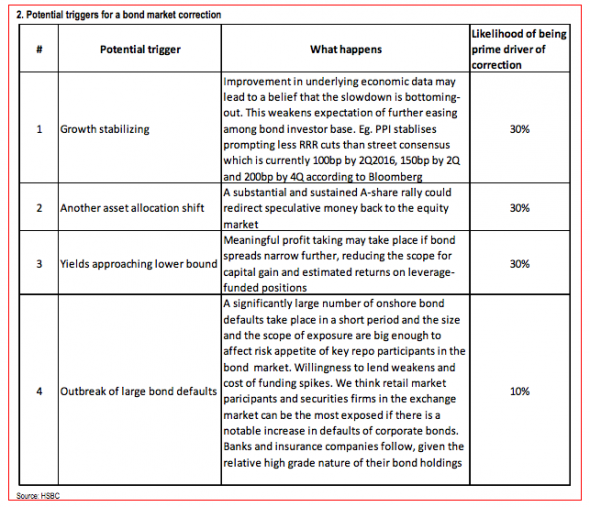

Via FTAlphaville, HSBC explores the consequences for the bond bubble “that has taken place since August is a liquidity rather than fundamental play. Hence, liquidity will have a key role in the rally’s life span”.

Following the sharp drop in the Ashare market, the government understands the painful consequences of slamming the breaks on a leverage-fuelled rally. Any sudden shock that drained liquidity may send the bond market into a correction that is bigger than expected, with ripple effects spilling over to other markets. We think the government is likely to maintain its cautious approach to default management as long as the recovery remains uncertain. Likewise, we don’t think the government will take drastic measures to clamp down on leverage-taking activities either.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.