“The options market seems to either be anticipating an inflection higher in the economic data, no rate hike, or an extreme lack of catalysts between now and year-end,” according to Goldman Sachs’ Krag Gregory. With VIX trading with a 13 handle, Gregroy warns, it is notably under-priced relative a 19 handle more in line with economic and policy uncertainty. The potential for volatility to swing higher seems more likely.

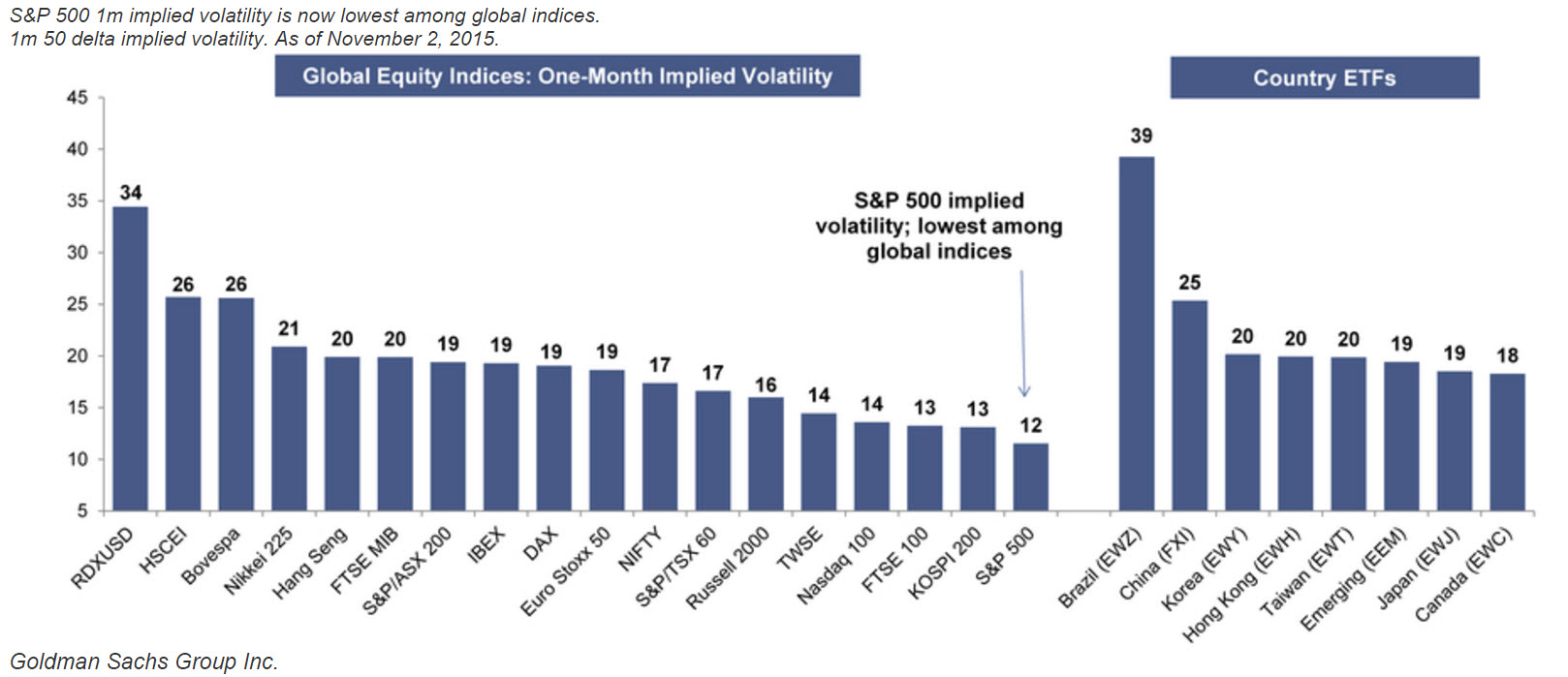

The VIX landed at 14.2 on November 2nd, back down to its average closing level during the low volatility years of 2013 and 2014.

That seems low to us given recent weakness in the U.S. economic data and a potential rate hike in December. The options market seems to either be anticipating an inflection higher in the economic data, no rate hike, or an extreme lack of catalysts between now and year-end.

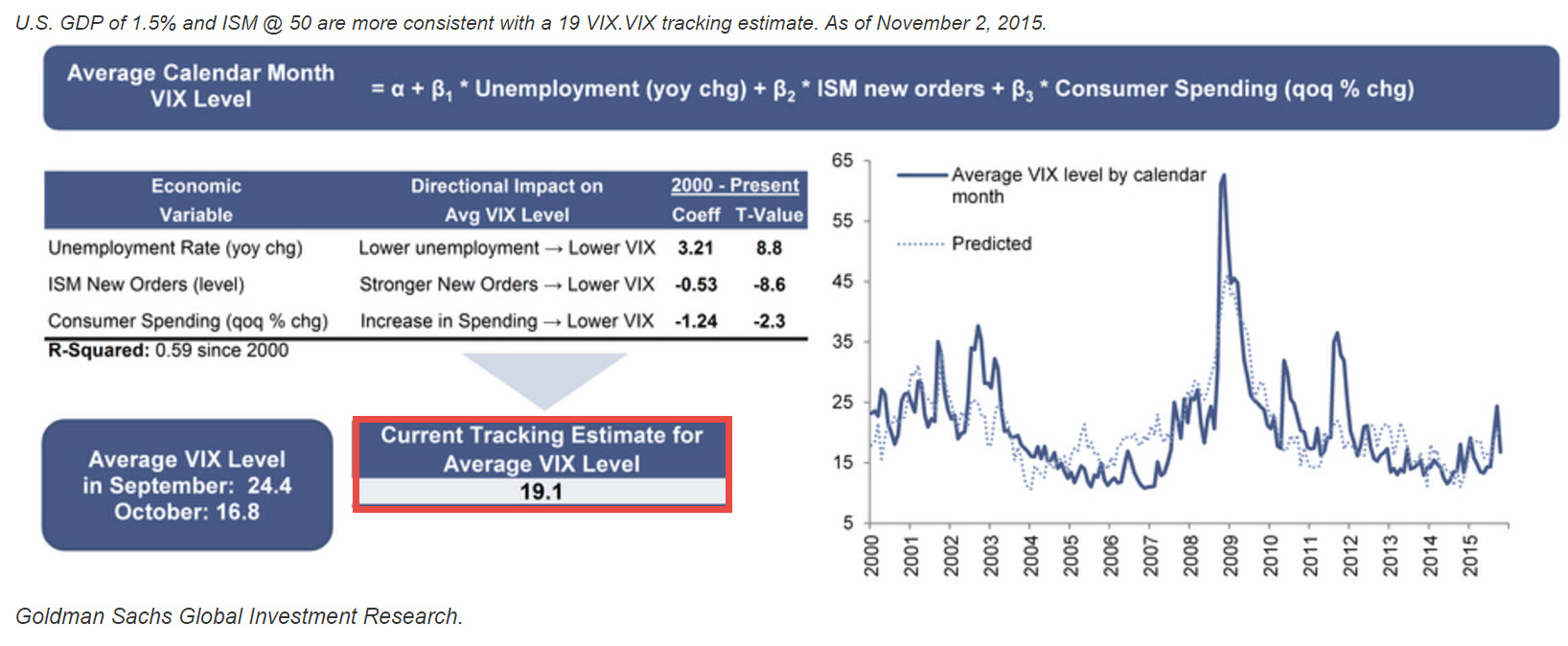

Argument for higher volatility:Uncertainty surrounding a mediocre economy + FOMC reaction function; GDP of 1.5% and ISM @ 50 are more consistent with a 19 VIX

Our VIX model uses economic inputs to estimate trend VIX levels over time. With the ISM, consumer spending and unemployment data that we have in hand, our models would suggest baseline VIX levels of 19, not 14 and change. Reverse engineering our model we estimate that a 14 VIX is more consistent with an ISM new orders level above 60 (ISM high 50’s) given no change in consumer spending or the unemployment rate.

The U.S. options market may be expecting economic stabilization, or a lower likelihood of a December rate hike given an ISM at 50.1.

Volatility: Less room for error with ISM @ 50 and GDP is 1.5% rather than 3%

GDP is 1.5% and ISM at 50.1: In our 2015 Volatility Forecast (January 20, 2015), we showed that the FOMC has tended to hike rates when the economy is on solid footing. U.S. real GDP growth has been 3% or higher during the quarter of the initial hike and the ISM averaged 57.6 the month of the hike and a robust 57 one- to three-months after a hike over the last three rate cycles. While the VIX is already pricing in an ISM level in the high 50’s and the FED has put a December hike back on the table, the economy is well below where we were at the beginning of past hikes. The advance number for real GDP was +1.5% in Q3 and the ISM stands at 50.1. That gives us a lot less cushion than in past cycles.

Implications: Modest U.S. and global growth may imply that U.S. market volatility (much like the FOMC) will be a lot more data dependent.

The economy and the FOMC reaction function will be the key into year-end. Our point is that the potential for volatility to swing higher seems more likely when we are (1) at low VIX levels, (2) the economy is mediocre, and (3) the market is navigating the ramifications of a potential December rate hike.

Bottom line: a VIX back at 2013-2014 levels seems low if a December rate hike really is in play. In terms of timing, it may be natural for volatility to take a breather after the intense market swings experienced in August-September, an earnings season, and three highly scrutinized central bank meetings (FOMC, ECB, BOJ). We would take advantage of lower option prices to implement direction views.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.