Ben Phillips, an Associate Professor at the ANU’s Centre for Social Research and Methods (and formerly of the National Centre for Social and Economic Modelling) has published new modelling backing Labor’s proposed reforms to negative gearing and the capital gains tax (CGT) discount, finding that these reforms would generate many billions of dollars of savings for the Budget (primarily from the top 10% of income earners) and would boost dwelling construction. The modelling also finds that Labor’s policy is far superior to the Turnbull Government’s rumoured $20,000 cap on negative gearing deductions, which would raise a relative pittance in extra tax revenue:

We estimate that in 2017-18 the total tax savings from negatively gearing properties is $4.3 billion. Under the Opposition plan these tax savings would only apply to newly constructed investment properties and all investments made prior to July 1 2017 would be grandfathered. Such exemptions would mean that the initial tax gains to the Commonwealth would be relatively small but would grow quickly…

It could well be expected that restricting negative gearing to new housing only would increase the share of investment housing devoted to newly built housing. There is little basis for estimating the impact on new housing but a ballpark figure that the share would increase to somewhere between 10 and 20 per cent would not seem too unrealistic. This would mean that the increase in tax revenue would be less than the $4.3 billion – somewhere between $3.4 and $3.9 billion per year in the longer term. In terms of number of persons affected the likely number would be between 1.0 and 1.1 million persons – with roughly 100,000 to 200,000 persons opting to purchase a newly constructed dwelling and therefore retaining negative gearing.

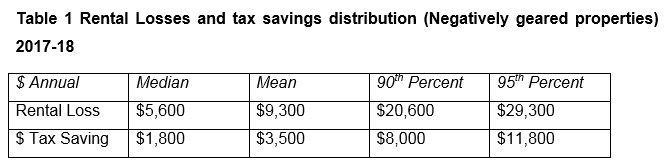

The typical tax savings for negatively geared individuals is $1,800 per year but the top 10 cent save at least $8,000 per year and the top 5 per cent save $11,800. The distribution of rental losses expected for 2017-18 show that the typical losses are $5,600 per year but the top 10 per cent are losing $20,600 per year and the top 5 per cent lose $29,300 each year…

An alternative to removing negative gearing (amongst several) is to cap the rental losses. We find that capping rental losses at $20,000 in 2017-18 would impact only around 10 per cent of negatively geared investors but increase tax revenue by around $1 billion each year…

Capital Gains distributional analysis…

In total we find that the capital gains discount reduction proposed by the Federal Oppostion will, in the long term save around $2 billion per year in 2017-18 dollars. Clearly, with a grandfathering arrangement in place the savings will take a substantial number of years to reach this level…

Conclusion…

We estimate that the removal negative gearing will increase taxation revenue in the long run between $3.4 and $3.9 billion dollars a year depending upon the increase in new housing construction that flows from the exemption for new housing. This analysis only include rental investments and does not include a number of other asset classes also impacted by the policy. Rental investments are easily the largest component impacted so we expect the overall impact will only be moderately larger than that estimated here.

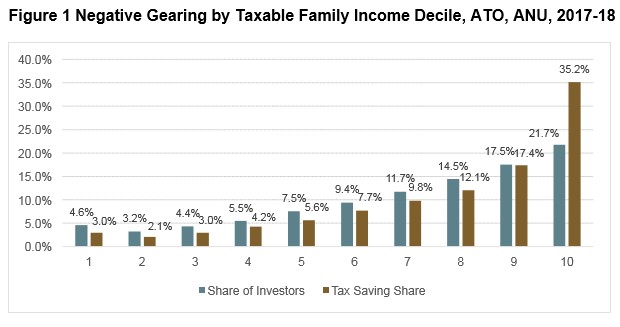

Our modelling shows that negative gearing benefits high income families with 52.6 per cent of the benefit going to the top 20 per cent of incomes. Only 5.2 per cent of benefits go to the bottom 20 per cent of incomes. This result is mostly driven by high income families being more likely to negatively gear, having larger negatively geared deductions and a progressive tax system that magnifies the gains for higher income persons.

We find that the typical amount of net rental loss is around $5,600 for a tax saving of $1,800. Negative gearing is heavily skewed with the top 5 per cent of net rental losses of $29,300 for tax savings of $11,800. Capping losses at $20,000 per year would cover around a quarter of the tax savings with only around 10 per cent of persons with negatively geared property affected.

Reducing the capital gains discount from 50 per cent to 25 per cent as proposed by the Federal Opposition would increase tax revenue by an estimated $2 billion in the long run in 2017-18 dollars. This is likely to be around a half of that obtained by the removal of negative gearing as also proposed.

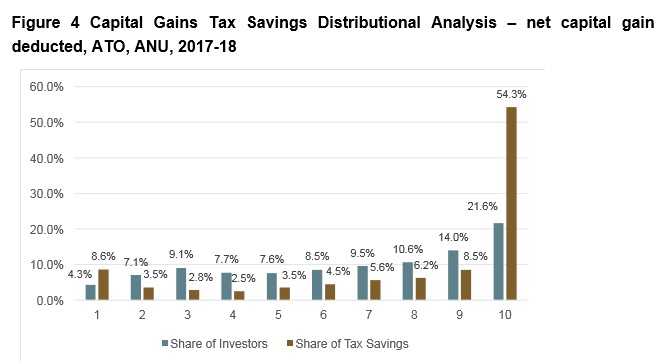

The capital gains discount overwhelmingly benefits high income families with the top 10 per cent enjoying nearly three quarters of the tax savings. By removing capital gains income from the decile income rankings we find that figure drops to 54.3 per cent flowing to the top 10 per cent of families as ranked by income.

Overall, we would expect significant long term savings from the proposal to remove negative gearing and to halve the capital gains tax concessions. Somewhere in the order of $3.5 to $3.9 billion per year in 2017-18 dollars for the negative gearing changes and $2 billion per year for capital gains tax changes. The two polices have been modelled in isolation and do not account for any potential interaction.

The vast majority of the additional revenue would be at the expense of the top 10 per cent of earners in Australia. Roughly two thirds of the tax revenue would come from the removal of negative gearing and the remainder from the halving of the capital gains discount to 25 per cent.

So, based on the above modelling Labor’s policy could save the Budget up to $5.9 billion a year compared to the Coalition’s rumoured $20,000 cap, which would raise only $1 billion per year in extra tax revenue. Labor’s policy would also help to boost dwelling construction, making it far superior.

Commenting on the results in Fairfax, Ben Phillips labeled Labor’s policy as “potentially the biggest housing affordability policy the country has seen”, while noting that “most of the benefit of negative gearing clearly goes to the top 10 per cent, and it’s the same for the capital gains tax, by a very large margin”.

The Turnbull Government is fast running out of excuses and lies to justify maintaining these tax rorts.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.