The ISM manufacturing and non-manufacturing surveys have long been benchmarks for economic momentum in the US. Albeit often the focus for markets, the headline results should not be fixated upon. Instead it is the rich detail that really matters, providing perspective on production; external and domestic demand; inventories; and employment.

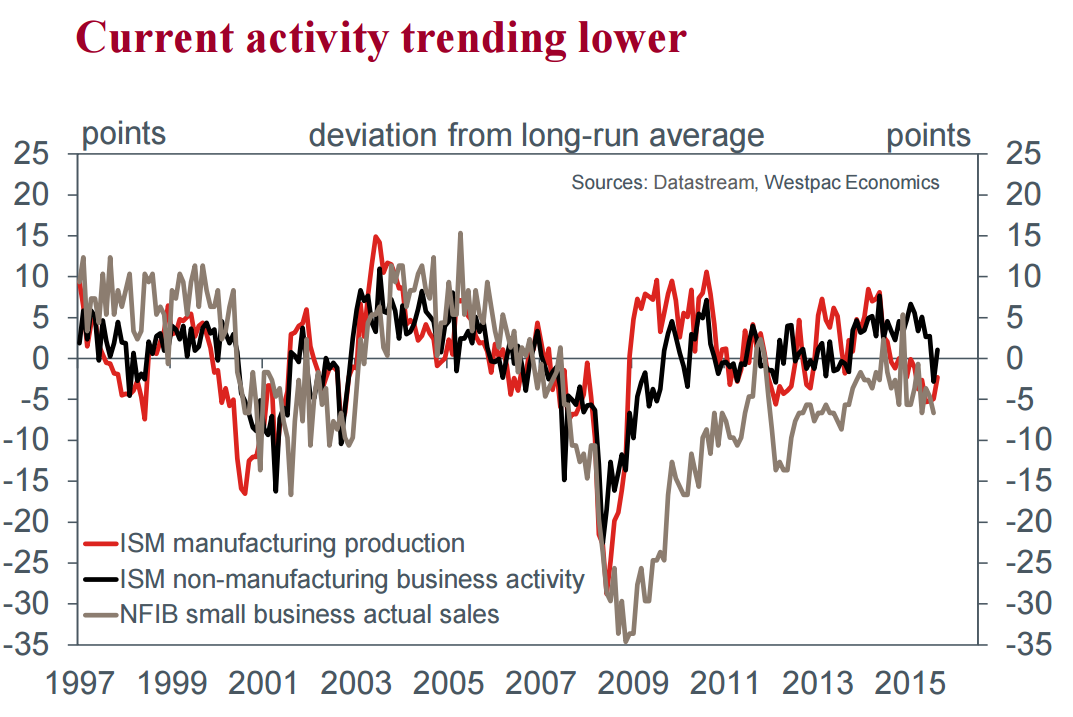

Beginning with production, late-2015 and January 2016 saw an abrupt downtrend take hold in production/current activity. Both indexes respectively fell from their long-run average (manufacturing) and well-above (non-manfuacturing) to below, and subsequently only saw a modest recovery in February. Corroborating this downtrend, the NFIB’s small business survey also deteriorated in step with the ISM’s (to January).

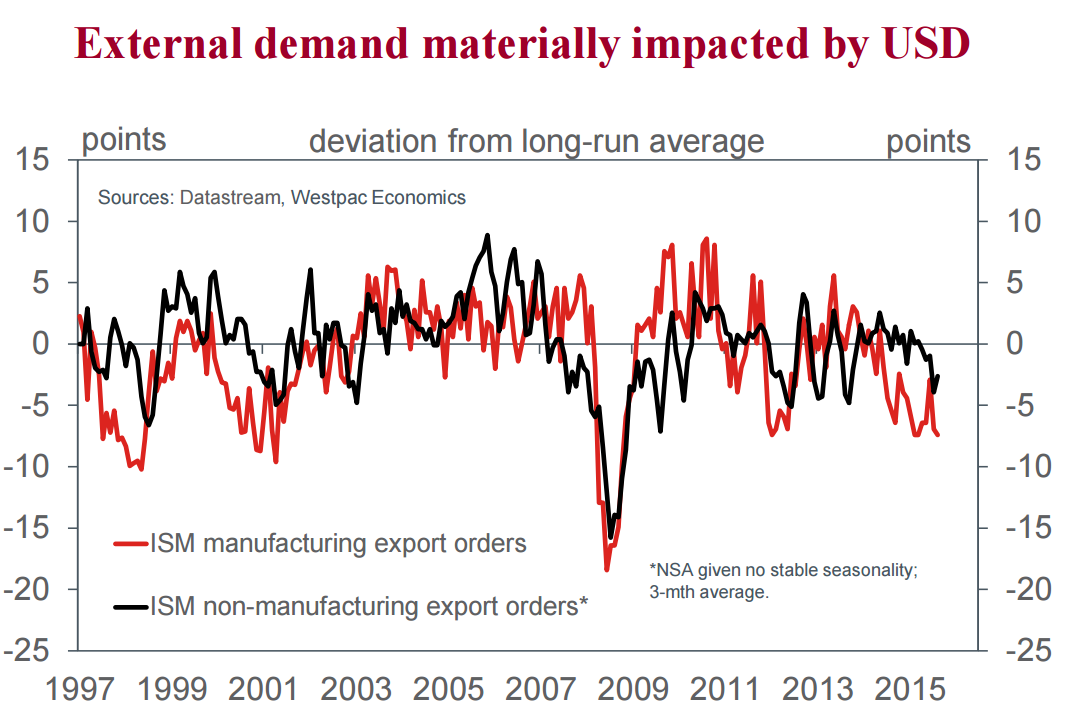

While the 12% appreciation in the USD against its trading partners over the year to June 2015 and the decline in energy sector investment previously impacted the manufacturing sector between November 2014 and mid-2015, a further 9% USD gain in the second half of 2015 intensified the manufacturing downtrend, and broadened the currency’s impact to the service sector. Clearly, for services, a threshold had been reached, challenging the sector’s competitiveness. Needless to say, soft global growth was also unhelpful during this period.

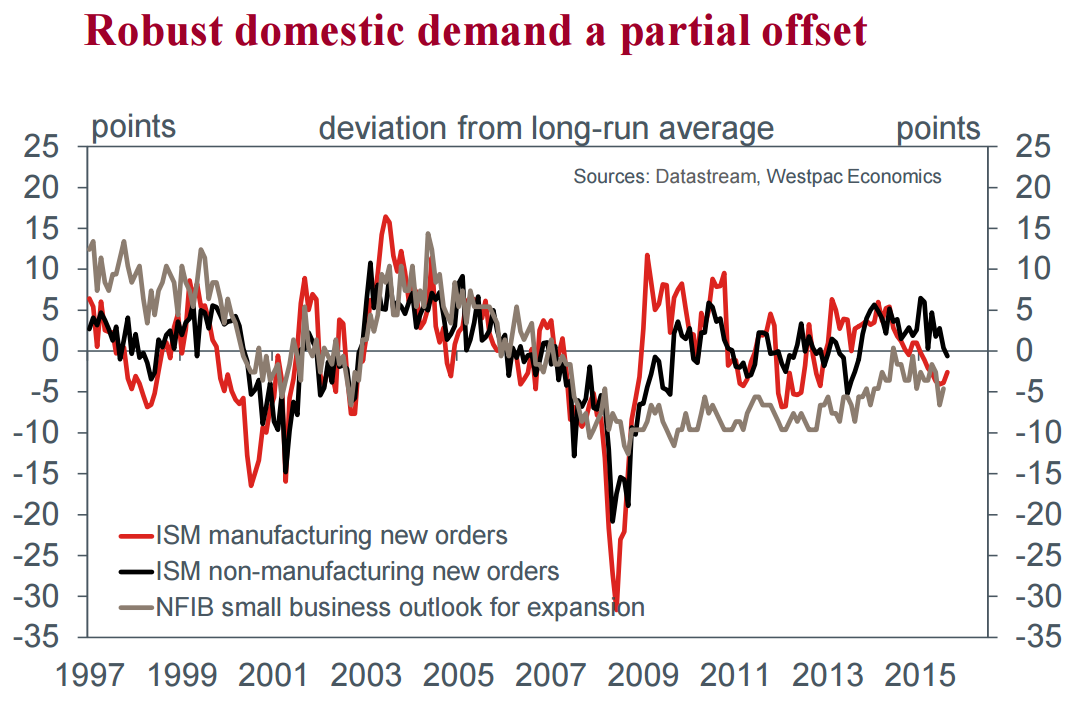

The impact that the USD has had on demand for both sectors’ output is best gauged by looking at the export orders series. For each survey, there has been a substantial and enduring decline. In comparison, the deterioration in the total orders series has been less severe. This signals that US domestic demand remains more robust. This is particularly true of services, for which total orders are currently ‘about average’.

Given the deterioration in external demand and fears over domestic momentum (owing to potentially higher interest rates and continued weakness in the energy sector), it is unsurprising that US firms have scaled back their inventory accrual (services), or are running them down (manufacturing). Inevitably this will reverse, but for the time being it remains a downside risk to GDP growth in Q1/Q2.

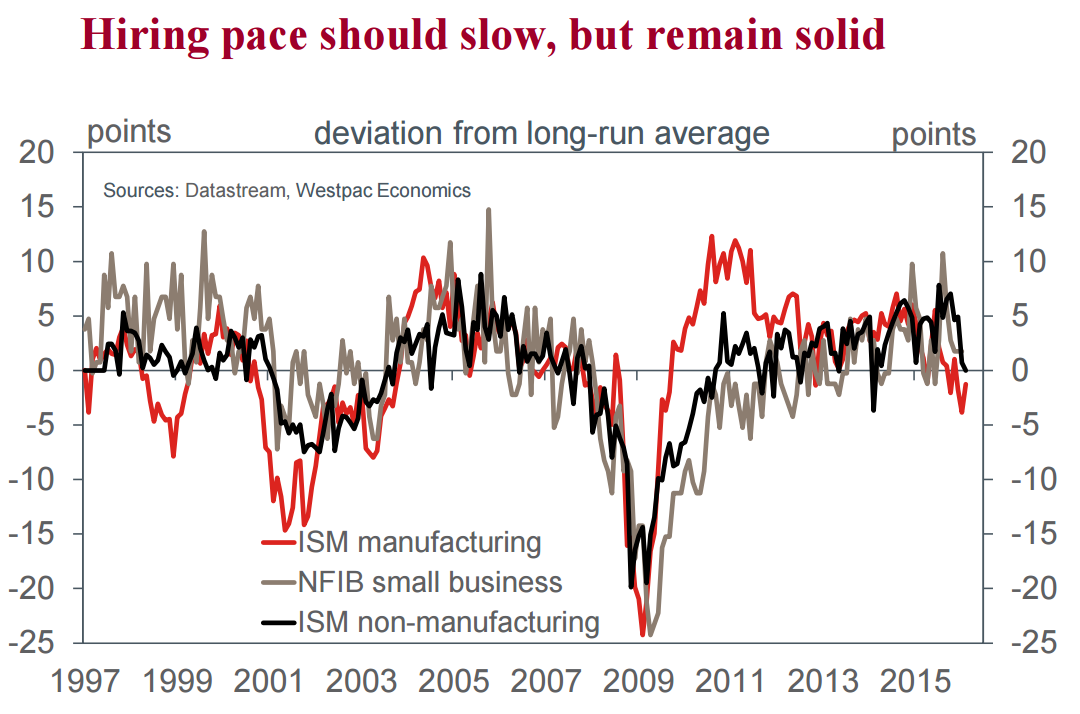

Far more important though is employment. From the ISM surveys it is clear that firms are reining in their demand for labour, across both manufacturing and services.

This trend does not represent a risk of weak or falling employment. Manufacturing employment has been soft over the past year, but growth remains positive. Meanwhile, the services sector has produced rapid job gains. The downtrend in the employment indexes therefore allude to a more modest pace of employment growth, consistent with a flat-to-slightly-down unemployment rate – that is, a moderation of 2015’s clear downtrend.

What such an outcome means for household incomes is also worthy of consideration. Wages growth has been slow to accelerate, and (if realised) a deceleration in job creation would keep a lid on wage pressures, with flow-on implications for consumer inflation.

For the FOMC, the detail from the ISM surveys signals some weakness in activity in the near term as well as good reason to be on guard over the potential impact a stronger USD could have on the US economy (particularly if global growth remains modest, or weakens further). For now though, there is not enough evidence to suggest meaningful job losses are on the way, or that the pace of wage growth and underlying inflation will come under threat. Albeit delayed, normalisation therefore remains in train.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.