From S&P today comes some spectacular research measuring the extend of global capex cuts as the Mining GFC takes full toll of materials and energy firms;

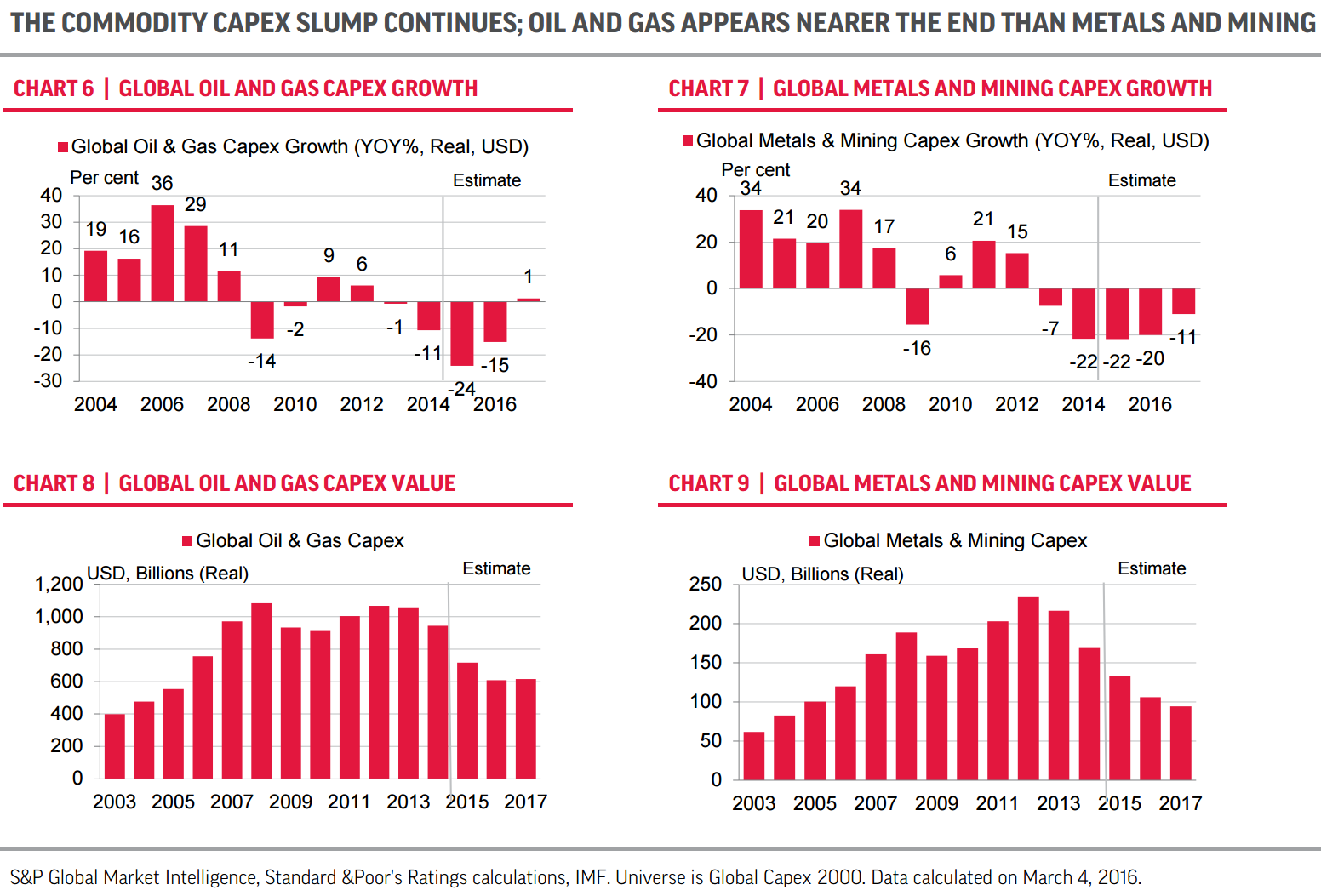

Crescendo. Cuts to commodity-related capex have reached a crescendo. We were already pessimistic about the broader capex outlook because of likely retrenchment in this area, but the severity of recent cuts has been remarkable. We estimate that global oil and gas capex fell by 24% in 2015 and will shrink a further 15% this year. Metals and mining capex appears to have fallen by 22% in 2015 and is likely to drop by another 20% this year.

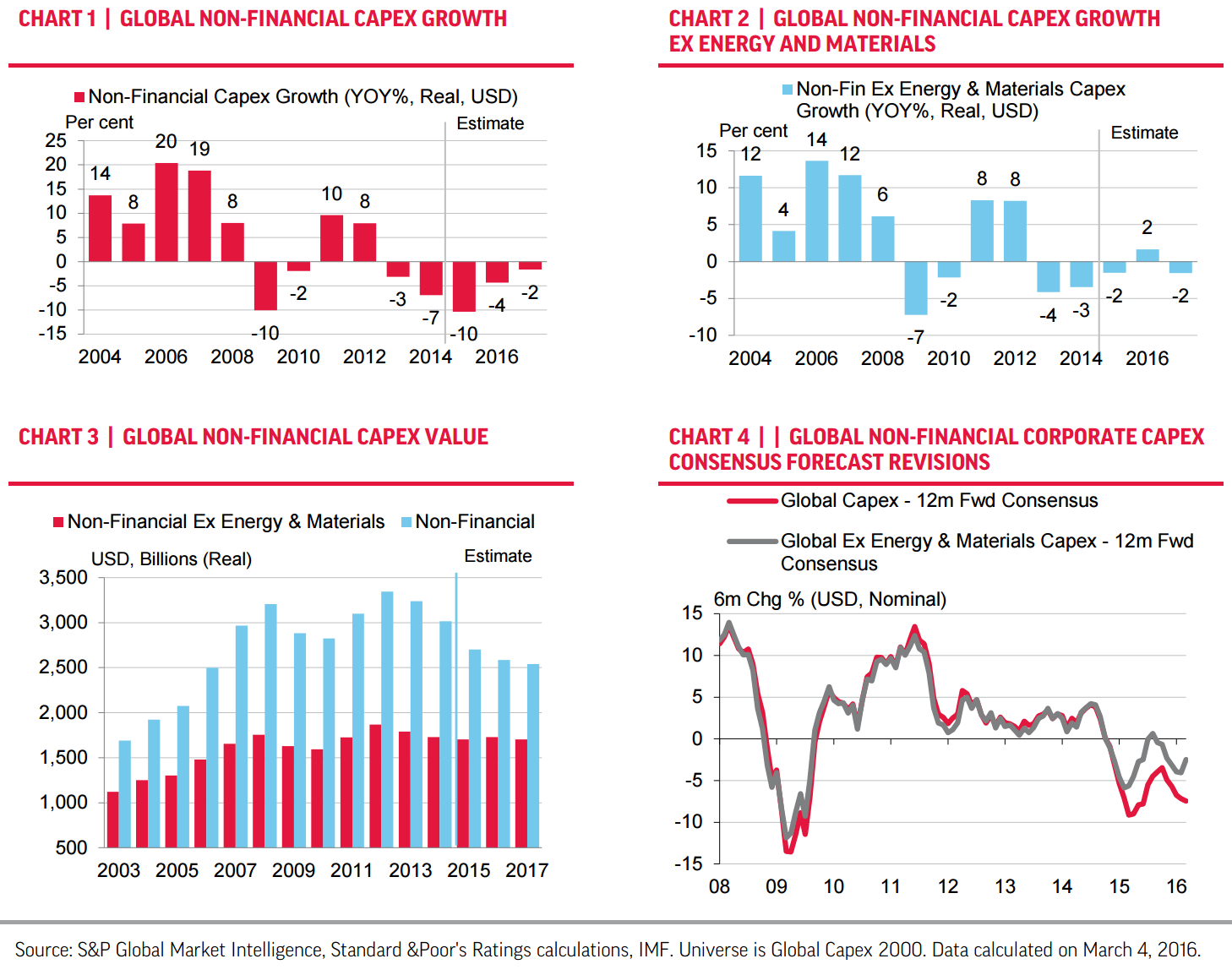

• Diminuendo. Global capex spending continues to contract as a result. On current estimates it fell 10% in 2015, and is likely to shrink by a further 4% this year and 2% next. If these projections are realized, the real term value of global corporate capex in 2017 will have slipped back to where it was in 2006. Forecast momentum also remains poor. Of the 32 companies in our Global Capex 2000 universe that were expected to invest more than $10bn in 2016, 25 have seen estimated spending fall in the past six months. Their total expected capex outlay has fallen by $58bn from $549bn to $491bn.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

• Diminuendo. Global capex spending continues to contract as a result. On current estimates it fell 10% in 2015, and is likely to shrink by a further 4% this year and 2% next. If these projections are realized, the real term value of global corporate capex in 2017 will have slipped back to where it was in 2006. Forecast momentum also remains poor. Of the 32 companies in our Global Capex 2000 universe that were expected to invest more than $10bn in 2016, 25 have seen estimated spending fall in the past six months. Their total expected capex outlay has fallen by $58bn from $549bn to $491bn.