Last week we mentioned that chief economist at the CBA Michael Blythe had penned a really awful housing bubble defense (no doubt aimed at debunking the recent Variant Percepation report) and today we offer a special report giving it the full treatment.

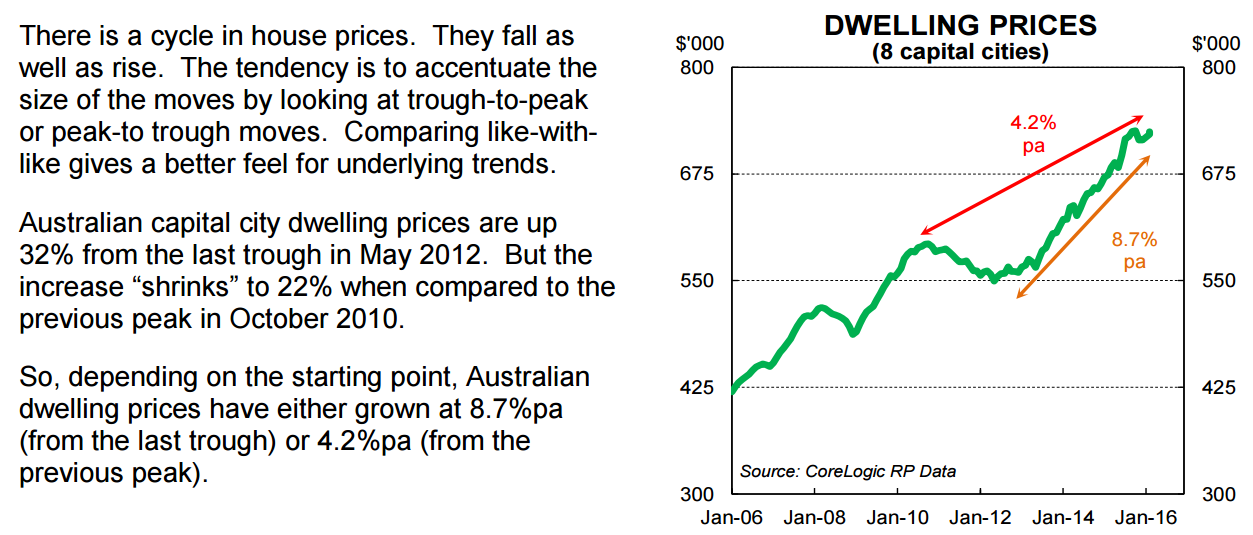

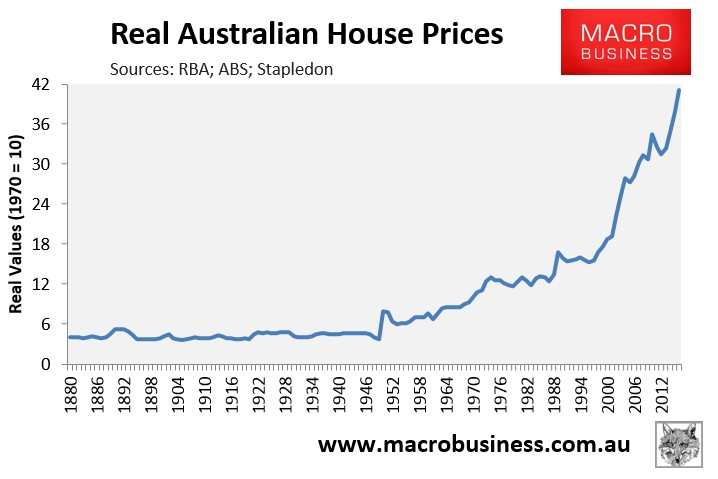

Can we just take look at the longer term chart:

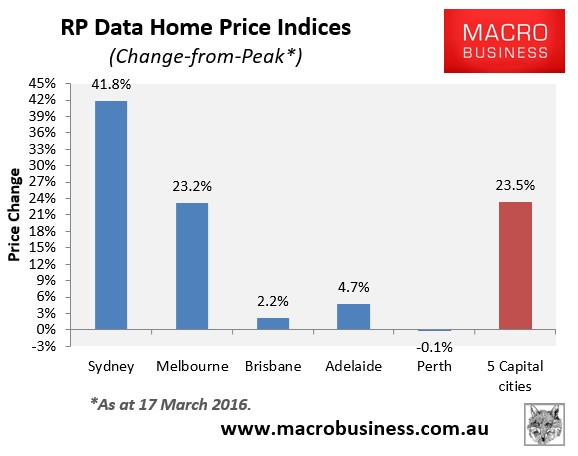

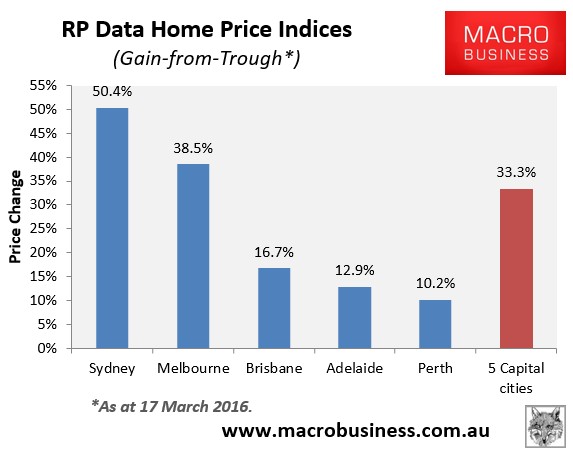

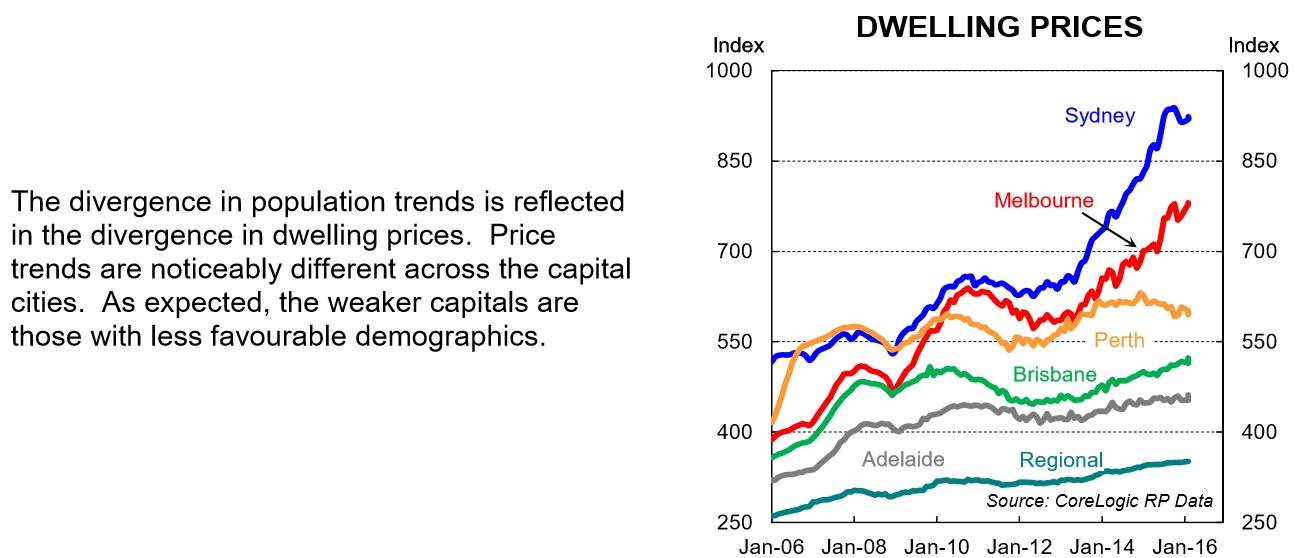

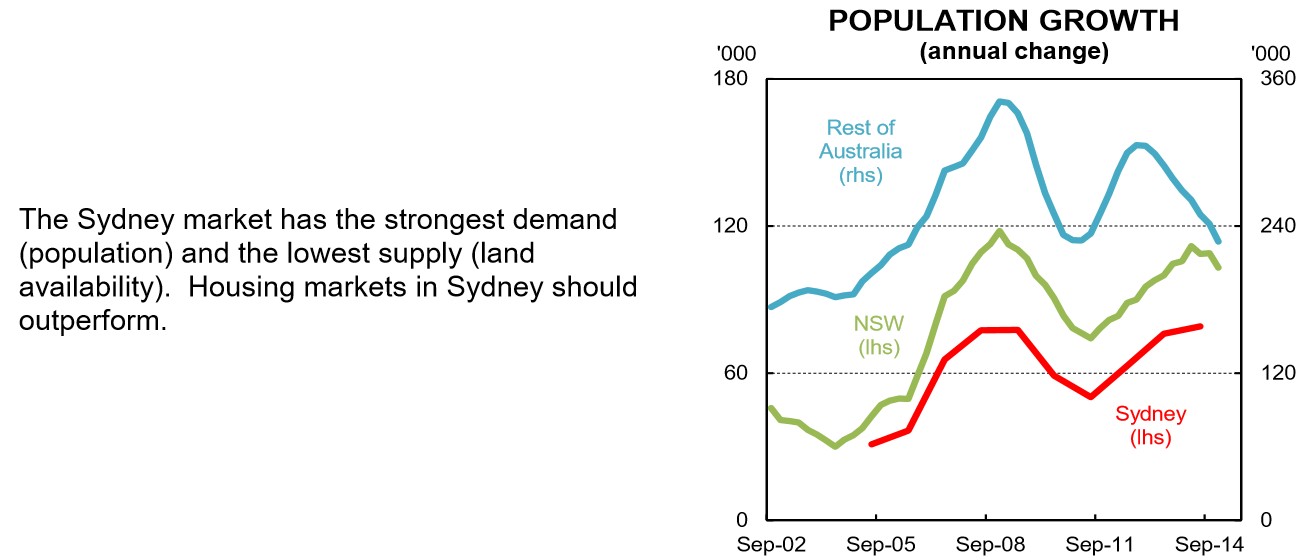

Or the Sydney and Melbourne gains from peak and trough:

Next:

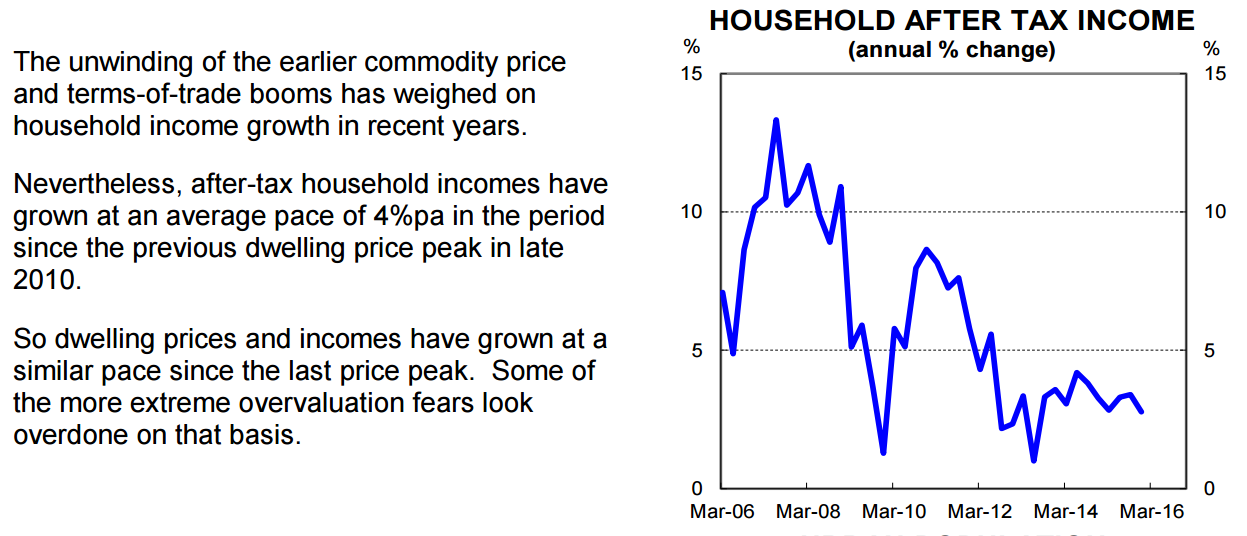

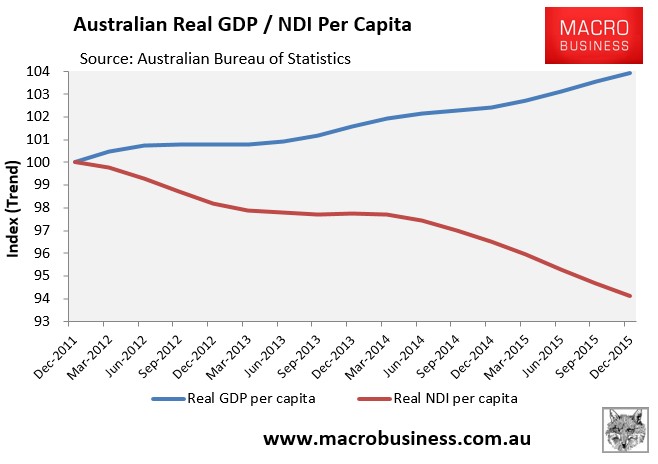

What matters is disposable income per capita and that has been tumbling throughout the last leg up in house prices:

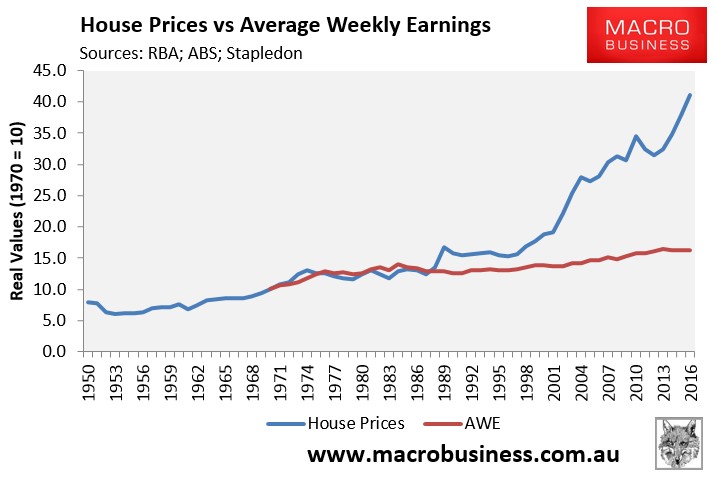

Or another way to look at it is house prices versus average weekly earnings:

Next:

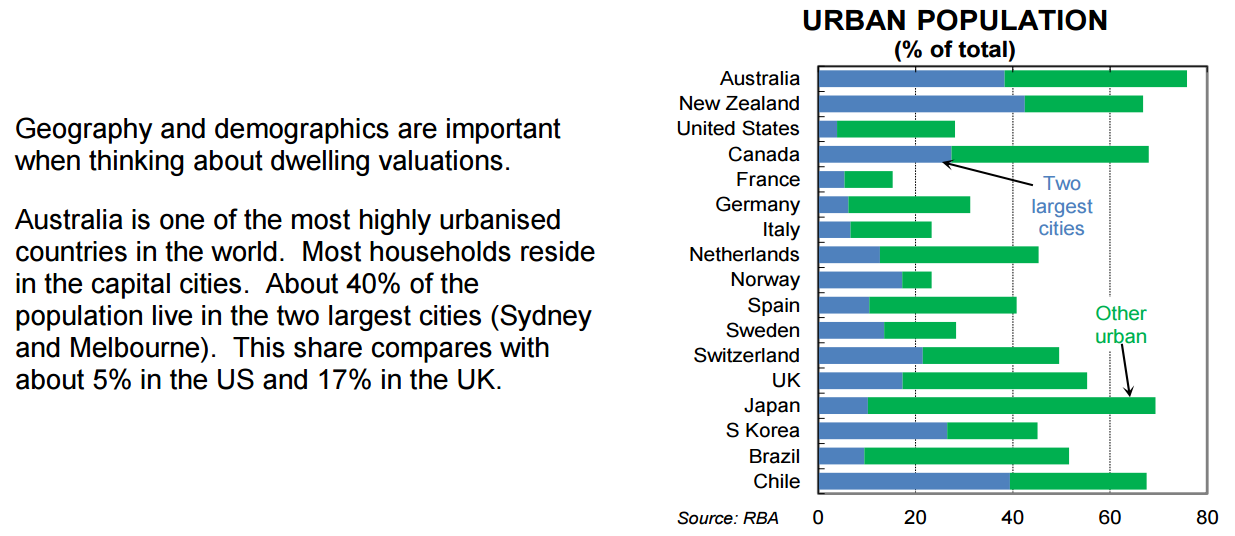

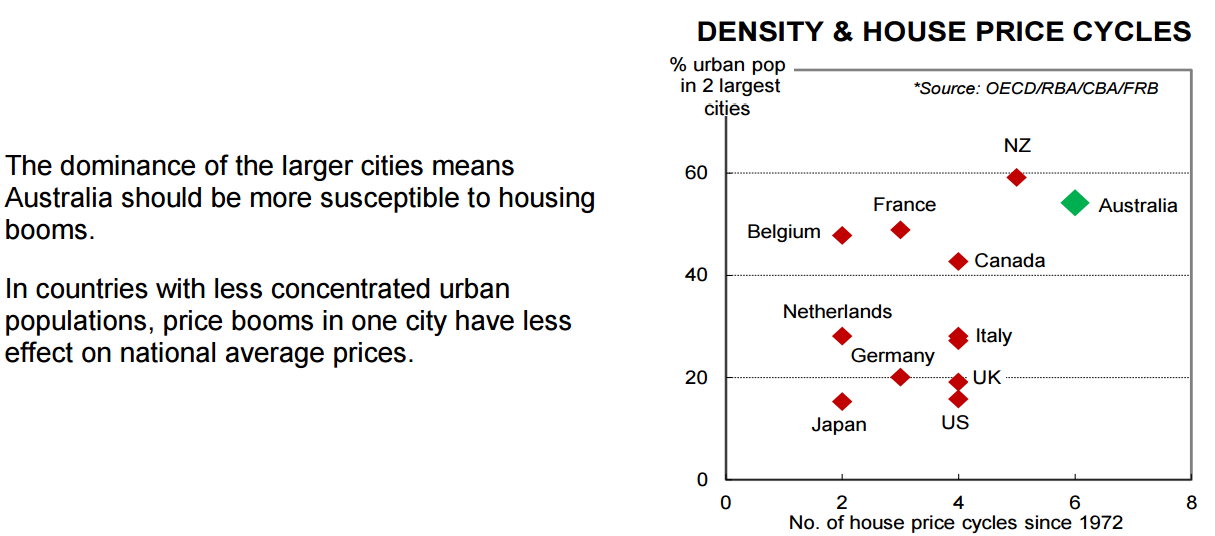

There is no reason high urbanisation levels should result in housing booms. None. There is no argument here at all, it’s just asserted as true.

Next:

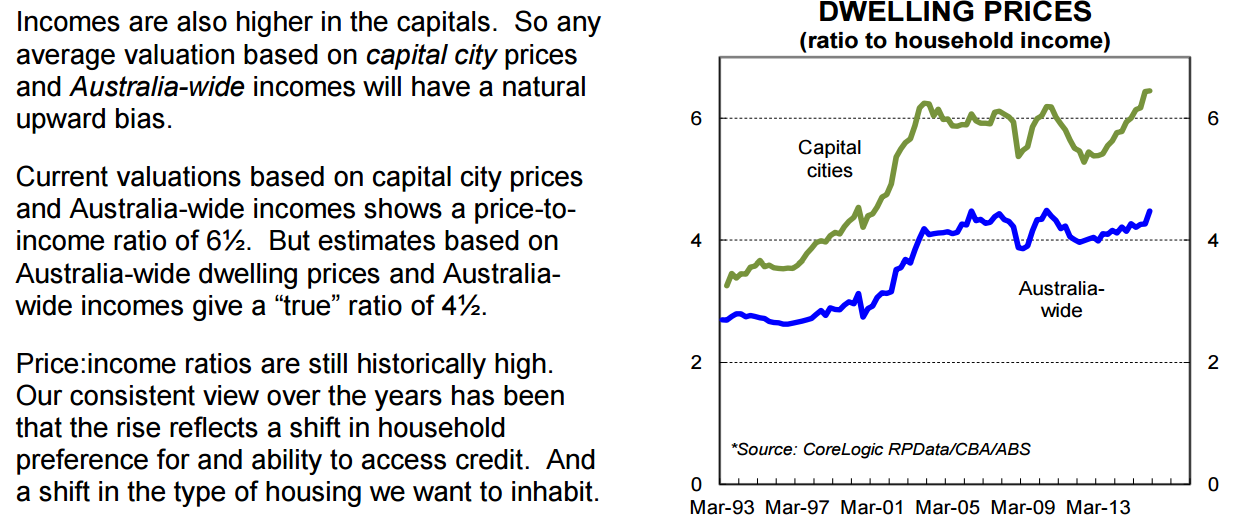

Where is the commensurate analysis of higher debt servicing costs resulting from the much larger mortgages in cities? Without it the only bias here is at the CBA.

Next:

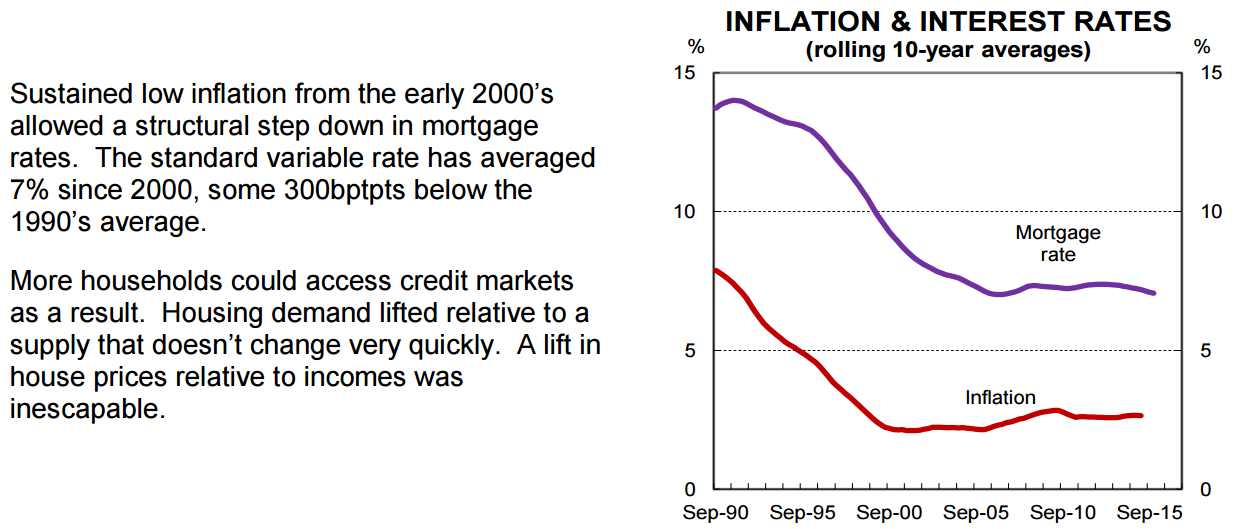

Nearly every bubble in history has been underpinned by easy credit. It is virtually a pre-condition.

Next:

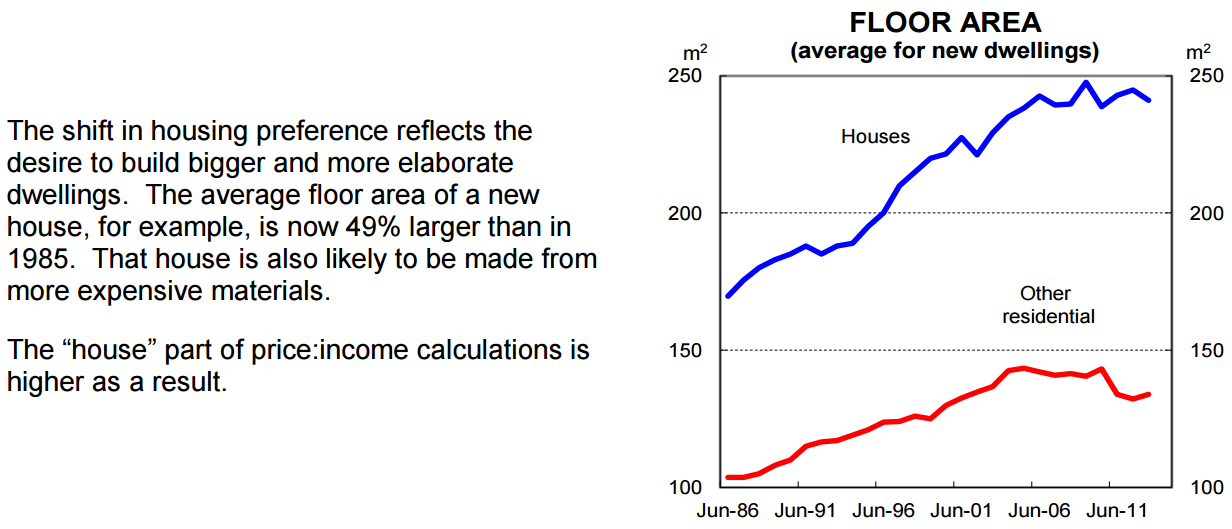

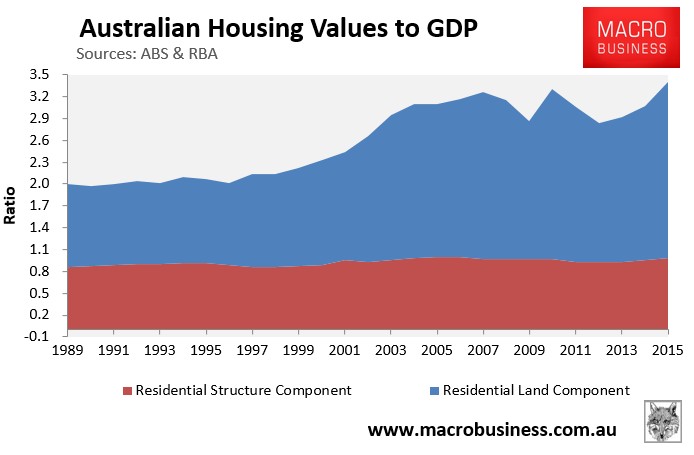

Almost all of the price inflation has been in the land not the house:

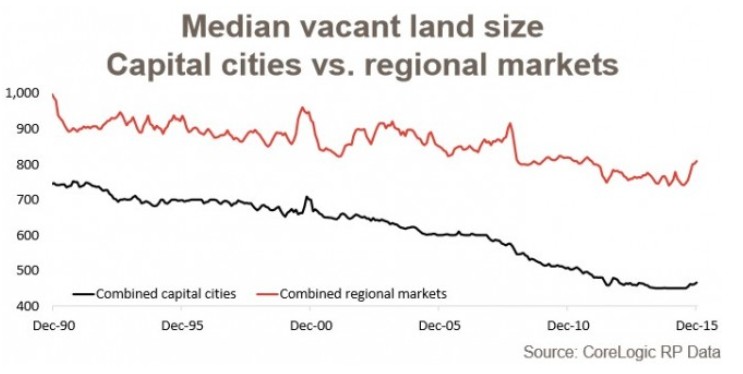

Moreover, median lot sizes have shrunk dramatically from 75o square meters in 1990 to 466 square meters at the end of 2015:

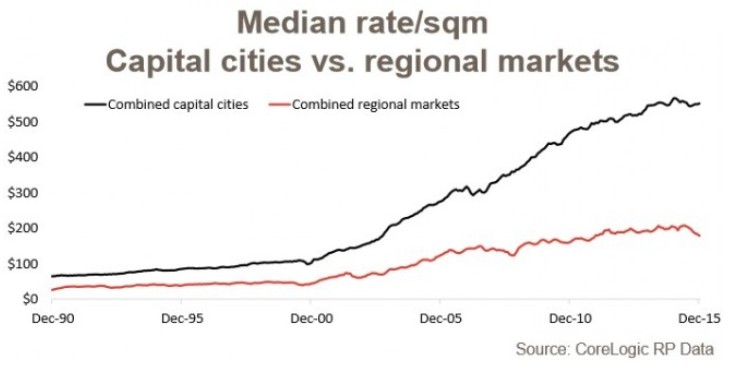

Accordingly, the median cost per square meter of vacant land has risen more than 500% over the past 25 years:

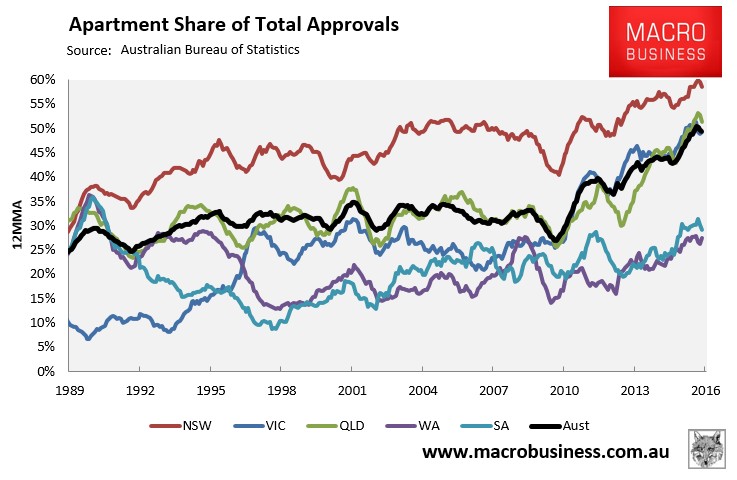

There has also been a shift into shoebox apartments:

In short, dwelling sizes are shrinking radically.

Next:

Here is a list of the public supports required to prevent a GFC implosion in values:

- exceptional RBA liquidity, under-pricing of the Committed Liquidity Facility (CLF) and the exposure of the CLF running into the hundreds of billions of dollars;

- deposit guarantees;

- wholesale funding guarantees;

- clandestine multi-billion dollar loans from the US Federal Reserve to the National Australia Bank (NAB) and Westpac Banking Corporation (WBC), only discovered in a document dump by the Fed under a Freedom of Information Act in 2010;

- multi-billion dollar purchases of residential mortgage-backed securities (RMBS) by the Australian Office of Financial Management (AOFM);

- Australian Securities and Investments Commission (ASIC) bans on short-selling;

- absence of ex-ante Financial Claims Scheme (FCS) fee;

- laxity of capital buffer requirements by the Australian Prudential Regulation Authority (APRA);

- reductions in risk-weightings, especially for mortgages;

- potential bail-ins of banks through converting deposits into equity as promoted by the Financial Stability Board (FSB);

- massive public stimulus;

- huge first home buyer grants, and

- opening the immigration spigot while relaxing foreign buyer restrictions.

Next:

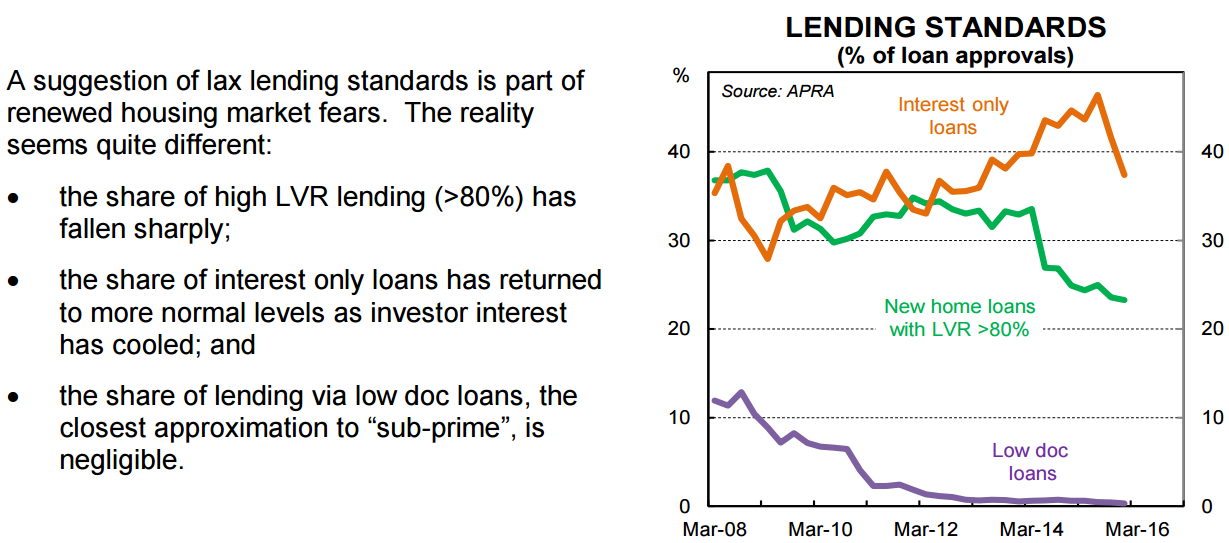

Interest only loans have only just started falling with macroprudential. They were the key driver of the post-2011 bubble pulse along with the huge investor surge which in Sydney reached absurd proportions:

Next:

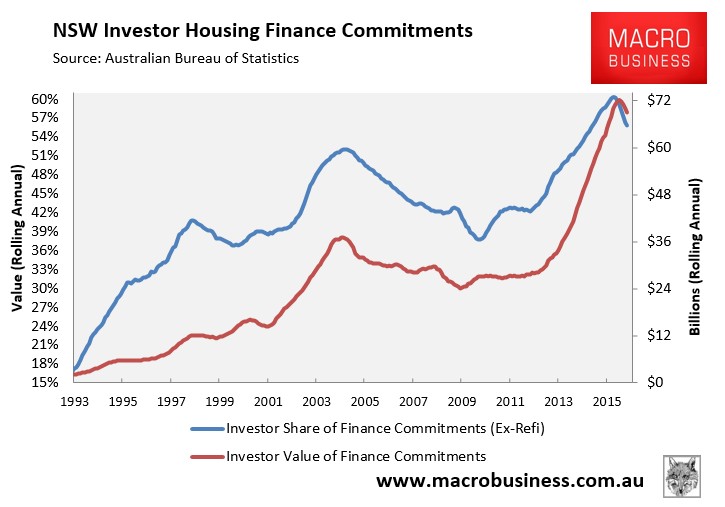

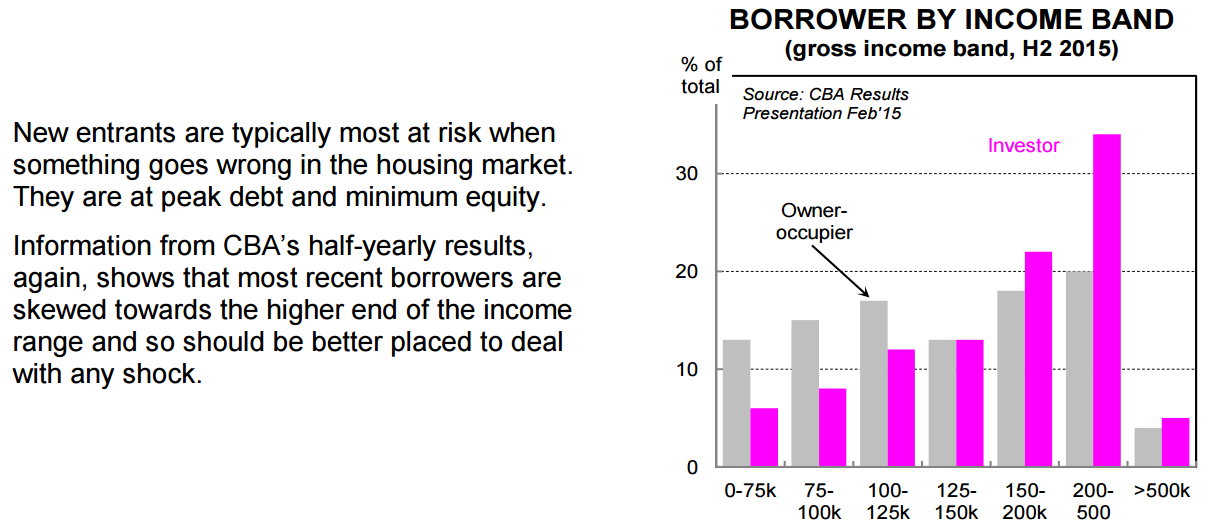

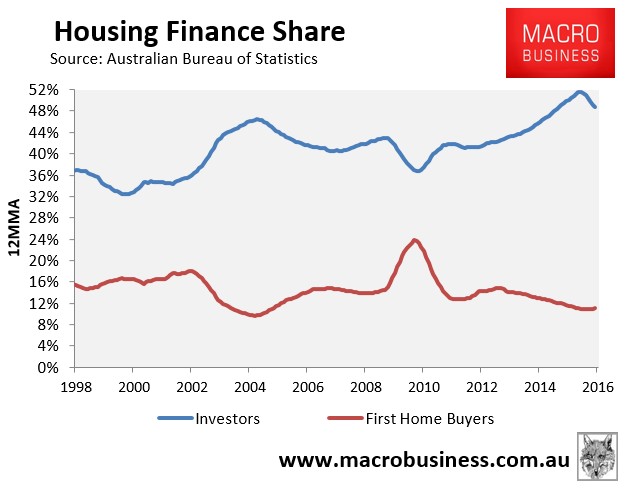

And what about the last leg of the bubble being driven by investors with loose hands?

Next:

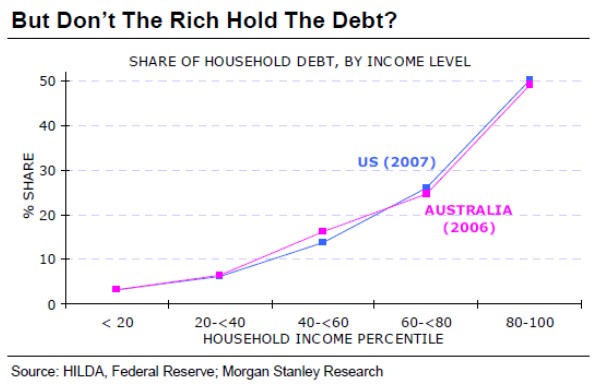

The US had a similar same debt distribution before it’s bubble popped:

Next:

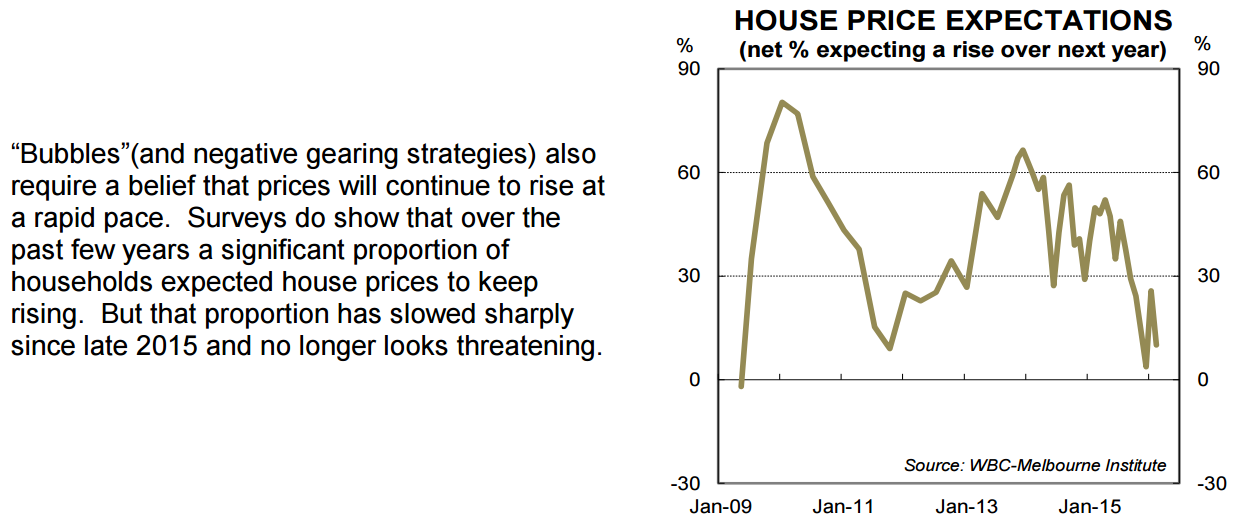

Looks like it was pretty high until very recently!

Next:

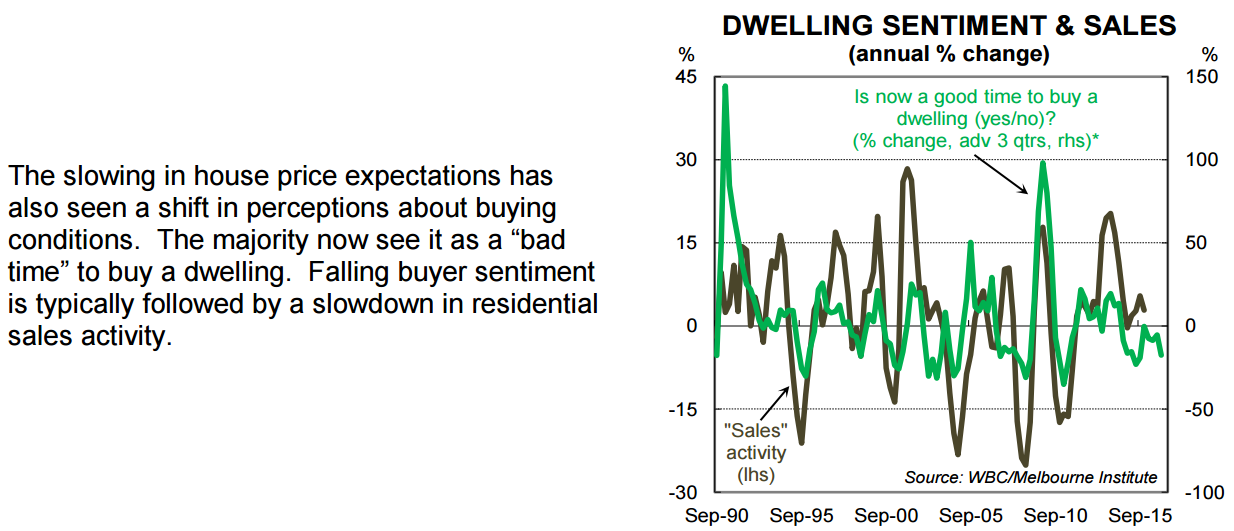

So the bubble is bursting?

Next:

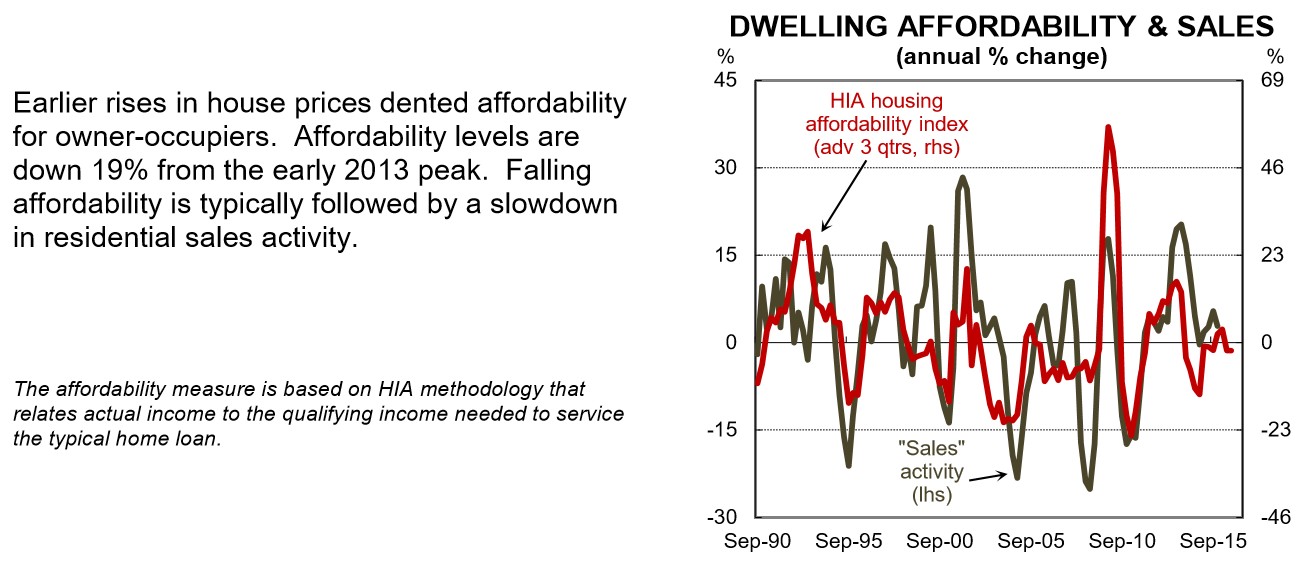

So affordability sucks then? No shit.

Next:

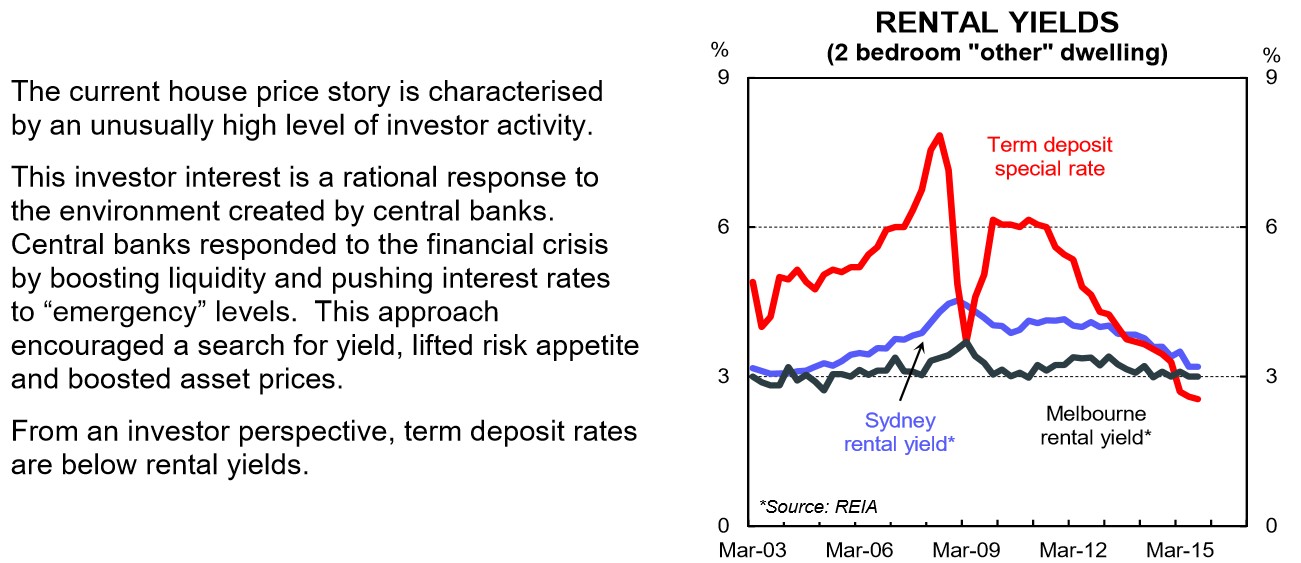

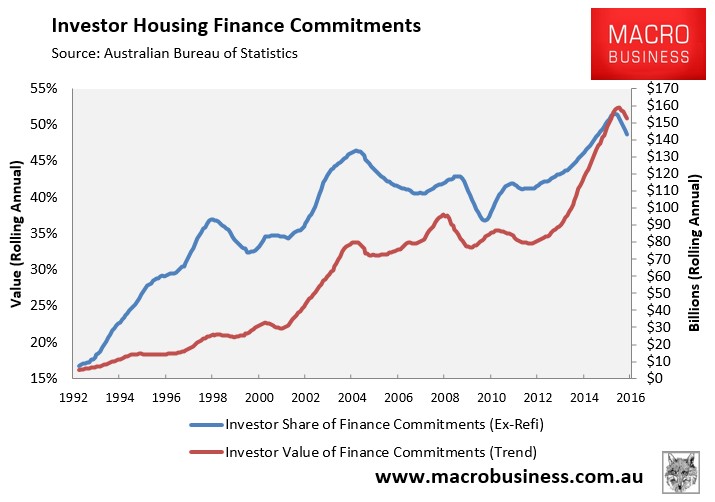

What’s your point? We know that it is an investor driven bubble:

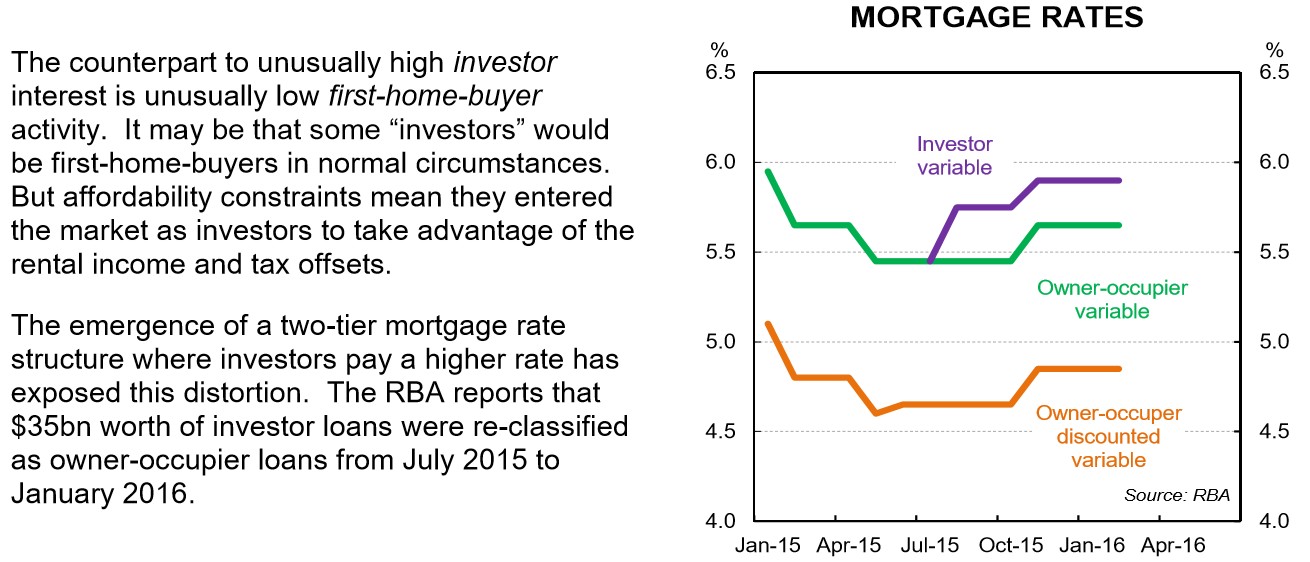

And we know that first home buyers have been shut out:

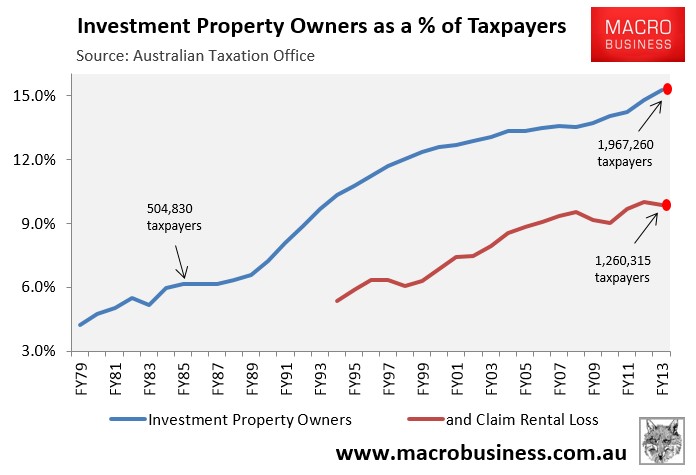

But why can’t you see that such a housing structure – whereby there are nearly 1.3 million negatively geared landlords effectively paying their property investment a dividend in the hope that it repays them with capital growth – is inherently risky?

How is this not by definition a speculative bubble?

Next:

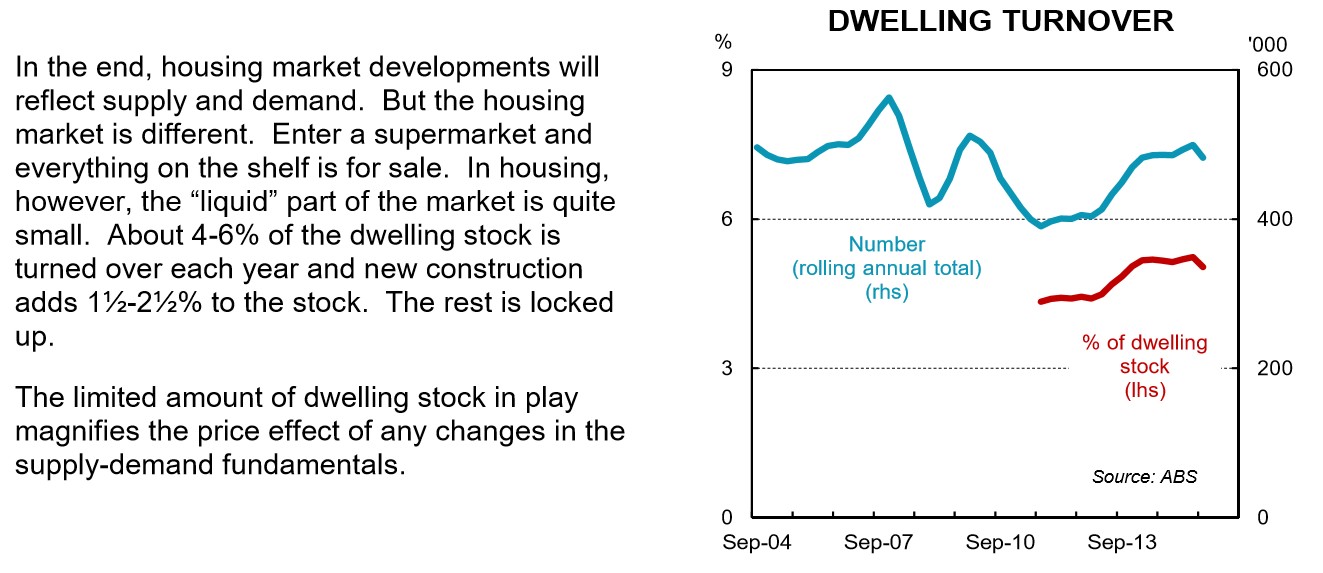

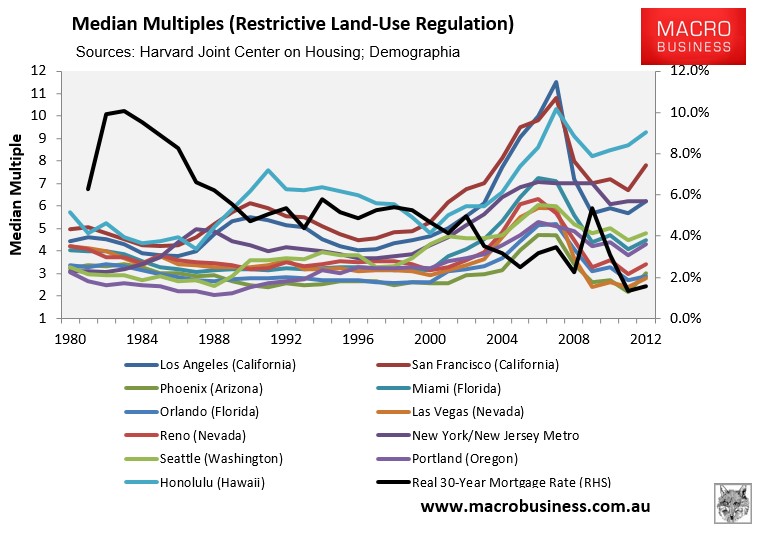

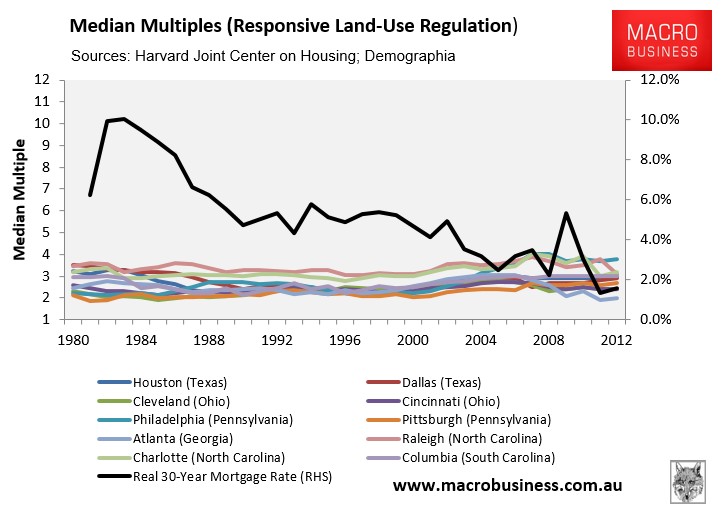

Very true. Tight supply means that prices are more sensitive to swings in demand. This is why the US states with restrictive planning experienced the biggest booms and busts in house prices:

Australia’s restrictive planning heightens the risk of boom and bust price cycles. It is not a one-way bet.

Next:

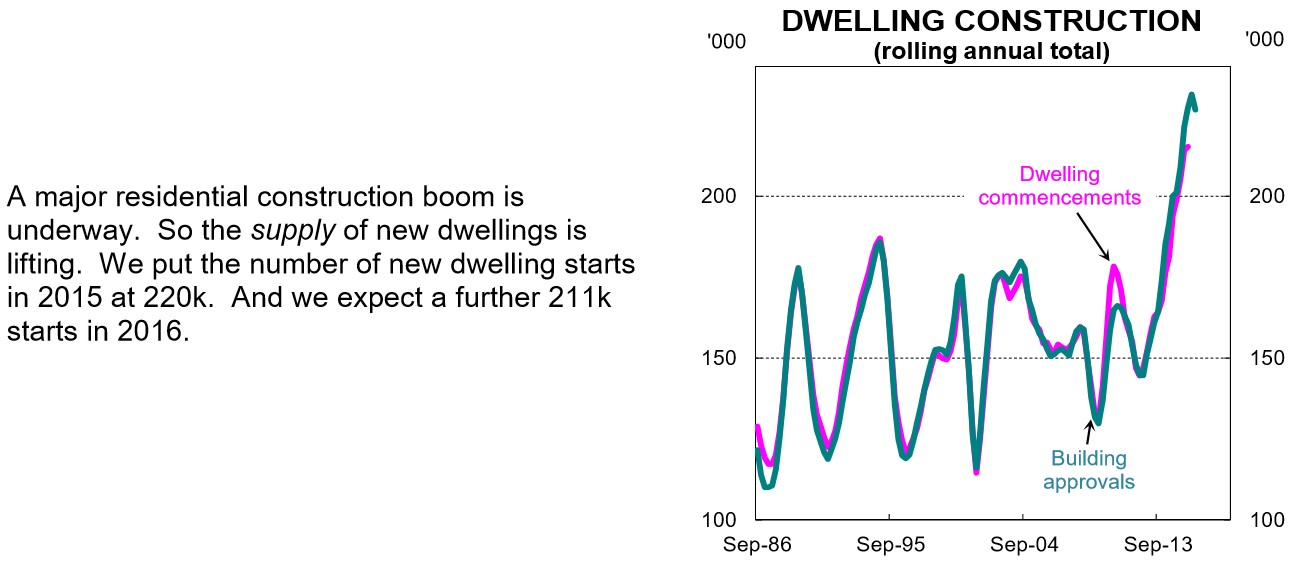

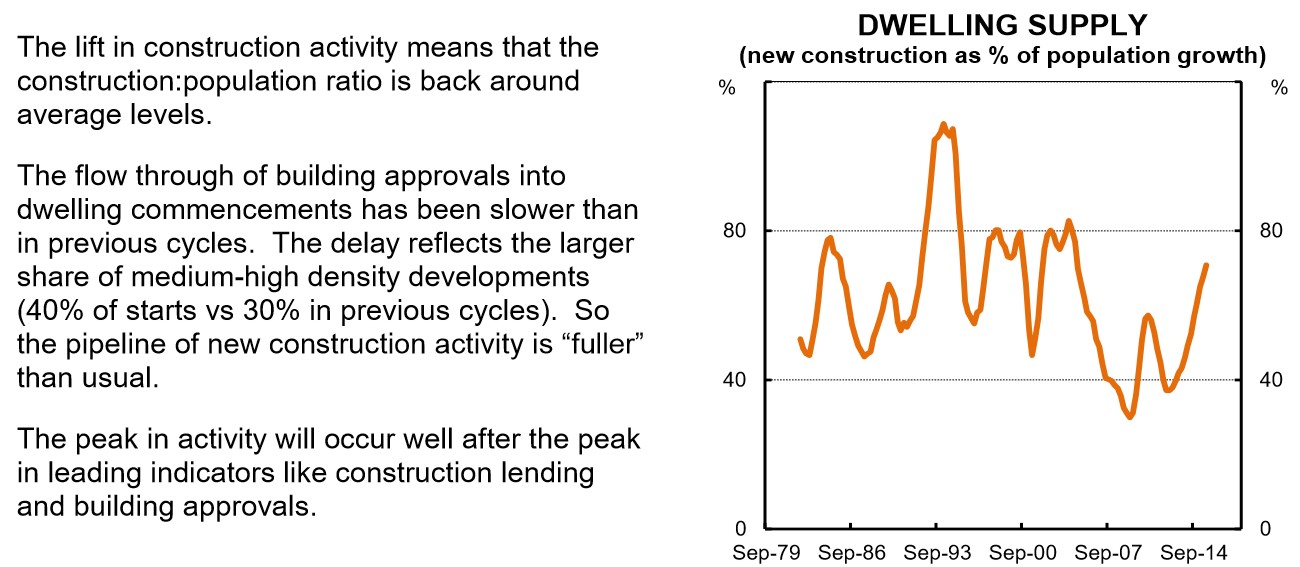

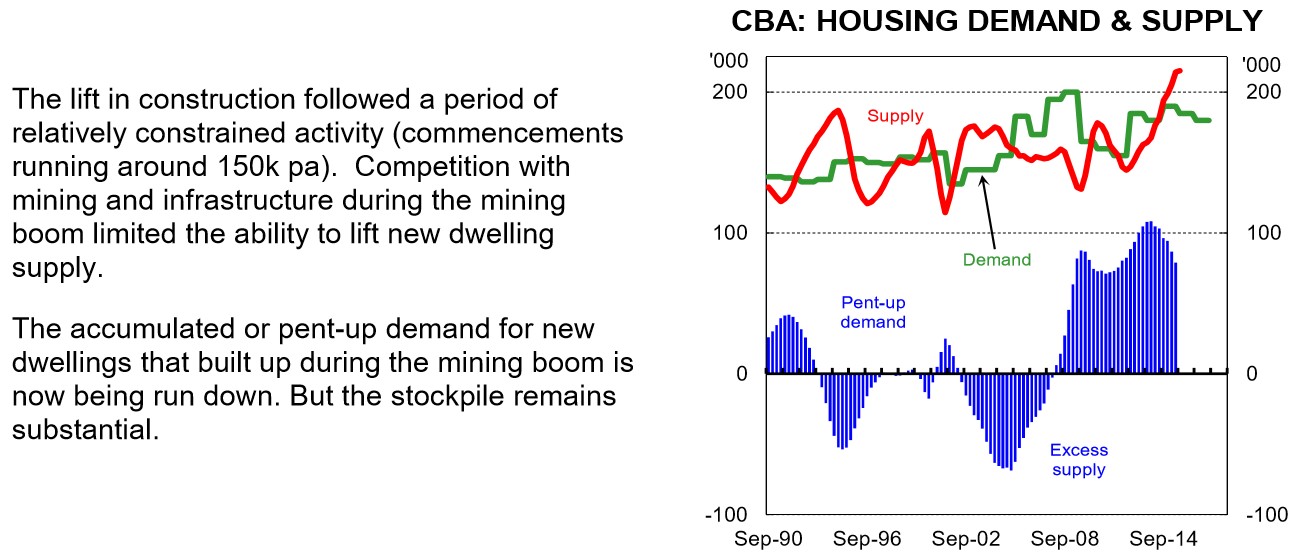

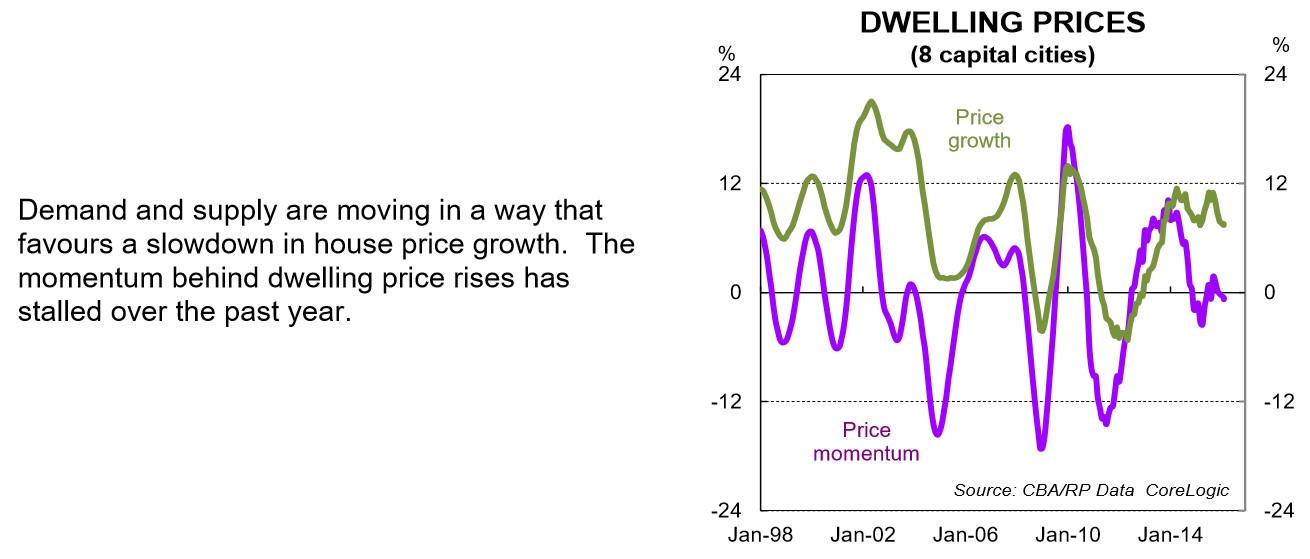

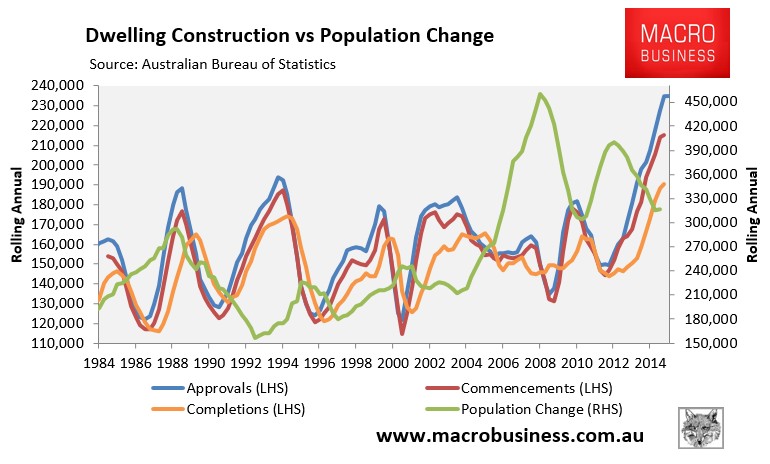

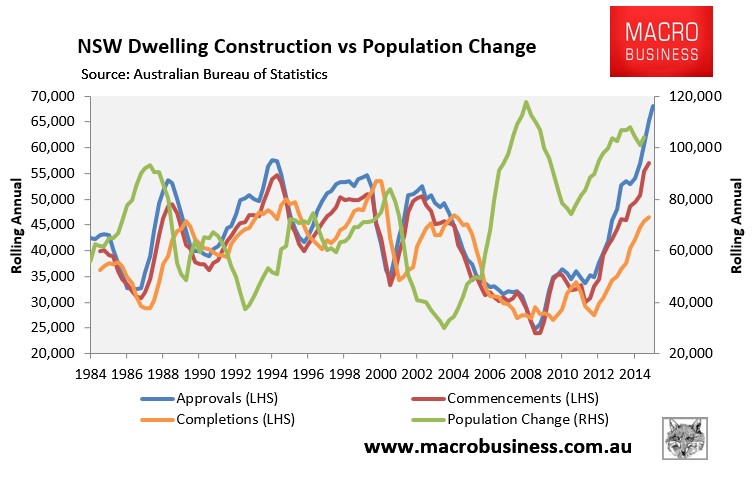

Dwelling supply is rising just as population growth is falling – hardly a positive indicator for house prices:

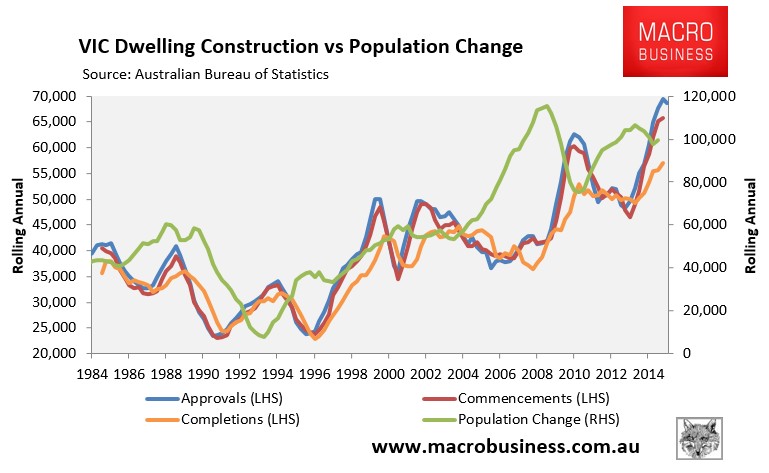

There is a big oversupply building in Melbourne:

And even the much vaunted “housing shortage” in Sydney is on borrowed time:

Next:

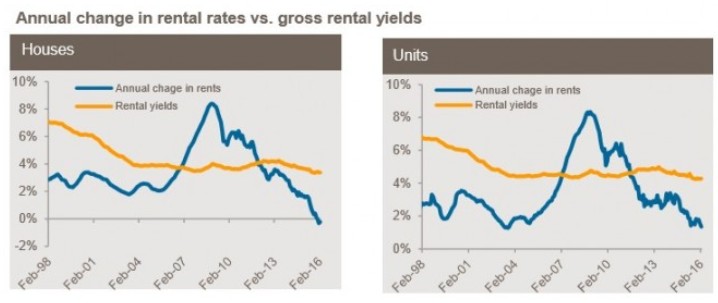

Actually, dwelling rents registered ZERO growth in the year to February, according to RP Data, which was the slowest growth on record. According to RP Data’s Cameron Kusher:

The causes of the slowdown in rental growth is falling wages, excess rental supply in certain areas and lower rates of population growth and population mobility impacting on demand for rental accommodation. With construction activity set to peak during over the next 24 months, but many new properties still to settle, there is a real possibility that rental rates will fall over the coming months. Landlords will continue to have little scope to lift rental rates while for renters it potentially means more surety in their accommodation and the potential to upgrade into a higher grade of accommodation for a similar cost…

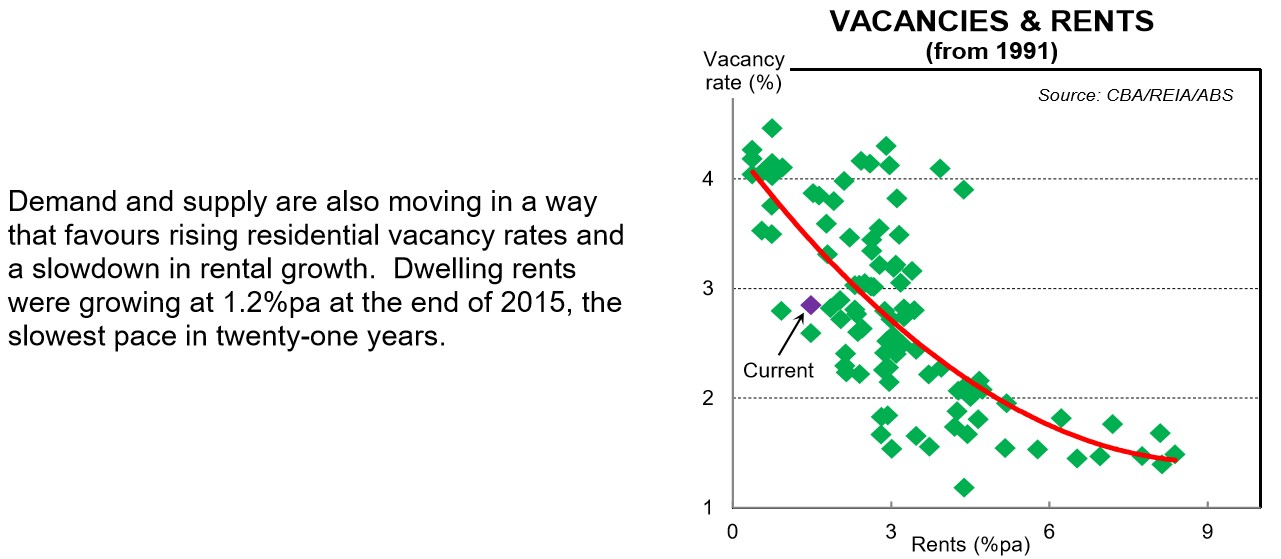

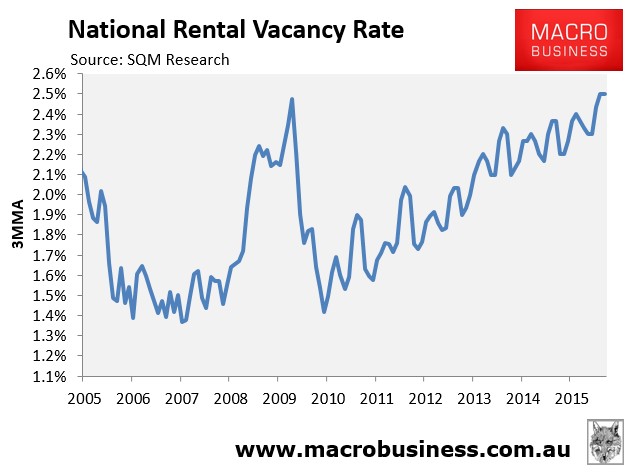

Moreover, rental vacancy rates are trend up and current sit at the GFC high:

Clearly Australia’s army of negatively geared investors are speculating on ongoing capital growth, which is the very definition of a “bubble”.

And finally:

The worry is not 2016. It is 2017 and 2018 as the triple forces of the declining housing market (both construction and prices), falling mining investment, and the closure of the car industry converge, substantially raising unemployment.

With housing values and debt at all-time highs, Australia’s economy will be precariously placed.