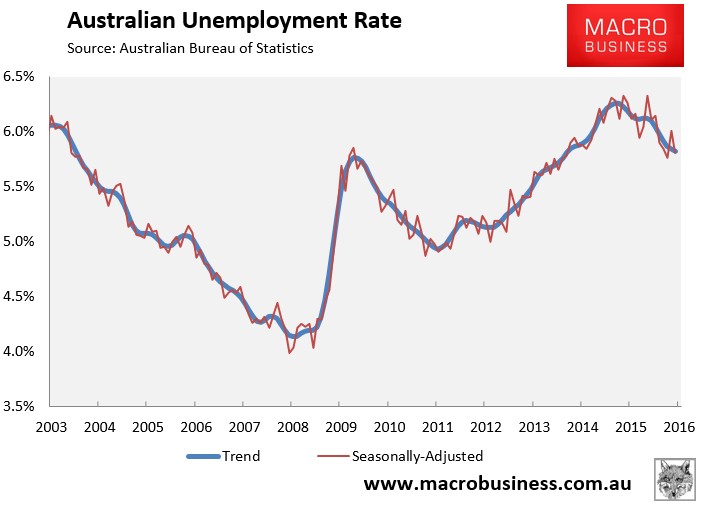

As summarised earlier, the Australian Bureau of Statistics (ABS) has today released its labour force report for February, which registered a tiny (300) rise in total employment but a 0.2% decline in the headline unemployment rate to 5.8%.

The fall in the unemployment rate beat analysts expectations of no change (i.e. 6.0%). However, jobs growth badly missed expectations, with analysts tipping an increase of 12,500 jobs in February.

In trend terms, the unemployment rate fell ever so slightly from 5.84% to 5.83%:

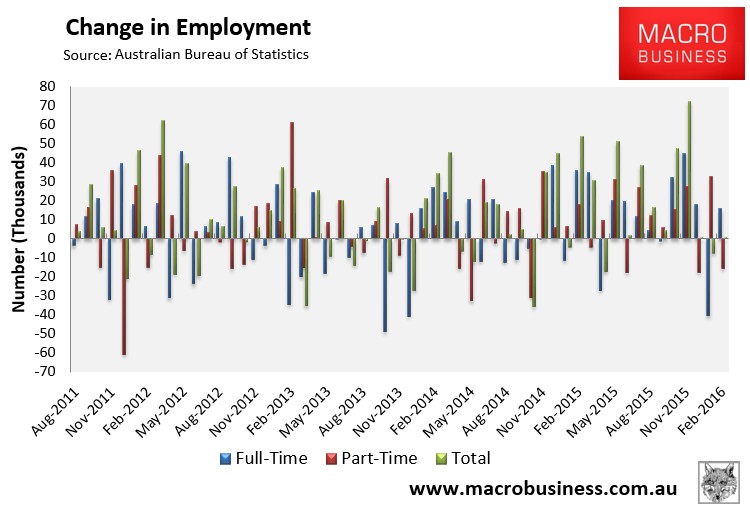

Again, total employment rose a seasonally adjusted 300 to 11,884,000, with full-time employment increasing by 15,900 to 8,192,600 and part-time employment decreasing by 15,600 to 3,691,500.

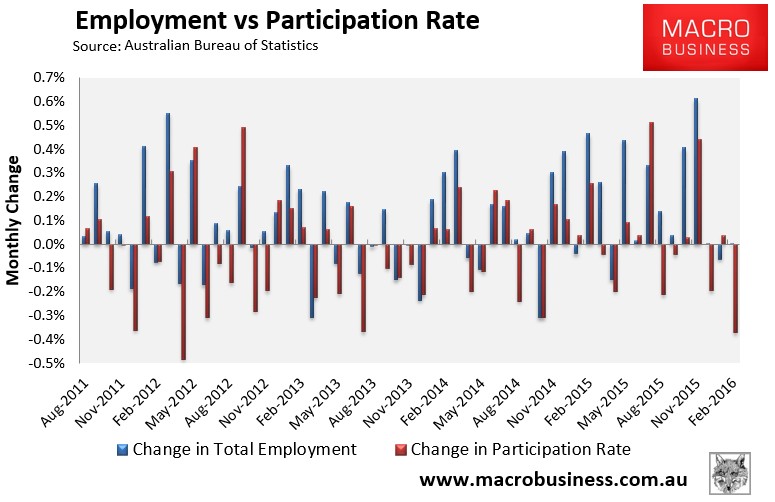

However, the participation rate fell sharply from 65.1% to 64.9%:

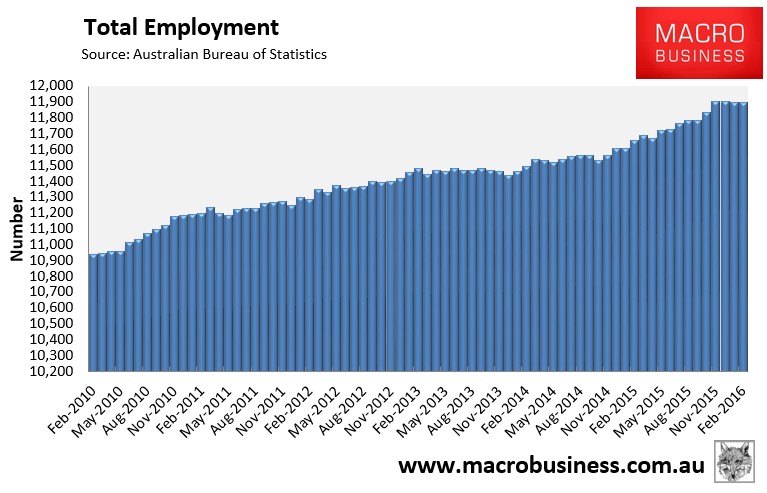

The trend in total employment has flattened after October’s and November’s numberwang:

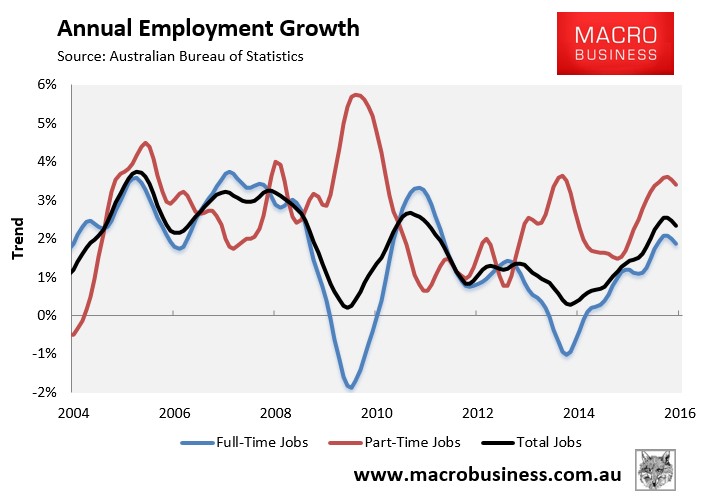

Annual employment growth has begun to soften and is being driven mostly by part-time employment:

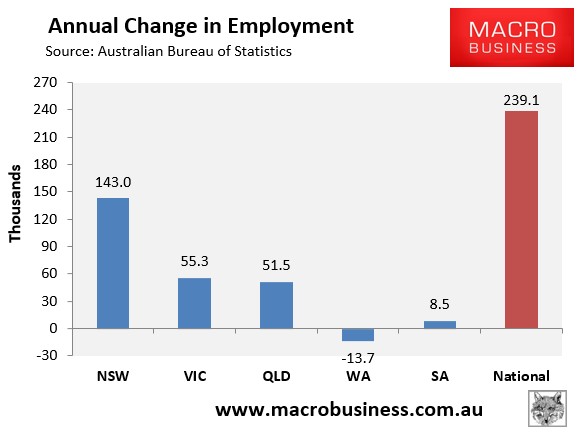

The housing bubble epicentre of New South Wales (Sydney) continues to drive jobs growth, accounting for 60% of total new jobs nationally over the past year in seasonally adjusted terms, whereas Western Australia is going backwards (see next chart).

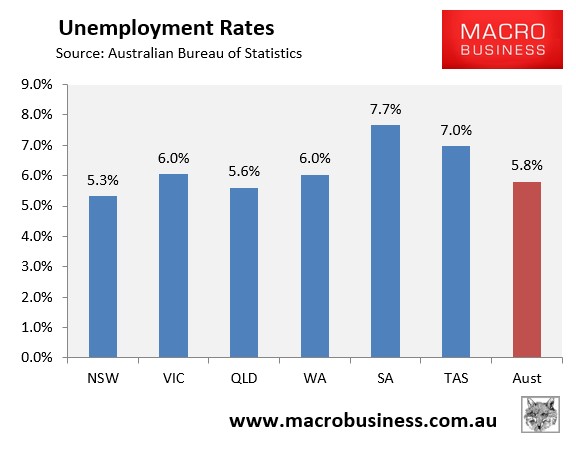

And South Australia and Tasmania continue to have the highest seasonally adjusted unemployment, whereas New South Wales (Sydney) is again leading the nation (see next chart).

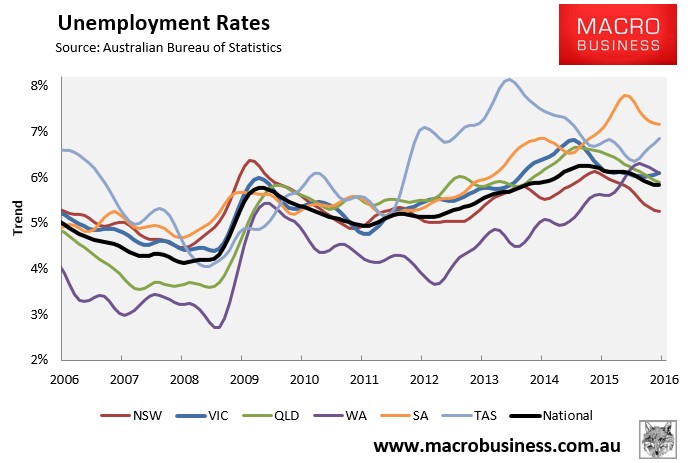

The state seasonally-adjusted figures are notoriously volatile and subject to a big margin of error. As such, the below chart shows the ABS’ trend unemployment rates, which again shows the bubble epicentre of New South Wales with by far the lowest unemployment, South Australia and Tasmania with the highest, Queensland with average unemployment, and Victoria and Western Australia with above-average unemployment:

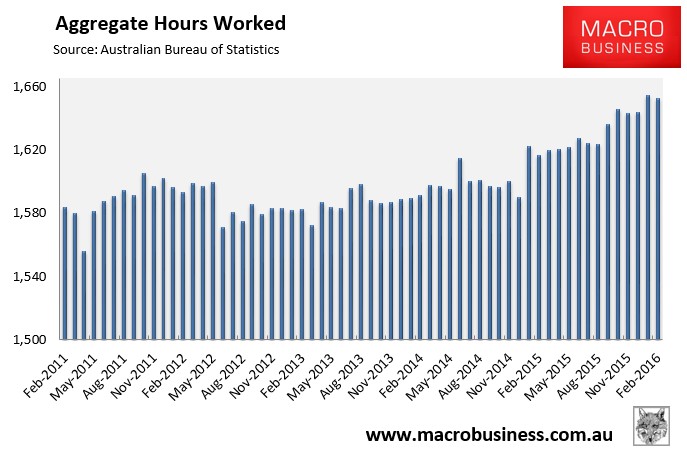

The aggregate number of hours worked fell in seasonally adjusted terms in February (down 2.0 million hours or 0.12%). However, hours worked have risen by 2.2% over the past year, which is above the growth in the population:

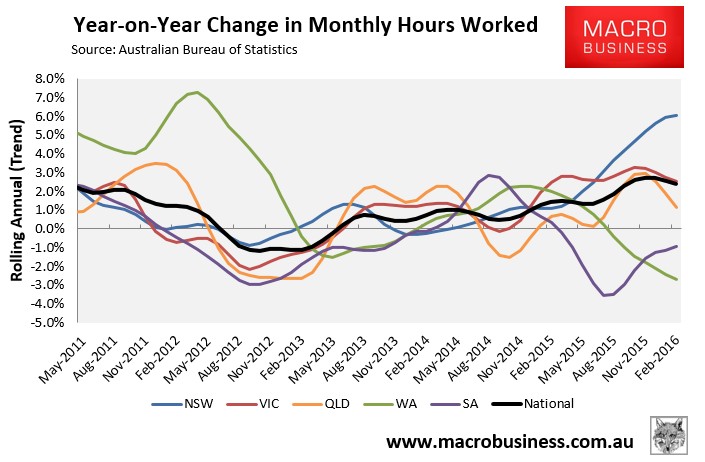

The below chart, which tracks the changes in hours worked on a trend basis, again shows that New South Wales (Sydney) has driven the lion’s share of this growth, with Victoria and Queensland also experiencing positive growth. By contrast, South Australia and Western Australia remain in the gutter, but with diverging trends:

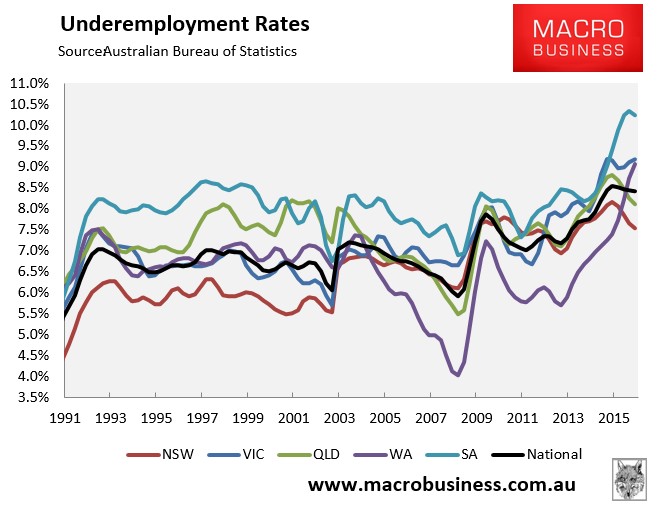

Underemployment remains near record highs in February at 8.4% nationally, but with significant divergence between the states:

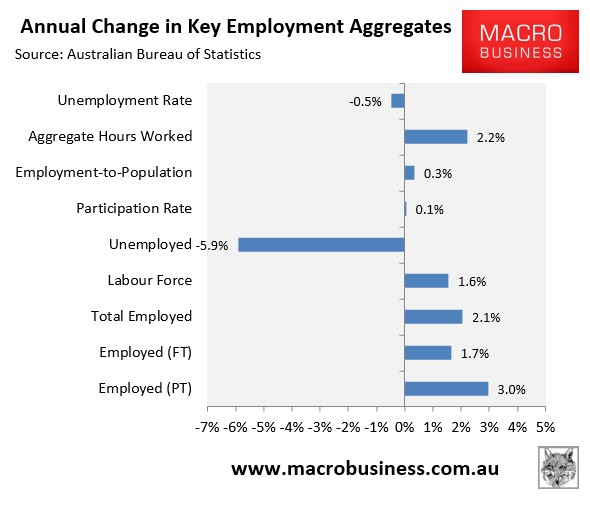

Finally, to round things out, the next chart summarises the annual change in the key employment aggregates on a seasonally-adjusted basis, which shows the solid improvement over the year:

Nothing has changed to the outlook following this release. The housing-induced boom in employment has continued, but will likely reverse in the second half as dwelling construction and prices begin to fall, coinciding with the ongoing contraction of mining investment and the closure of the car industry from late in the year.

unconventionaleconomist@hotmail.com