In our view, there continues to be risk to consensus loan loss forecasts in FY16E, primarily from higher collective provisioning, single-name exposures, and “pockets of weakness” in the Australian and New Zealand economies. With this in mind, we highlight last week’s statement from the RBA in its Financial Stability Review that the”near-term risks for residential property developers have increased, with a mismatch between a growing supply of geographically concentrated apartments on the east coast and concerns about softening demand for these apartments in some areas”.

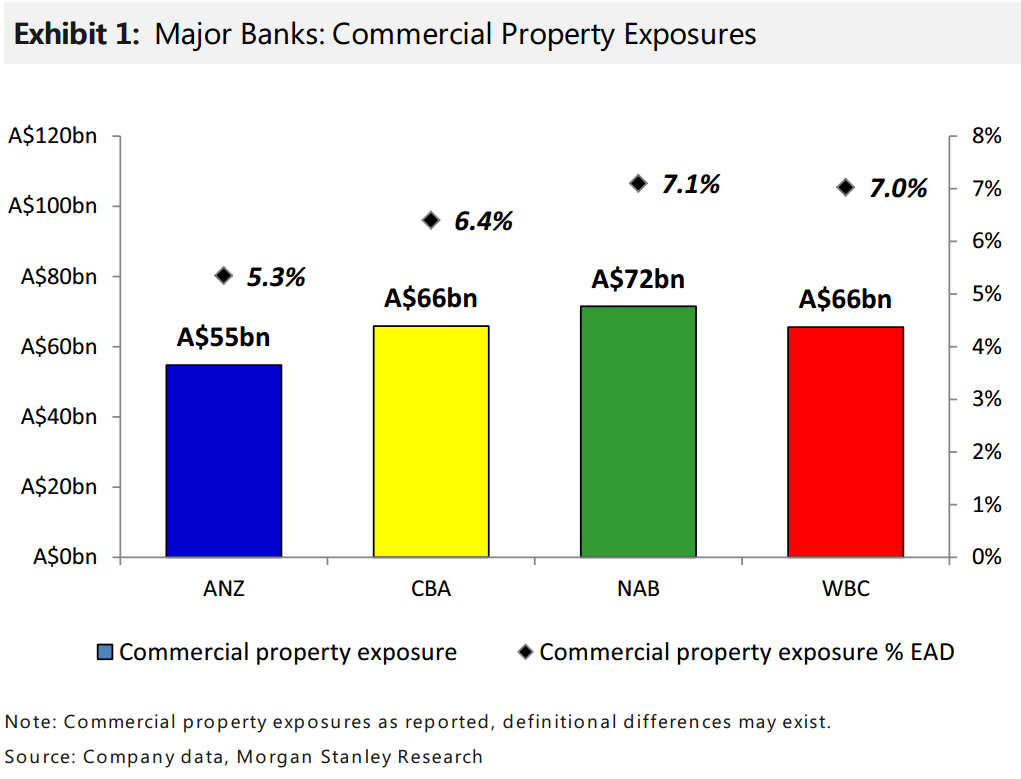

Our Chart of the Week shows that the major banks’ exposure to commercial property is ~A$260bn, or an average ~6.5% of total group exposures (ANZ: ~5.3%; CBA; ~6.4%; NAB: ~7.1%;WBC: ~7.0%). Furthermore,exposure to the residential segment is ~A$44bn or ~17% of total commercial property (ANZ: ~22%; CBA; ~18%; NAB: ~11%;WBC: ~20%). We also note the following: (1) ANZ has the least exposure to commercial property at ~A$55bn or ~5.3% of group exposures,and its Australian portfolio grew ~6.5% in FY15; (2) NAB has the most exposure to commercial property (~A$72bn or ~7.1% of group exposures) and its residual UK exposure has run down to ~A$1.5bn; (3) WBC discloses that ~56% of its commercial property borrowers have exposures >A$10m, with ~20% of these loans being to developers, ~45% to investors and ~35% to diversified property groups and trusts; (5) only ~A$420m or ~0.64% of WBC’s portfolio was impaired at FY15; (6) all else equal,a 50bp increase in commercial property loss rates would reduce our FY17E cash profit forecasts by an average of ~3%, ranging from ~2% at CBA to ~4% at NAB; (7) a 50bp rise in loss rates on the residential segment would reduce earnings by ~0.5% at each bank.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.