Australian retail sales growth slowed in early 2016. That slowdown might be seen by some as overdue given that Australian retail sales growth has outperformed relative to underlying income growth for some time now. In fact, in 2015 Australian retail sales growth was comfortably outperforming the post-GFC average.

But the Australian economic environment remains a challenging one. The slowing in China’s economy continues while lower commodity prices mean that resources construction projects in Australia will continue to wind up (without being replaced) and act as a major drag on growth for at least another year to come. Given the magnitude of the downturn seen in commodity prices and still underway in resources construction, Australia’s economy has shown strong resilience, but it has nevertheless taken a toll on national income growth.

It is against that backdrop that the Reserve Bank announced its latest interest rate cut in early May. While the initial response from consumers was positive – consumer sentiment jumped in May – retailers may want to take a cautious approach to the outlook. Many of the challenges to the Australian economy to which the Reserve Bank is responding are also challenges for retail. Retail sales growth has been able to outstrip growth in income largely due to the willingness of consumers to run down their savings, assisted by a house price boom which provided a big boost to the housing wealth of many consumers. In addition, a boom in housing construction has encouraged spending on consumer durables, while a fall in petrol prices had diverted some income from petrol retailers to other retailers.

The difficulty now facing retailers is that many of those supports are temporary, so the one-off boosts that supported retail spending are likely to fade. After an extended period of low interest rates, there are increasing question marks about the sustainability of the cheap credit-wealth channel and, despite another rate cut, neither housing prices nor the pace of housing construction are likely to be quite as powerful drivers in the next few years.

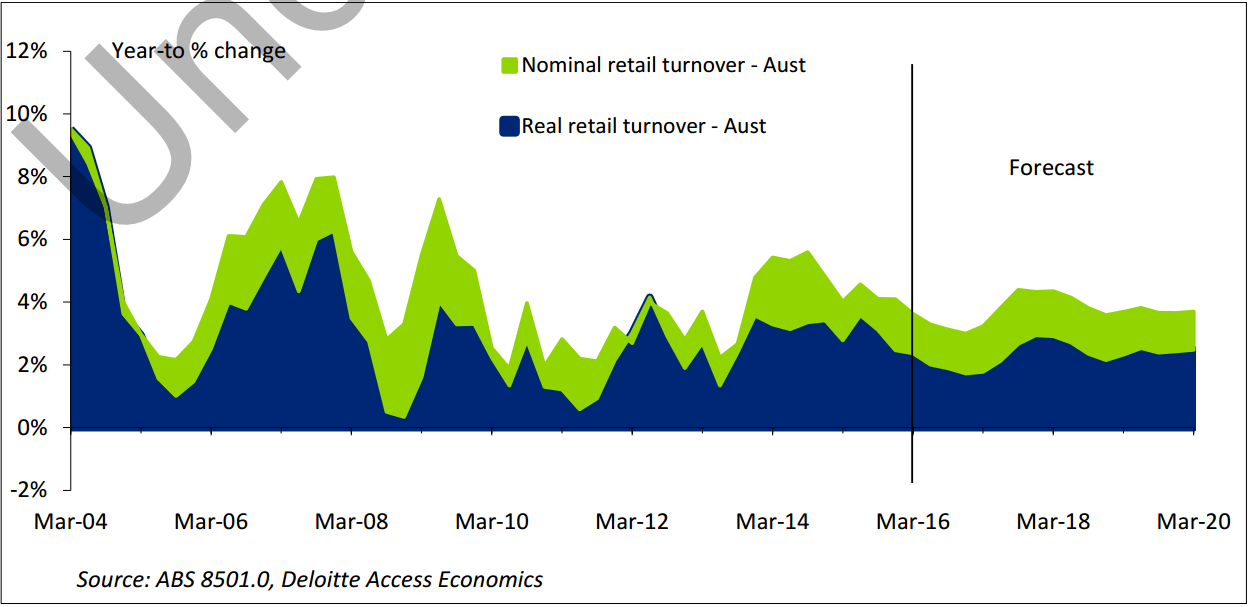

Meanwhile, the challenges to income growth are continuing with wage growth remaining at record lows. That is why retail sales growth is seen as slowing further through the course of 2016 (see Chart 1).

Macro environment

Global growth is doing OK, but not much more than that: there’s little incentive for many businesses to invest in new industrial capacity, both because China has built too much new capacity for many years now, and because global growth simply doesn’t support much increased capacity. And although many nations – everywhere from the US to China and here in Australia – are looking for consumers to fire up their economic prospects, those consumers are too indebted and too cautious to splash out too much.

Australia continues to swim strongly against the global tide, shrugging off a tricky trio (China’s slowdown, rotten commodity prices and a fast fading resource construction boom) to show some resilience in economic growth. But the pressures of the moment are set to linger with China’s transition to last for years, and low commodity prices meaning that the next couple of years will be characterised by a further slowdown in capex. Finally, some of the boost from lower interest rates may lose a degree of potency because housing construction and housing prices may soon peak. In short, the Australian economy isn’t quite yet ready to slip the leash, with the pace of Australia’s growth set to stay modest in the short term.

Retail sales to date

Retail sales growth slowed to 3.6% over the year to March 2016 (in nominal terms). For some time now, retail sales growth has outpaced lacklustre underlying income growth being supported instead by factors such as interest rate cuts and rising housing wealth. The strength in retail is being driven by non-food retailing with clothing retailers and department stores the standout sectors in early 2016. Sales growth for clothing retailers has now overtaken that of household goods retailers where sales growth has moderated as the housing cycle starts to cool. Food retailing continued to be subdued in early 2016. The outlook for retail sales Retailers will be hoping that the Reserve Bank’s rate cut in early May will help to revive the support for retail spending provided by lower interest rates, including the spillovers to retail sales from a strengthening housing market. But having already witnessed a surge in housing prices and consumer durables spending there are doubts as to how much longer the cheap creditwealth channel can be sustained. That channel is looking increasingly fragile with housing valuations looking stretched and the likelihood that both domestic and foreign investors slow their rate of investment into Australian property. Meanwhile, the headwinds to Australia’s economic growth continue with China’s economy slowing and resources construction set to fall further in 2016-17. These challenges mean that a recovery in underlying income growth is unlikely to be immediate, and retail sales growth may be lower in 2016-17.

Overall, real (inflation-adjusted) retail sales growth was 3.3% for 2014-15. After that strong outcome, we see retail sales growth slowing to 2.5% in 2015-16 and 1.9% in 2016-17.

State by State

Retail sales growth across the States is continuing to be marked by a two-speed split. The jurisdictions of NSW, Victoria, South Australia, Tasmania and the ACT are outperforming, assisted by booming housing markets in the case of NSW and Victoria. Meanwhile, the jurisdictions most exposed to the downturn in the resources sector (Queensland, Western Australia and the Northern Territory) are continuing to underperform the national average. But the likelihood is that housing markets will be less of a positive for retail going forward meaning that retail sales growth may slow elsewhere through the year ahead, particularly in NSW and Victoria.

With the capex triple-header, rating downgrade and falling terms of trade, the economy will be especially dependent upon a troubled consumer for growth in 2017…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.