Markets are a dear in the Brexit headlights and you can’t really blame them. How do you discount a referendum with such binary outcomes? The US dollar was weak:

But yen is off to the races while euro sits uselessly awaiting its death knell:

Advertisement

Commodity currencies roared on an oil snap back:

Gold recovered some Jo Cox losses:

Brent oil ripped out of its funk:

Advertisement

Base metals yawned:

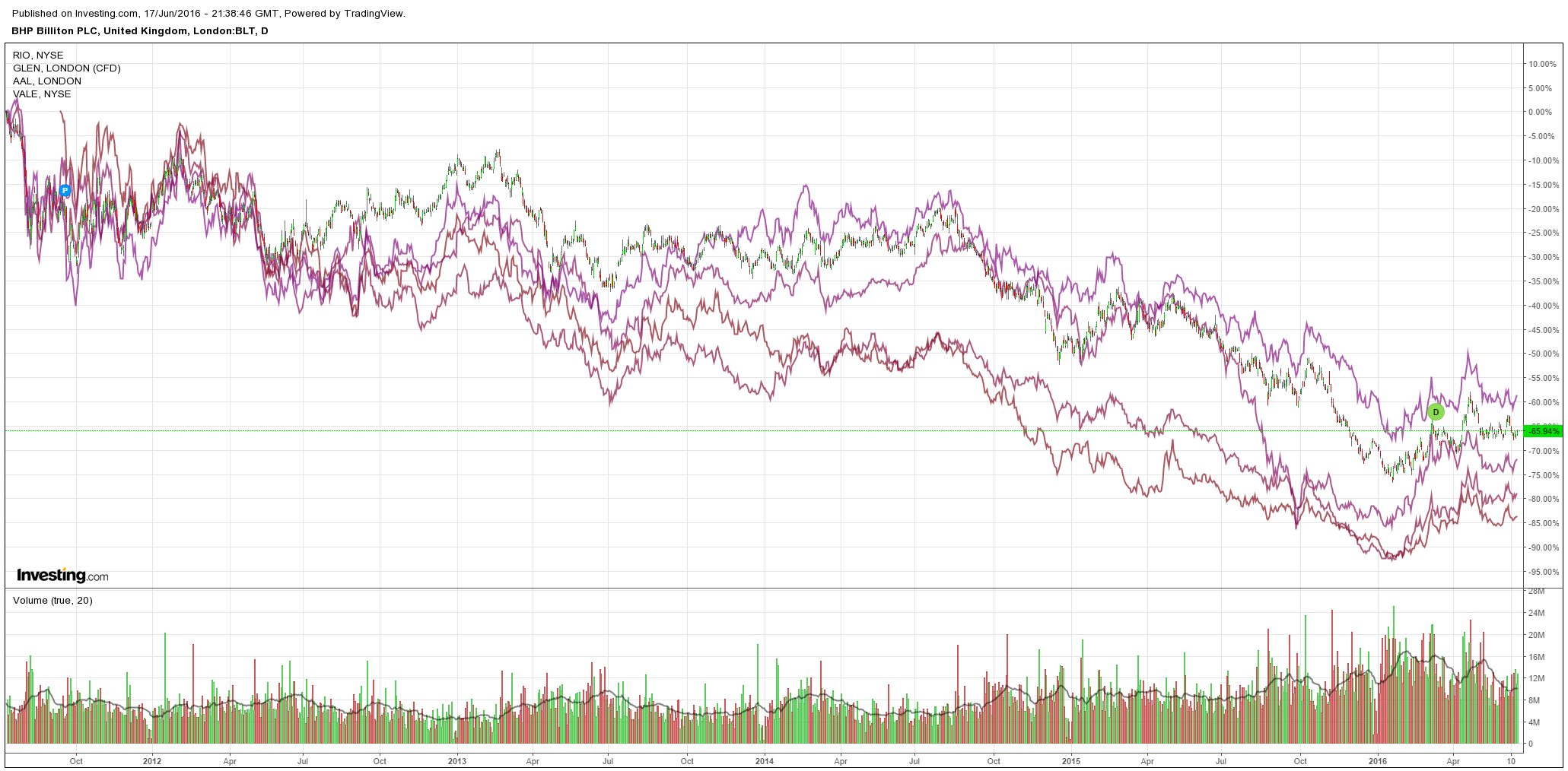

Big miners roared stupidly:

And high yield EM and US debt was firm but has clearly lost momentum well short of previous rebound highs:

Advertisement

Morgan Stanley sums up the outcome:

Scenario framework for MSCI Europe in event of BREXIT

PE framework. MSCI Europe’s N12M PE is 14x today and has averaged 15x over the last 3M. This compares to our expectation of a 5-10% rally if the UK votes to remain in the EU. The median reading since 1987 is 12.9.

Base case: We assume a 15% drop in N12M PE which would imply a move down to 12.8 from its L3M average.

Bear case: A 20-25% drop in the N12M PE would imply a move down to c. 12x – still materially above the single-digit lows seen during 2011/12.

EPS framework. Historically, European earnings have generally declined by 30-40% during recessions, although their current depressed level suggests a similar outcome from here would be unlikely.

Base case: We assume a 5-10% drop in EPS reflecting a slowing of economic activity and downward pressure on Financials profits (that still account for 30% of the market). FX weakness would be likely to provide some modest support to EPS over time. This assumption is smaller than the 11% decline in EPS seen during 2011-2012.

Bear case: We assume 15-20% drop in EPS based on our economists’ forecast for deeper GDP slowdown under their ‘severe stress’ scenario

MSCI Europe

The base case view is of a vote for the UK to remain in the EU, and a resulting stock rally. In the tables below MS applies its expected price moves in bull, base and bear scenarios against the underlying index’s average price level over the last 3 months (note the numbers are virtually identical if compared versus L6M). For example:

MSCI Europe is currently 4.5% below its L3M average.

Hence, in the base case view that European equities would fall 15-20% under Brexit, this leaves a further 10.5% to 15.5% to go.

This implies an index range of between 1070-1137 for MSCI Europe versus the current level of 1278. In the event of a vote to remain MS assumes a 5-10% relief rally. If this upside is applied against the L3M average then it implies upside of between 9.5% and 14.5% in the event the UK votes to remain in the EU. This is equivalent to an index level of between 1405 and 1472.

Impossible to position for so don’t. Look through it to underlying trends.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.