On Friday, the RBA released its August Statement on Monetary Policy (SoMP), which contained the below analysis of Australia’s dwelling construction pipeline:

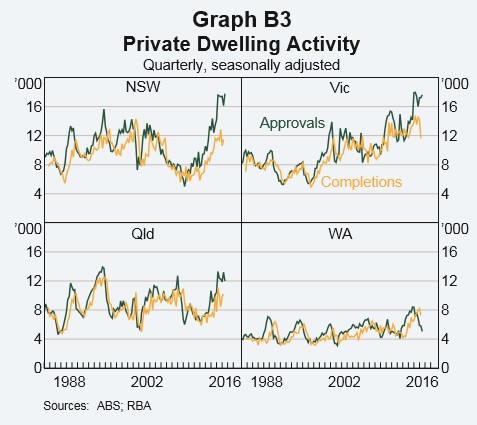

Since 2012, the supply of housing has increased in all Australian states, but activity has been concentrated in the four largest states of New South Wales, Victoria, Queensland and Western Australia, which together account for more than 90 per cent of Australia’s total building activity. Building approvals data suggest that there will be a further expansion of supply in these states over the next year or two (Graph B3).

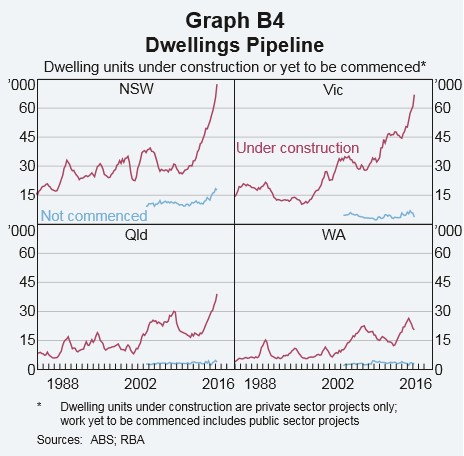

The number of newly approved dwellings has been above completions for some time, leading to a build-up in the pipeline of work yet to be done to historically high levels. In part, this reflects a shift in the composition of approvals towards higher-density dwellings, which typically take longer to complete than detached dwellings. This build-up in dwellings under construction or yet to be commenced is particularly apparent in New South Wales and Victoria (Graph B4).

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.