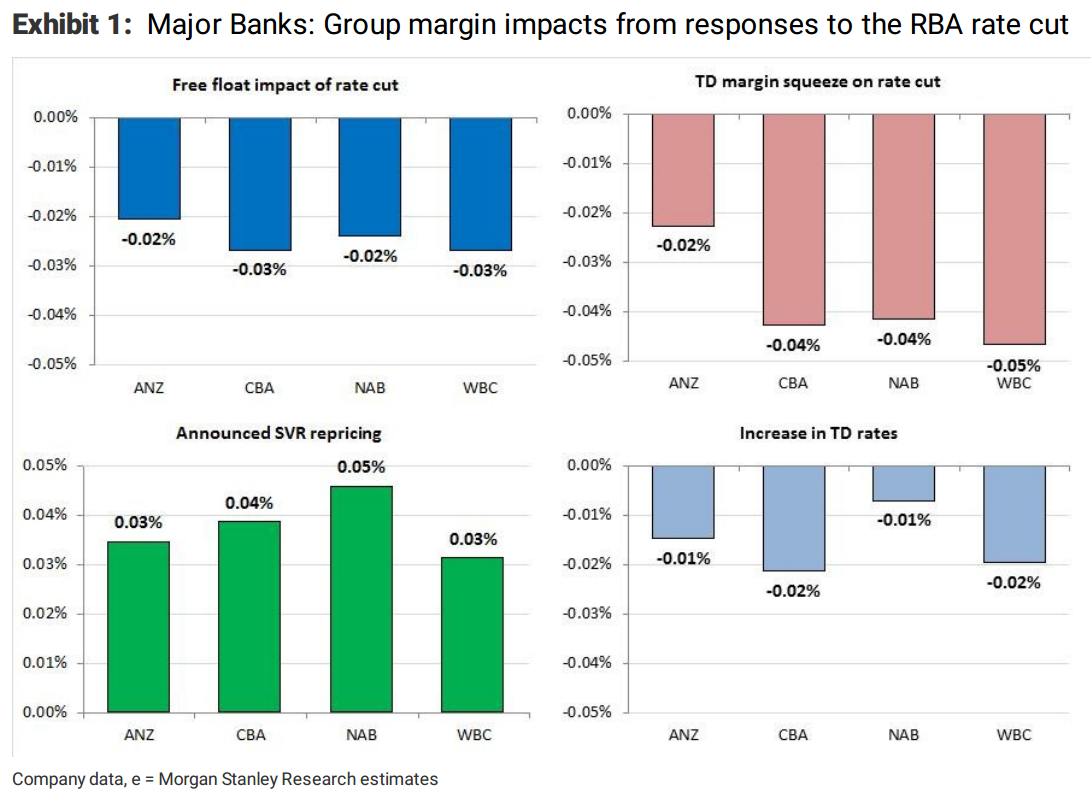

The major banks have responded to the RBA’s 25bp rate cut by: (1) re-pricing home loan standard variable rates (SVRs) by ~12-15bp; (2) increasing rates for >1yr term deposits (TDs) by 45-75bp (although NAB raised 8-month TD rates by 85bp); (3) re-pricing business SVRs by 12-15bp. With this in mind, our Chart of the Week shows the full-year effect on margins from: (1) the stand alone “free float” impact from the 25bp rate cut; (2) a 25bp “squeeze” on margins for all Australian TDs; (3) the SVR re-pricing announced today;and (4) the increase in rates on >1yr TDs.

We highlight that: (1) NAB is the biggest beneficiary of today’s SVR re-pricing, but our forecasts already assume 15bp of re-pricing by all of the banks in August and February (refer Australia Banks:Falling Margins (17 Jul 2016)); (2) we expect use of differentiated re-pricing for mortgage products (OOLvs IPLand P+I vs IO) will become more common; (3) the decision to increase rates on >1yr TDs likely reflects the need to meet net stable funding ratio (NSFR) requirements in 2018; (4) one more RBA rate cut and some TD margin squeeze are included in our forecasts, but we see downside risk from a resumption in the “war on deposits”; (5) margin headwinds are becoming more broad based and ANZ looks less vulnerable than peers; (6) we forecast an average of ~1bp margin contraction in FY17E (ANZ: +4bp; CBA -4bp; NAB -1bp; WBC: -2bp); (7)even with SVR re-pricing benefits, falling interest rates increase downside risk to the consensus estimate of “flattish” margins in FY17E; (8) in our view, ANZ needs margin expansion to mitigate the revenue headwinds from institutional bank “rebalancing”

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.