The state of the mining nation: who’s delivering the de-leveraging?

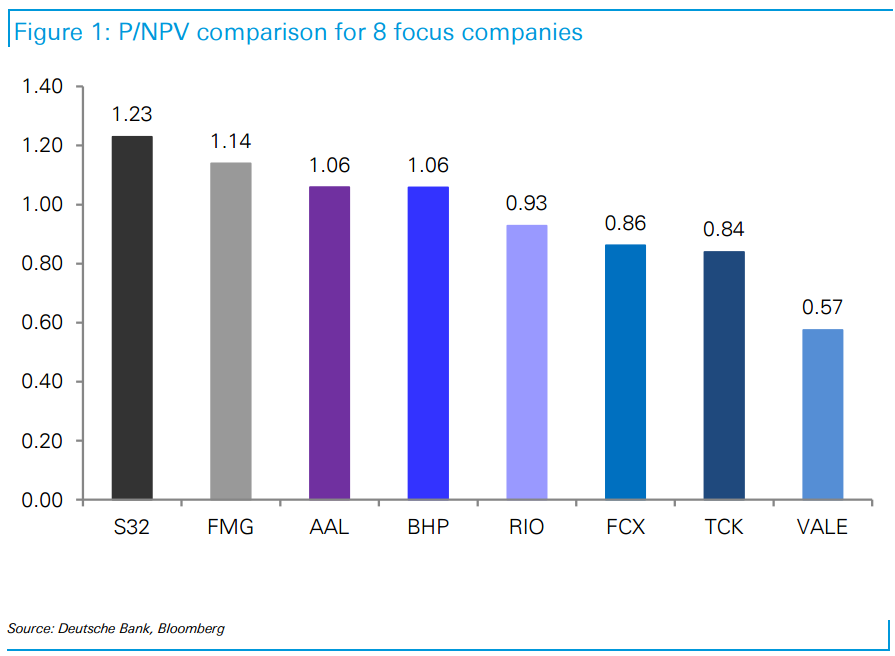

In this first of a series of reports looking at the key themes for the global mining stocks, we analyse the major diversified, iron ore and copper miners using both DB estimates and spot prices for NPV and four key metrics: (i) Net Debt/EBITDA, (ii) FCF generation and yield, (iii) EV/EBITDA, and (iv) div yield. Vale is trading at 0.6x P/NPV and has the highest financial leverage (3.9x ND/2017E EBITDA), conversely S32 is net cash and trading at 1.2x P/NPV. TCK, Vale and FMG have ~14% 2017E FCF yield with TCK and VALE +30% at spot. We have upgraded TCK to Buy with a recent share price decline, strong FCF potential and the ability to de-lever. RIO, Vale and FCX are also buy-rated.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.