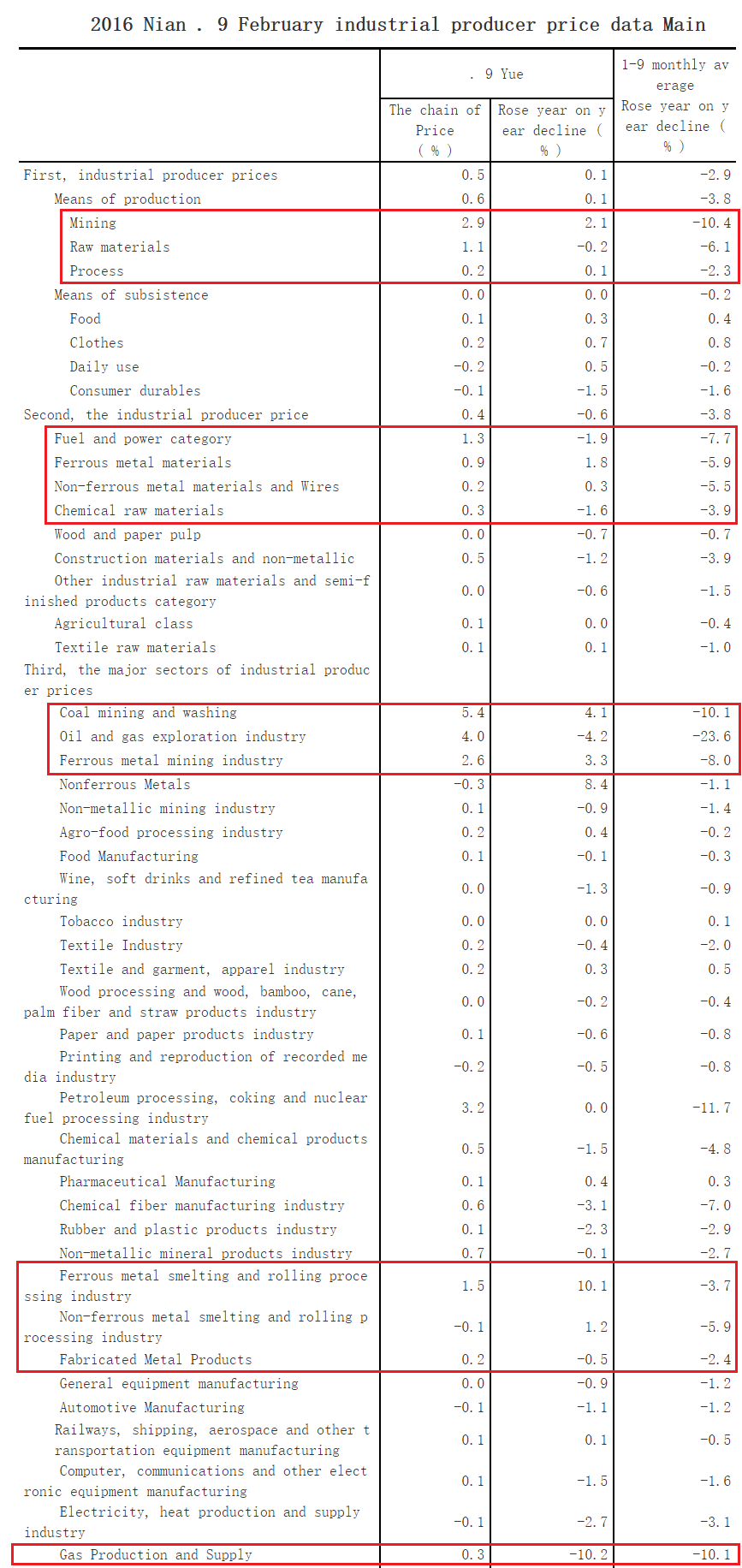

Friday night, commodity markets drew strength from China’s inflation numbers, especially iron ore futures which resumed their tear. The inflation numbers were remarkable, with a spectacular resurgence at the factory gate especially, into the positive in the first time for five years:

There is one very good reason to doubt that the rebound is either sustainable or will support commodity prices for very long. Here are the internals:

Note that nearly all of the inflation rebound is in primary commodity production or second stage processing of the same. If you break down the numbers you find that the turn in commodities themselves has an unweighted average of -7.7% year to date versus 1.5% month on month. By comparison, secondary and tertiary prices have turned from an unweighted average of -1.35% year to date to 0.1% month on month, and most of the gains are again commodity related sectors.

There are a few points to make about this:

- the PPI is going to keep rising just on the base effect. Year on year, the top ten commodity inflation sectors are up an average of 5.1%. Month on month they are rising 28% annualised!

- the great commodity reflation began in January so for Q4 we’ll see no change in the PPI base and by year end it will be running at roughly 4%. Even through Q1 the change to the base is minimal so the PPI is going to keep rising to perhaps 5%.

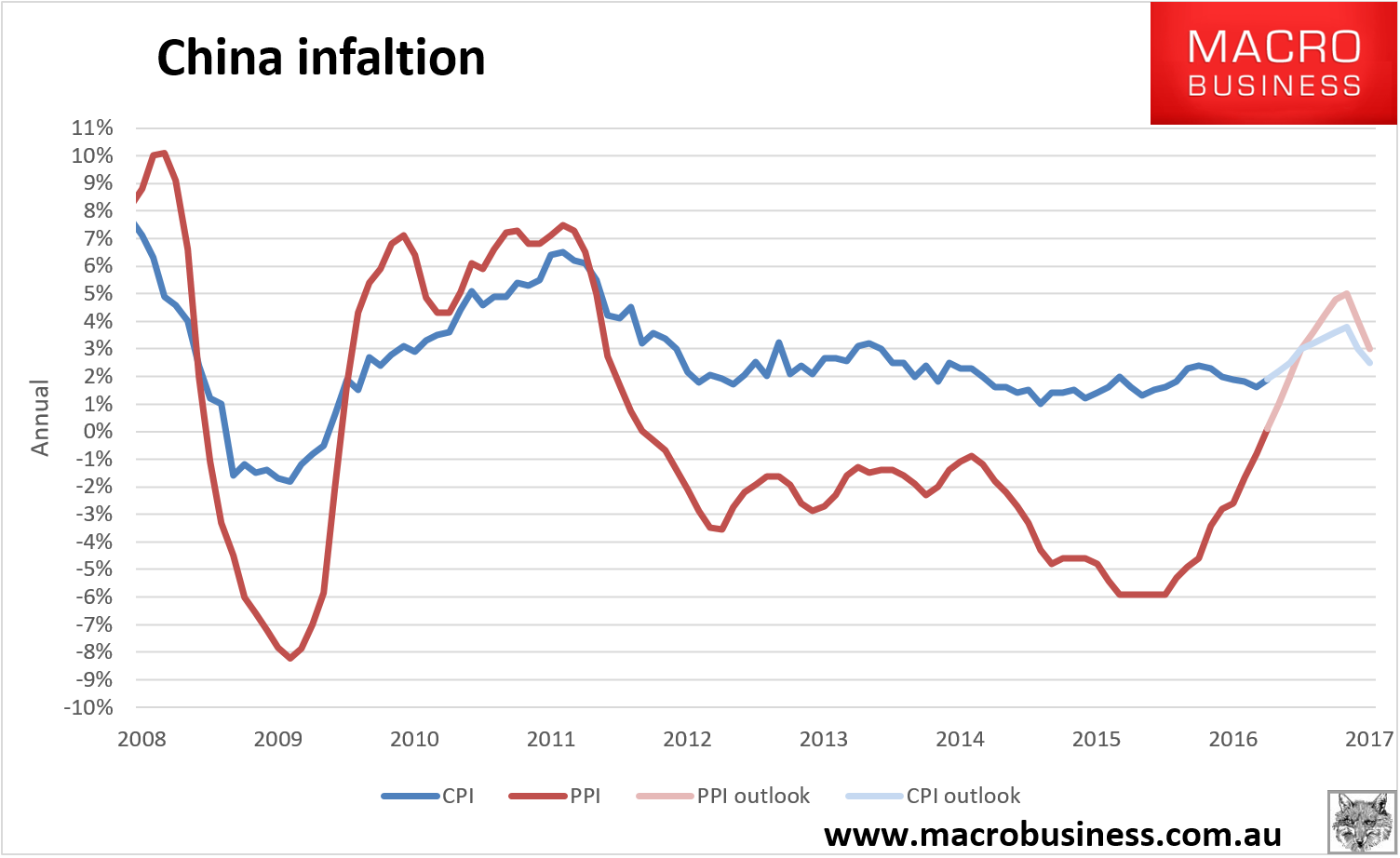

- moreover, based upon past relationships, the CPI is going to firm fast as well as coal prices hit the 75% of electricity production based on fossil fuels and input prices for agricultural chemicals drive up the all-important foodstuffs category. Here’s my best guess for where we’re headed on both:

In conclusion:

- most of these jumps are temporary, driven by coal, iron ore and oil. I expect they will have all peaked by year-end and begin to wash out from Q2 2017. Even so, until then, how will markets take this kind of inflationary burst as it continues through the pipeline? The PBOC is already leaning hard on the housing bubble and the pressure to tighten will increase sharply. It is a bad Chinese contribution to global bond and equity prices already under pressure from central bank yield steepening globally;

- second, if Friday night’s iron ore action is indicative of the drivers for commodity price rises now, then they are rising because they are rising (as opposed to end-user demand) which is never a great signal for where a market is headed.