Cross-posted from The Conversation:

Australian Treasurer Scott Morrison recently suggested the Reserve Bank of Australia (RBA) avoid cutting interest rates below the current 1.5%. The Turnbull government’s “fiscal consolidation”, he said, was more important for stimulating the economy.

This is big talk, and to be anything close to credible it needs to be backed up by big policies.

Morrison is not alone among politicians wading into the current debate on interest rates. Republican presidential nominee Donald Trump has said US Federal Reserve Chair Janet Yellen “should feel ashamed” for keeping rates so low. US President Barack Obama and UK Prime Minister Theresa May have been more lucid, taking greater care to understand the tradeoffs that central banks face.

Debate is certainly warranted. Negative interest rates were widely considered “impossible” just a decade ago, yet today they are the norm for OECD countries. If they are here to stay then serious reforms will be necessary to keep capitalism working.

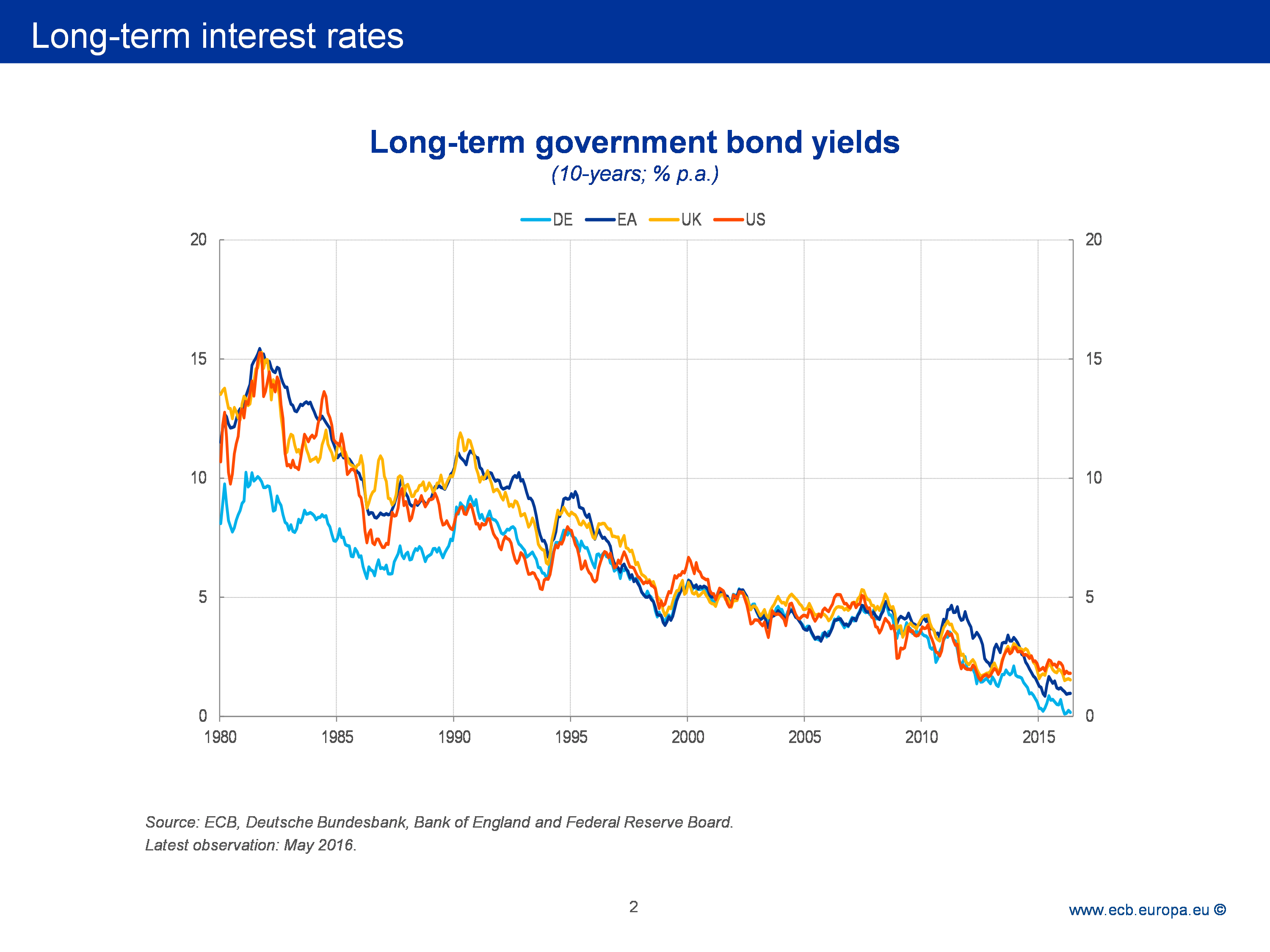

Australia, so far, remains an outlier. The RBA’s rate of 1.5% may be a record low on our shores, but it is enviably high compared to most of the OECD.

But as Australia faces the end of the mining boom, the end of a housing boom, and the end of car manufacturing and gas-intensive manufacturing, downward pressure on growth and interest rates is building.

To counter this, Morrison must offer a credible way of avoiding further cuts in Australia.

Excess savings

Interest rates are low across the OECD due to excess savings. This is the same problem that caused prolonged unemployment during the Great Depression.

Imagine the world spontaneously decided to save 10% more of its income in 2017. As the year progressed, demand for goods and services would collapse. Businesses would find their warehouses packed with unsold goods and their staff under-utilised. They would be forced to lay off workers and halt production. Spooked investors would be unwilling to expand businesses, build housing, or invest in production. Asset prices would collapse, many debts would become unpayable, and the resulting financial crisis would further cut into employment.

In turn, high unemployment would feed back to further reduce demand. The negative feedback between employment and demand would send the economy into a downward spiral. During the Great Depression, US industrial output shrank by an astounding 50% and unemployment reached 25%.

What sends savings higher in the first place?

Both the Great Depression and Great Financial Crisis were triggered by asset bubbles. When the bubbles burst, savings increased rapidly while investment plummeted, due to negative expectations (which increase savings for the coming hard times), financial instability (which leads people and companies to hold on to their money rather than lend it to potentially insolvent others), and high levels of debt (which increase savings to pay down debt).

The role of monetary policy

Interest rates are so important in this story because they affect the rate of savings and investment – they reward savers and cost investors.

Higher interest rates increase the incentive to save and reduce the incentive to invest. They will tend to cool the economy. Lower interest reduce the incentive to save and increase the incentive to invest, and tend to heat the economy up.

The role of central banks is to set monetary policy to what is termed the “neutral” rate of interest. This is the rate that keeps the economy running at its full potential, by balancing intentions to save and intentions to invest – so that neither is in excess.

For this reason, central banks do not reduce rates “on purpose”, but follow the underlying neutral rate by using (roughly) the following formula:

- If unemployment is high and inflation is below target (usually around 2-3%), then there is spare capacity in the economy. Interest rates are above the neutral rate and should be lowered to heat things up.

- If unemployment is low and inflation is above target, then the economy is likely overheating. Interest rates are below the neutral rate and should be raised before inflation gets out of control.

Extremely low interest rates at OECD central banks are a symptom of current economic conditions, where too many people are saving and not enough people are consuming or investing.

Why is the “neutral” interest rate so low today?

The global neutral interest rate has actually been trending steadily downward since the 1980s. This is unprecedented in the history of capitalism, and its importance cannot be overstated.

Bank of England researchers identify several reasons behind this trend, each of which either increases intentions to save or reduces intentions to invest:

- growing inequality, which increases savings because the rich save more of their income

- an ageing population living longer, which increases lifecycle savings for retirement

- the growth of emerging markets, predominantly China, which have very high levels of savings

- the lower cost of capital goods, which reduces the capital outlay needed for the same investment

- reduced population growth, slowed productivity growth, and reduced public investment, each of which cut demand for new investment.

Together these trends towards excess saving have reduced the neutral rate by around 4% since 1980.

Importantly, we can be confident that most of these changes are here to stay. Low interest rates appear to be the new normal for advanced capitalist societies.

Can our government policies credibly keep interest rates higher?

Treasurer Morrison acknowledges that rate cuts are a “matter for the RBA”, and that his comments will have little influence on its decision making.

To actually influence the path of RBA interest rates, the Turnbull government must take actions that place substantially more of the load in boosting demand on fiscal policy (government spending). Given increasing government spending will further increase an already problematic budget deficit, such policies are only justifiable where their long-term benefits outweigh their immediate costs.

The Turnbull government’s policy in this area rests heavily on the proposed company tax cut of A$48 billion over the next ten years. Ordinarily such a tax cut might increase investment. But investment in the OECD has been disappointingly unresponsive to the kind of small change in profitability that the company tax cut will bring.

In the US, for example, investment remains low even while corporate profits are around record highs. Instead of investing, businesses are hoarding trillions of dollars in profits. This pattern is highly suggestive of monopoly-like rents being pervasive among larger corporations, in which case company tax cuts will only increase savings.

The pro-investment signal businesses really need is greater consumer demand for goods and services. Yet to fund company tax cuts, the Turnbull government is cutting back on the most effective of demand-boosting fiscal policies: welfare programs. Poorer individuals live closer to subsistence, so tend to spend most of the additional income they receive. Taking money from welfare and sending it to corporations risks increasing corporate saving while reducing consumer demand – the exact opposite of what is needed.

Given the cost to the ailing budget of A$48 billion, the proposed tax cuts are a waste of the Australian government’s minimal fiscal headroom. It is fortunate they will soon be blocked in the Senate.

Scott Morrison’s comments show some understanding of the challenges presented by the new low-rate era. The policies he promotes do not.

While Australia faces its greatest economic challenges in a generation, it seems we are still waiting for the greatest economic reformers in a generation to arrive.

Article by Reuben Finighan, Senior Research Officer at The Melbourne Institute and Fellow of the ARC Life Course Centre of Excellence, University of Melbourne

{kind=link}