Macquarie’s latest Chinese steel mill survey is out:

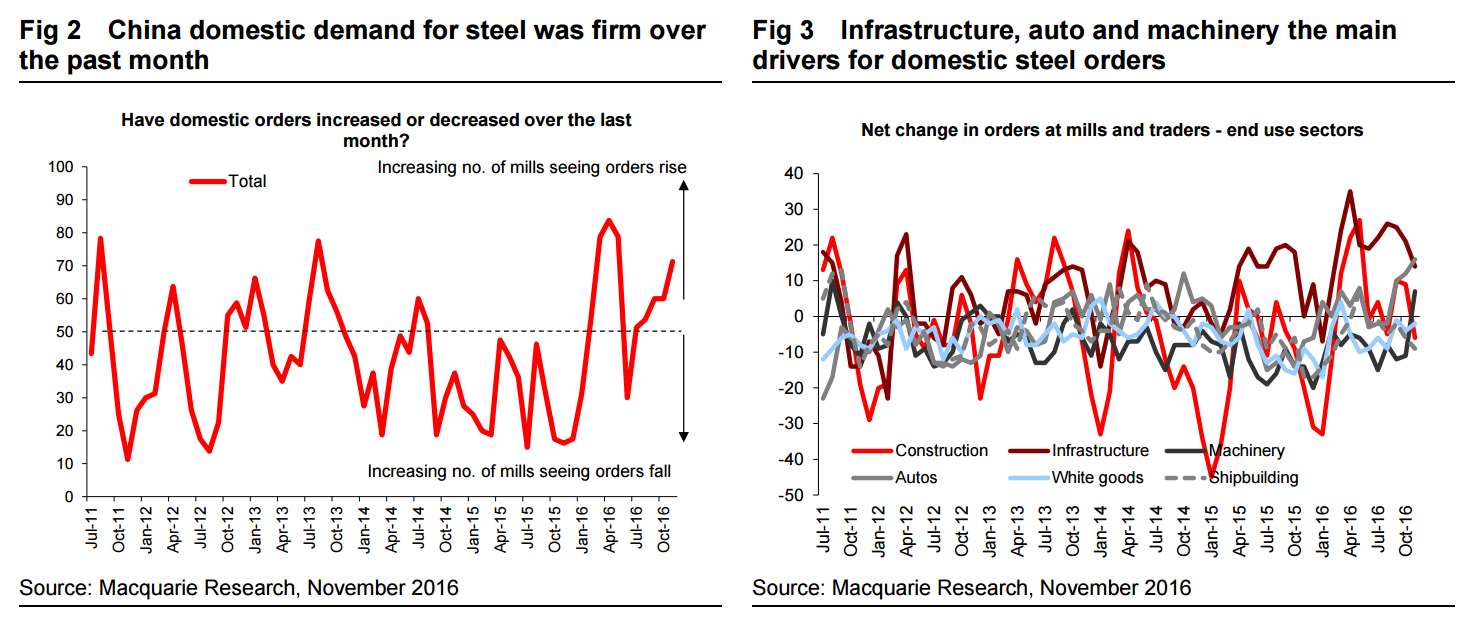

Our latest China steel survey shows a broader-based improvement in demand and sentiment, and indicates that raw materials demand will also remain robust. Sentiment towards the market improved in November, particularly from traders who were previously more cautious in October. Domestic orders improved over the past month for Chinese steel mills, and while property and infrastructure demand for steel has eased, a clear improvement in demand has been seen from machinery and autos. Both mills and traders steel inventory are stable compared with last month and standing at a comfortably low level.

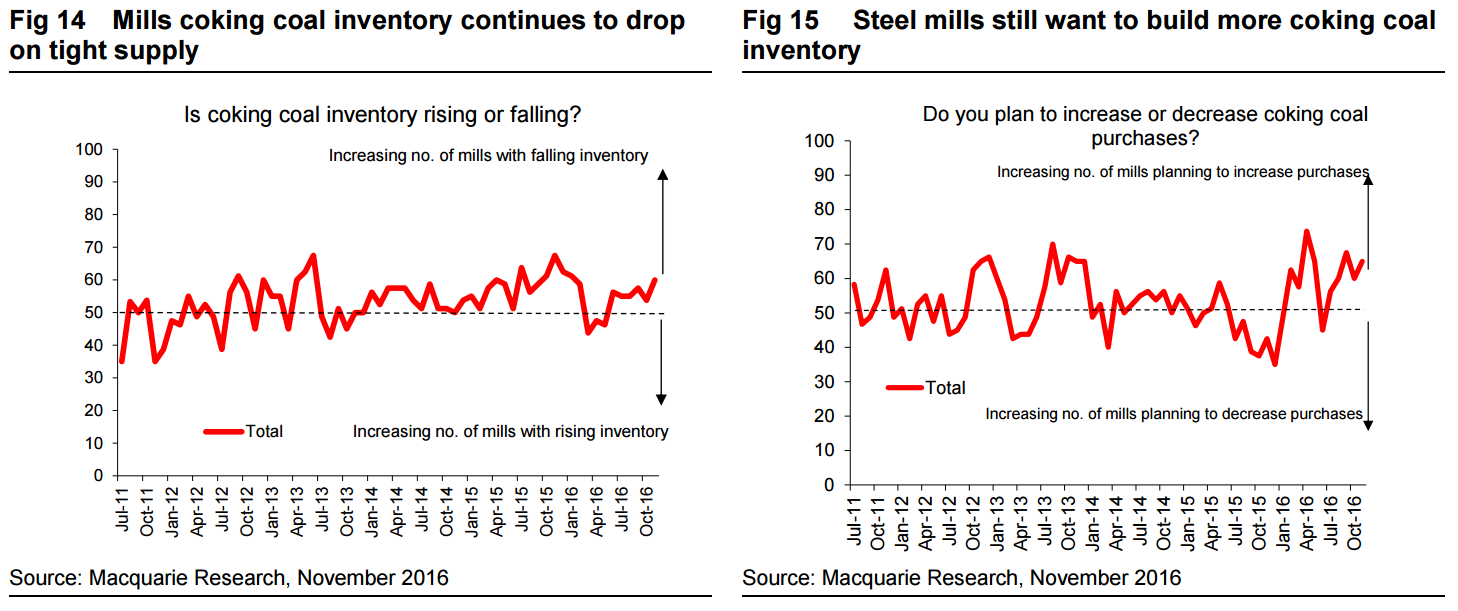

Steel mills continue to have interest to restock raw materials, but coking coal inventory continues to fall on tight supply while iron ore stocks are flat MoM. All these findings in our latest survey were supported by what we heard from our speakers on our latest China commodities trip last week in Beijing, Tangshan and Shanghai, where there was a clearly optimistic outlook toward the steel and raw materials market near term.

Unlike iron ore where mills managed to hold a stable inventory, Chinese steel mills have continued to draw on their coking coal inventory, as supply remains tight. Mills clearly have the desire to build more coking coal inventory but they seem to have failed over the past few months. This is in line with what we heard from steel mills in Tangshan last week that they don’t have much coke and coking coal inventory currently due to ongoing tight supply. Our coal speaker from SHCCE during the trip told us that among the 1,000 mines that has been allowed to switch back from “276” days to “330” days in October, 450 have some coking coal output, with a total unwashed capacity of near 900mt versus 2.39bn tons total capacity for all 1,000 mines.

We question the veracity of this number, as it is significantly bigger than the previous 789 mines that reportedly had 350~380mt of coking coal capacity, suggesting more coking coal mines were included in the latest batch of approved mines. However, our speaker warned that supply recovery in coking coal could be harder than thermal coal due to the complexity in coal types and also the share of SOE mines in the coking coal industry is lower than in thermal coal, and that private miners are more reluctant to bring back production on lack of confidence in government policy and coal prices for next year.

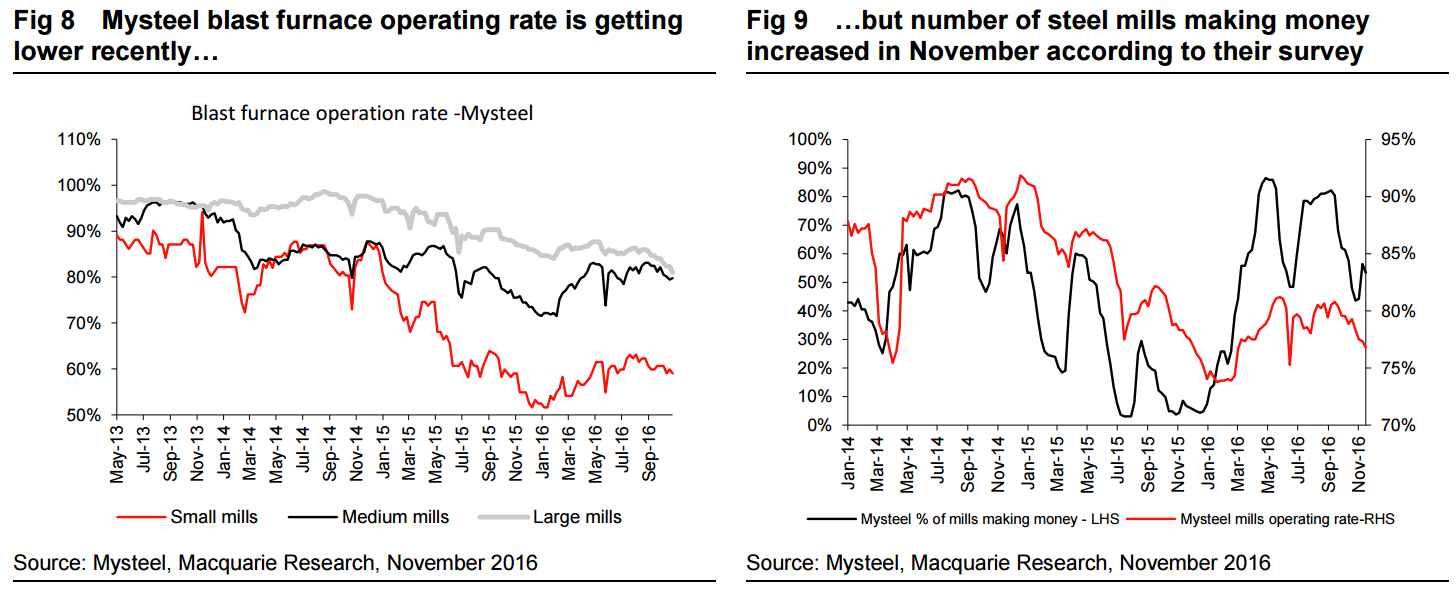

For me there are several warning signals that the bubble is on its last legs here. Although domestic demand is still good, construction is the key sector and it is coming off.

Second, with Chinese coking coal mines set to resume, deflation there is only a matter of time.

Third, we can expect all of these metrics to be partially inflated by speculative hoarding so none will be as good as they appear.

Advertisement

Macquarie sums it up for me:

Chinese bulk commodity futures resumed an upward trajectory on Tuesday on the news of further, more stringent environmental-related steel output cuts in Tangshan. In our view, while this is clearly helpful to steel prices, we still struggle to understand the Chinese investor logic that this is good for iron ore (given it inevitably means lower iron ore demand). The Steel Index 62%Fe iron ore price rose 5.7% on the day to $73.8/t, a level we fell is ~$15/t above what can be justified by current fundamentals. Meanwhile, with the excitement in commodity futures continuing, the SHFE has once more raised margins for copper, aluminum, zinc, lead, nickel, tin, rebar and HRC (from 8% to 9%) and raised the daily limit-up mark from 6% to 7%, effective from Thursday.

Precisely. Looking for reason here is pointless. It’s a bubble and will burst when it bursts.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.