The US dollar is running wild again. All other majors got caned:

Commodity currencies too:

Gold was monstered as expected:

Advertisement

Brent held on:

Base metals roared as the Chinese future bubble revived on iron ore:

Advertisement

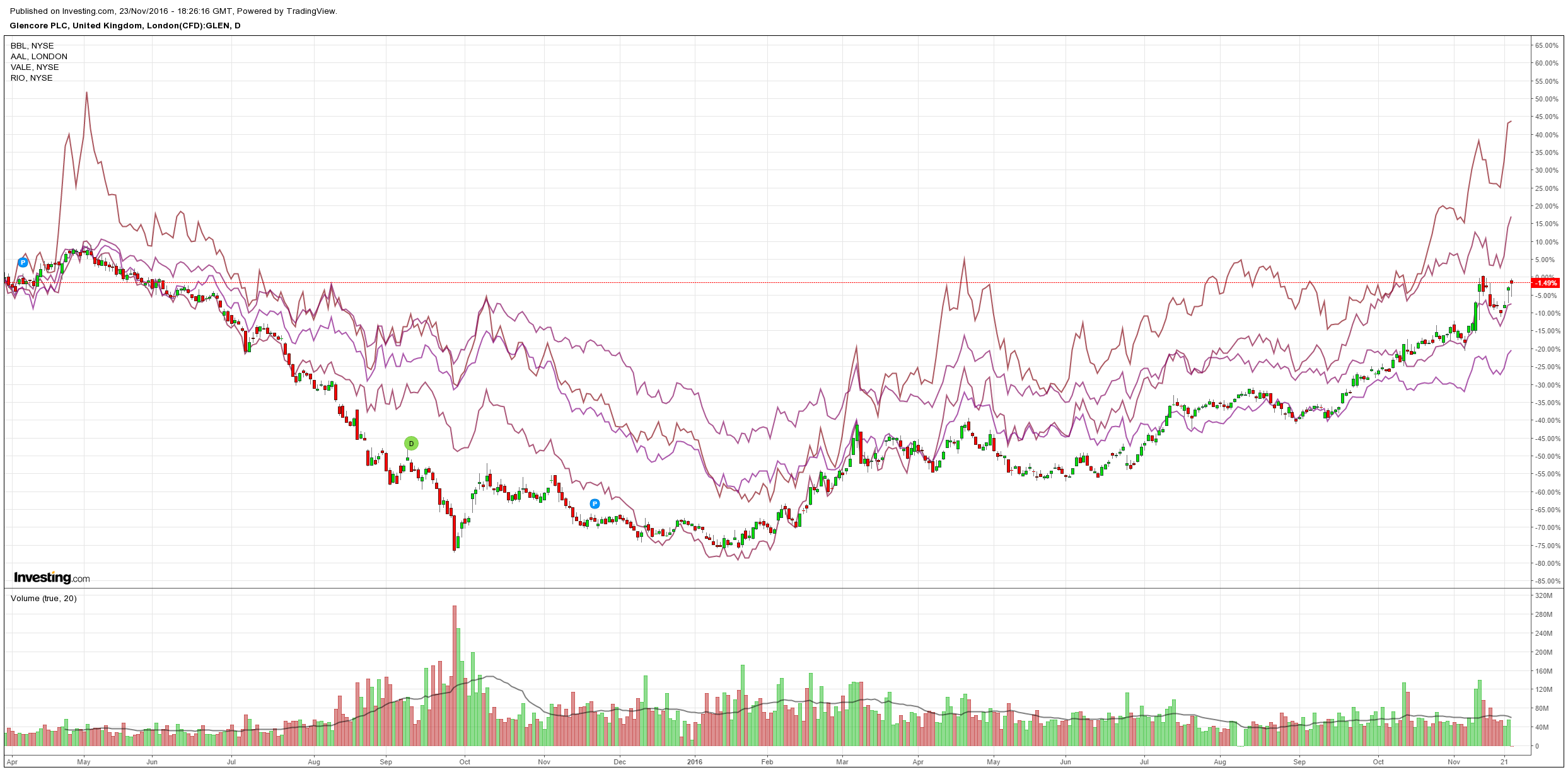

Miners rose:

EM and US high yield fell:

EM stocks rose:

Advertisement

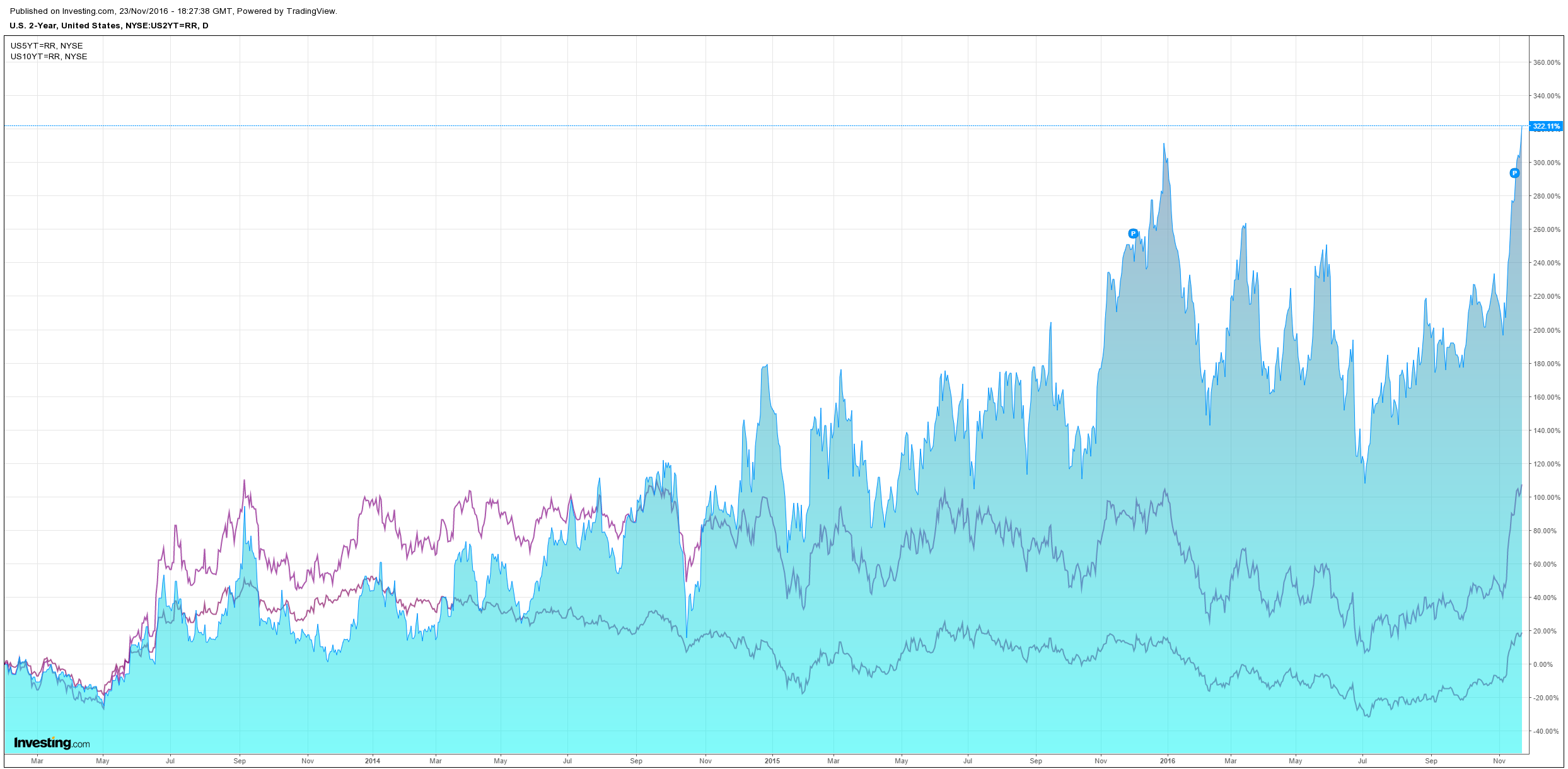

US bonds were flogged, the two year yield broke out but the curve flattened:

Stocks held their highs:

Advertisement

The USD remains the only game in town. The commodities rally will have to break at some point into this monetary headwind. As well, the US yield curve steepening is beginning to reverse which is indicting a short term bounce in growth and inflation only.

Fed minutes were the release dejour:

Most participants expressed a view that it could well become appropriate to raise the target range for the federal funds rate relatively soon, so long as incoming data provided some further evidence of continued progress toward the Committee’s objectives. Some participants noted that recent Committee communications were consistent with an increase in the target range for the federal funds rate in the near term or argued that to preserve credibility, such an increase should occur at the next meeting. A few participants advocated an increase at this meeting; they viewed recent economic developments as indicating that labor market conditions were at or close to those consistent with maximum employment and expected that recent progress toward the Committee’s inflation objective would continue, even with further gradual steps to remove monetary policy accommodation. In addition, many judged that risks to economic and financial stability could increase over time if the labor market overheated appreciably, or expressed concern that an extended period of low interest rates risked intensifying incentives for investors to reach for yield, potentially leading to a mispricing of risk and misallocation of capital. In contrast, some others judged that allowing the unemployment rate to fall below its longer-run normal level for a time could result in favorable supply-side effects or help hasten the return of inflation to the Committee’s 2 percent objective; noted that proximity of the federal funds rate to the effective lower bound places potential constraints on monetary policy; or stressed that global developments could pose risks to U.S. economic activity. More generally, it was emphasized that decisions regarding near-term adjustments of the stance of monetary policy would appropriately remain dependent on the outlook as informed by incoming data, and participants expected that economic conditions would evolve in a manner that would warrant only gradual increases in the federal funds rate.

In their discussion of monetary policy for the period ahead, members judged that the information receivedsince the Committee met in September indicated that thelabor market had continued to strengthen and thatgrowth of economic activity had picked up from the modest pace seen in the first half of this year. Although the unemployment rate was little changed in recentmonths, job gains had been solid. Household spendinghad been rising moderately but business fixed invest-ment had remained soft. Inflation had increased somewhat since earlier this year but was still below the Committee’s 2 percent longer-run objective, partly reflecting earlier declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation had moved up but remained low; most survey-based measures of longer-term inflation expectations were little changed, on balance, in recent months. With respect to the economic outlook and its implications for monetary policy, members continued to expect that, with gradual adjustments in the stance of monetary policy, economic activity would expand at a moderate pace and labor market conditions would strengthen somewhat further. Almost all of them continued to judge that near-term risks to the economic outlook were roughly balanced. Members generally observed that labor market conditions had improved appreciably over the past year, a development that was particularly evident in the solid pace of monthly payroll employment gains and the increase in the labor force participation rate. It was noted that allowing the unemployment rate to modestly undershoot its longer-run normal level could foster the return of inflation to the FOMC’s 2 percent objective over the medium term. A few members, however, were concerned that a sizable undershooting of the longer-run normal unemployment rate could necessitate a steep subsequent rise in policy rates, undermining the Committee’s prior communications about its expectations for a gradually rising policy rate or even posing risks to the economic expansion. Members continued to expect inflation to remain low in the near term, but most anticipated that, with gradual adjustments in the stance of monetary policy, inflation would rise to the Committee’s 2 percent objective over the medium term. Some members observed that the increases in inflation and inflation compensation in recent months were welcome, although a couple of them noted that inflation was still running below the Committee’s objective. Against this backdrop and in light of the current shortfall of inflation from 2 percent, members agreed that they would continue to carefully monitor actual and expected progress toward the Committee’s inflation goal. After assessing the outlook for economic activity, the labor market, and inflation, as well as the risks around that outlook, the Committee decided to maintain the targe trange for the federal funds rate at ¼ to ½ percent at this meeting. Members generally agreed that the case for an increase in the policy rate had continued to strengthen.But a majority of members judged that the Committee should, for the time being, await some further evidence of progress toward its objectives of maximum employment and 2 percent inflation before increasing the target range for the federal funds rate.

Advertisement

A few members emphasized that a cautious approach to removing accommodation was warranted given the proximity of policy rates to the effective lower bound, as the Committee had more scope to increase policy rates, if necessary, than to reduce them. Two members preferred to raise the target range for the federal funds rate by 25 basis points at this meeting. They saw inflation as close to the 2 percent objective and viewed an increase in the federal funds rate as appropriate at this meeting because they judged that the economy was essentially at maximum employment and that monetary policy was unable to contribute to a permanent further improvement in labor market conditions in these circumstances. The Committee agreed that, in determining the timing and size of future adjustments to the target range for the federal funds rate, it would assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment would take into account a wide range of information, including measures of labor market conditions,indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee expected that economic conditions would evolve in a manner that would warrant only gradual increases in the federal funds rate and that the federal funds rate was likely to remain, for sometime, below levels that are expected to prevail in the longer run. However, members emphasized that the actual path of the federal funds rate would depend on the economic outlook as informed by incoming data. The Committee also decided to maintain its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipated doing so until normalization of the level of the federal funds rate is well under way. Members noted that this policy, by keeping the Committee’s holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions.

December is go. Two hikes next year on that rhetoric. Bonds have further repricing ahead. USD too.