• The Annual National Accounts for financial year 2015/16 included revised estimates for business investment. Here we provide a brief recap of recent trends.

• In terms of the mining / non-mining investment picture there are a couple of key take outs.

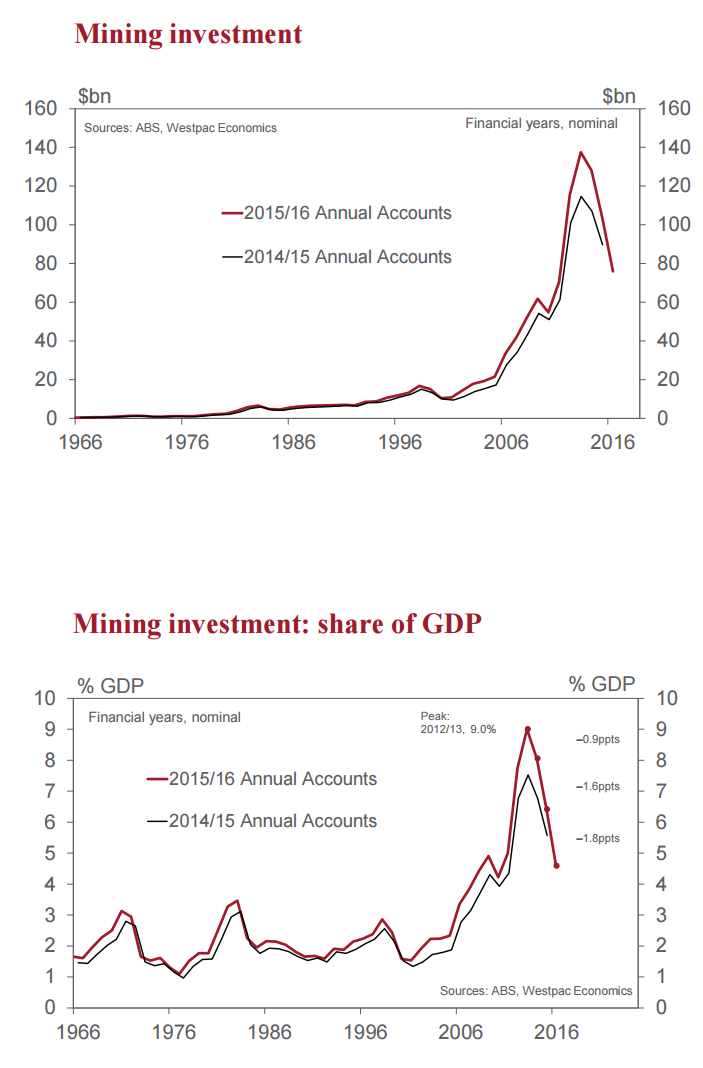

• The mining investment boom has been revised higher. It appears that some investment previously allocated to other industries has been reclassified.

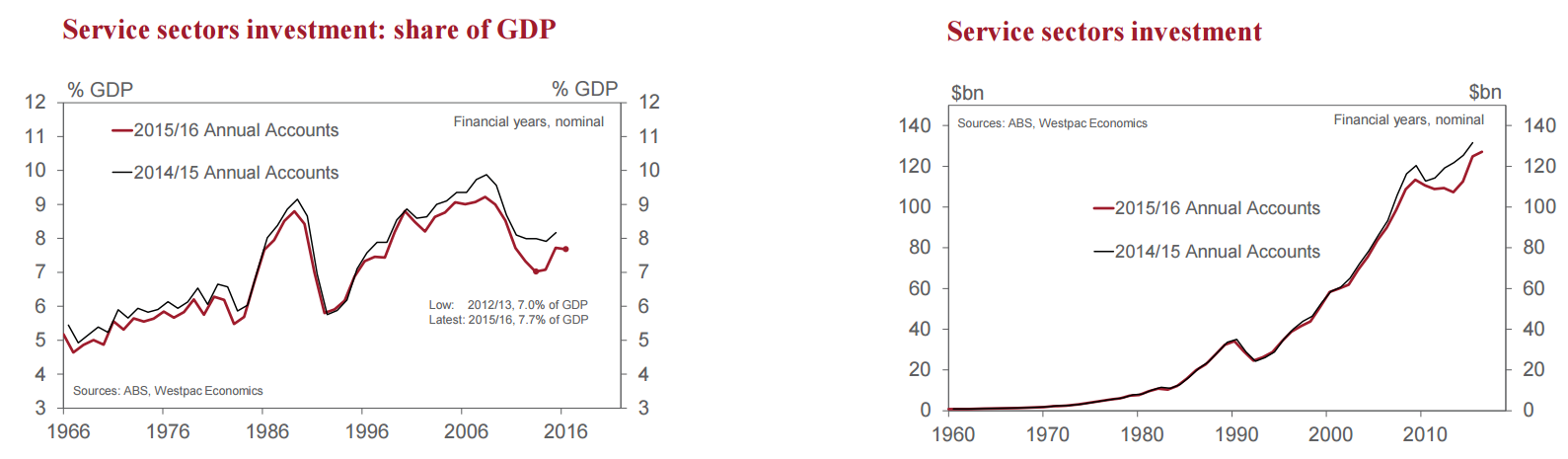

• Non-mining business investment has a more pronounced cycle over recent years.

Mining investment: The timing of the peak in mining investment remains 2012/13. In nominal dollar terms, mining investment climbed to a high of $137bn, upgraded by almost $23bn from the 2014/15 annual national accounts. As a share of the economy, mining investment peaked at 9.0% in 2012/13, upgraded from 7.5% – a rather sizeable revision. For the 2015/16 financial year as a whole, mining investment moderated to 4.6% of GDP. The end of the mining investment boom is in sight. Work on the remaining gas projects under construction is due to be progressively completed during 2017.

Services investment: Investment by the service sectors (covering 15 industry groupings) has been marked down in recent years. The largest downgrade, of over $14bn, is in 2012/13. Service sector investment now has a more pronounced recovery. In the two years to 2014/15 nominal growth is 5% and 11%, upgraded from 3% and 5%. However, the recovery lost momentum in 2015/16, a rise of only 2%. The strong result for 2014/15 occurred as the housing boom had a head of steam and as the Australian dollar fell sharply, to be at more competitive levels.

And the lesson? If you want to grow post-mining boom get the dollar down.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.