I remain focused on US reflation which has more momentum today. Donald Trump is moving on legal immigration, via the FT:

The US Department of Homeland Security on Tuesday issued sweeping new rules for border security and deportations as part of President Donald Trump’s promised crackdown on illegal immigration. In a pair of memorandums, homeland security secretary John Kelly detailed steps “designed to stem illegal immigration and facilitate the detection, apprehension, detention and removal of aliens who have no lawful basis to enter or remain in the United States”. Mr Kelly directed subordinates to start planning construction of a wall along the border with Mexico; hire 10,000 new immigration agents plus 5,000 additional border control officers; and “surge the deployment of immigration judges and asylum officers”. The moves continue Mr Trump’s breakneck effort to demonstrate early progress towards fulfilling the campaign promises that fuelled his election victory.

Advertisement

Whatever your principles, it all adds to US wage inflation at the margin. OPEC is also doing its bit as oil futures take off, via John Kemp:

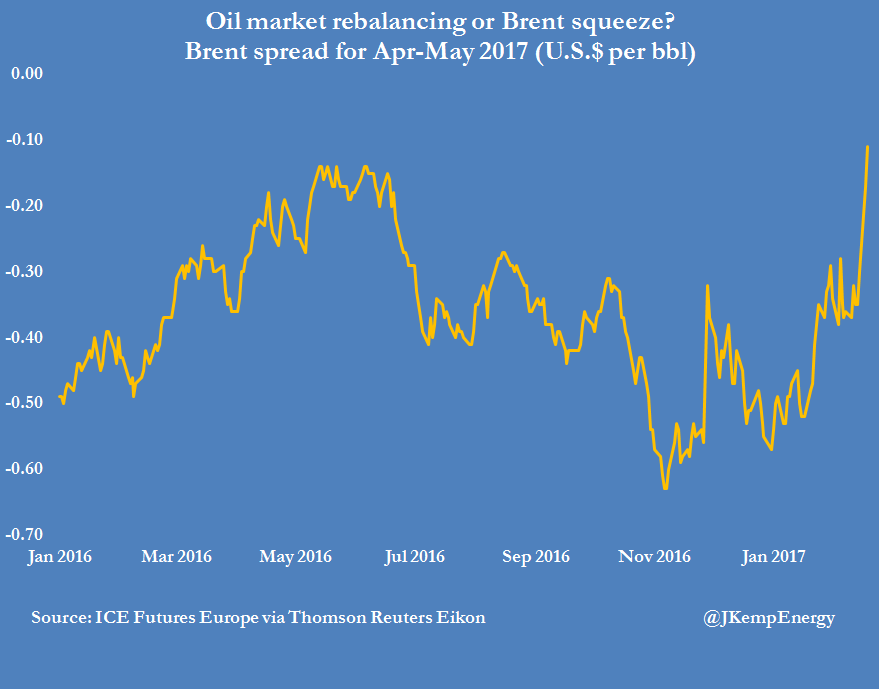

Brent futures prices for the second quarter have risen strongly in recent days suggesting traders expect the oil market to move into deficit earlier or that a squeeze is underway.

Calendar spreads for nearby months have tightened sharply since the middle of February to a level that will make storing oil outside the United States unprofitable from the start of the second quarter onwards.

The calendar spread from April to May has tightened from a contango of 35 cents per barrel on Feb. 15 to just 17 cents on Feb. 20 and is now trading around 12 cents (http://tmsnrt.rs/2mhTrZd).

The spread is now too narrow to cover the cost of financing and storing barrels under any set of realistic assumptions about the cost of borrowing money and leasing tank space.

Spreads are even narrower for later months, with a contango of just 10 cents for May-June and 7 cents for June-July.

The spread tightening has been concentrated in the second quarter which implies traders now expect a supply deficit to occur from April rather than June (http://tmsnrt.rs/2mhEB4W).

Calendar spreads have tightened much more in Brent than in WTI – where the spreads remain wide enough to finance crude stockpiles in the United States through until about June (http://tmsnrt.rs/2lirXoA).

If the tightness in Brent persists, physical traders will have an incentive to unwind cash-and-carry storage trades where they hold a long position in physical oil and a short position in futures.

Physical barrels will be sold from stockpiles to refiners and reported inventories should start to decline rapidly.

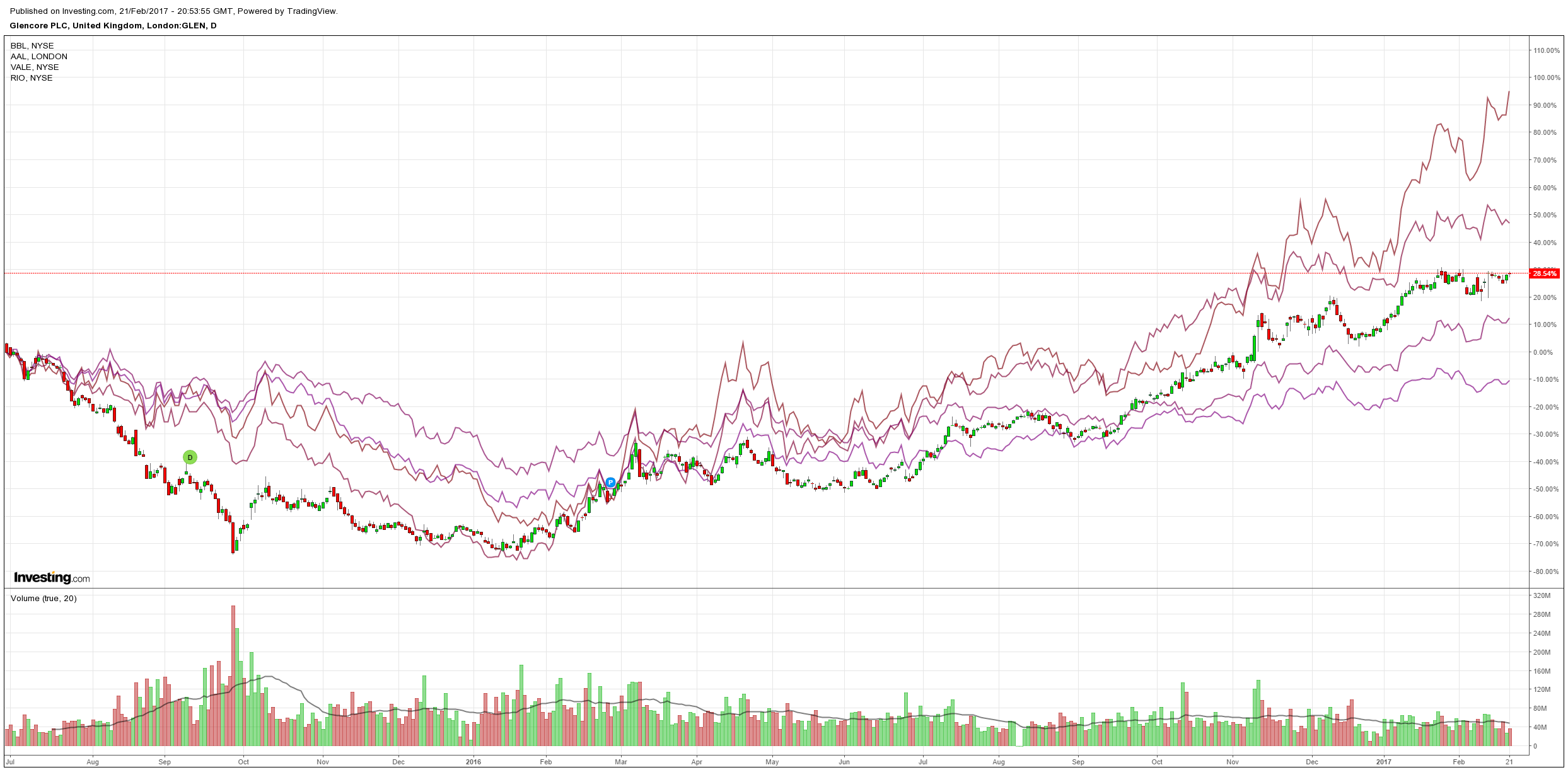

If this happens then US shale will continue its gallop back into the field. The high yield debt that funds it has already broken out. Everything will rise with it: base metals, shares and yields. At least until the last one chokes it all off, it’s boom, baby, boom!

Advertisement

MB allocations remain:

buy the dips in the S&P500 and USD;

buy the dips in short end Aussie bonds (though this one may need review if the Coalition housing bribe arrives);

sell the rallies in AUD and commodities;

buy gold on the dips for portfolio protection;

sell property (especially if we get the Coalition housing bribe!)

We are also exploring a new European long given it may just turn out that France and Germany swing Left not Right in their elections unleashing eurobonds and fiscal but more on that later.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.