It’s time for RBA Assistant Governer Luci Ellis to be promoted. Let’s recall her exemplary record of housing bubble defenses.

In 2006, as the world stood as the brink of the greatest housing crisis in history, Ms Ellis made the bold claim that:

The resulting expansion in both sides of the household balance sheet is an important development for policy-makers to monitor, but it is probably not of itself a cause of financial instability…

Particularly in North American markets, simple ratios have given way to credit scoring and risk-based pricing, so that loan sizes and pricing are more closely tailored to individual borrowers’ circumstances. To the extent that this reduces the margin of safety for some borrowers who are now able to borrow more than the older practices would have implied, this might mean that more households are facing greater financial risks than previously. But overall, this easing of financial constraints is a reflection of their ability to repay and withstand those risks. Therefore it cannot be assumed that a shift away from the earlier lending practices based on rigid ratios implies that financial vulnerability has increased in any significant way…

[And] The most important lesson to draw from recent international experience is that a run-up in housing prices and debt need not be dangerous for the macroeconomy, was probably inevitable, and might even be desirable.

Since then, Ms Ellis has also claimed that:

Advertisement

the US housing bust resulted from supply flexibility when it was, in fact, the reverse;

Last week she added to this impressive list going in to bat for the great bubble using eccentric figures on debt ratios [my emphasis]:

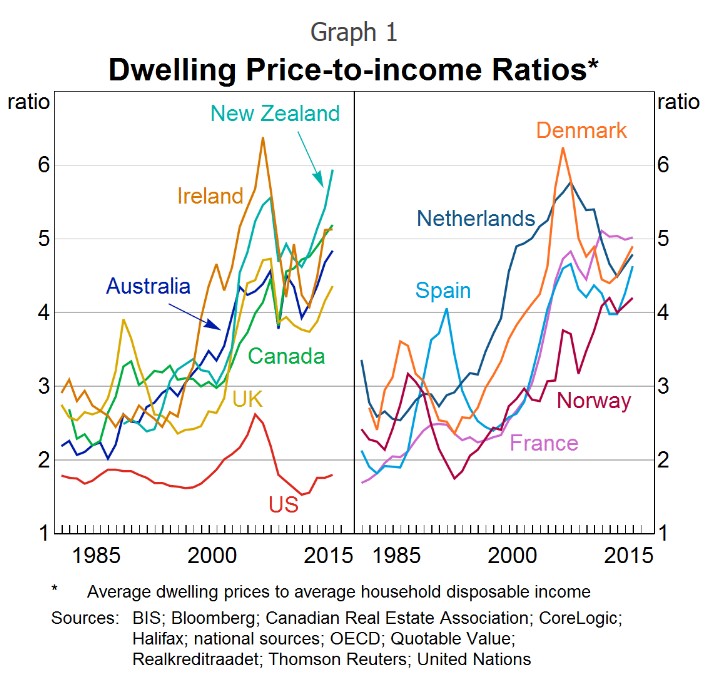

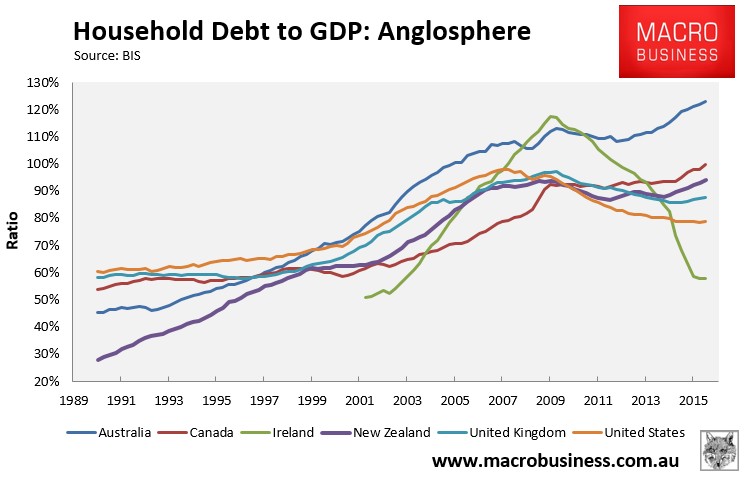

Australia is somewhere around the middle of the pack of mid-sized countries on this metric.

Similar comparisons of household debt-to-income ratios across countries also put Australia in the middle of the pack.

When in fact it looks like this, according to the Bank for International Settlements (BIS):

Advertisement

And she re-iterated the untruth:

What we can do is get some sense of the relativities between countries that you might expect, given those institutional and other differences. For example, we can reasonably expect that countries where much of the population lives in smaller, cheaper cities will have lower national aggregate ratios of housing prices to incomes than other countries. That might partly explain why the price-to-income ratio for the United States is relatively low.

When we know for a fact that Ellis is comparing apples to oranges by using “greater” measures of Australian city populations but only inner city populations for the US, and we know that she has been notified of such.

Advertisement

This is some serious heavy-lifting on behalf of the bubble and we don’t think that it should go unrewarded given it appears to represent the bank’s view. Ms Ellis has already been promoted for this fine work to Assistant Governor (Economic) but that’s insufficient. Following the Securency case, Rick Battelino and others enjoyed fat retirement packages and exotic locales. It is only fair that Ms Ellis enjoy a similar sinecure and, if that is any problem, it can always be, ahem, finessed.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.