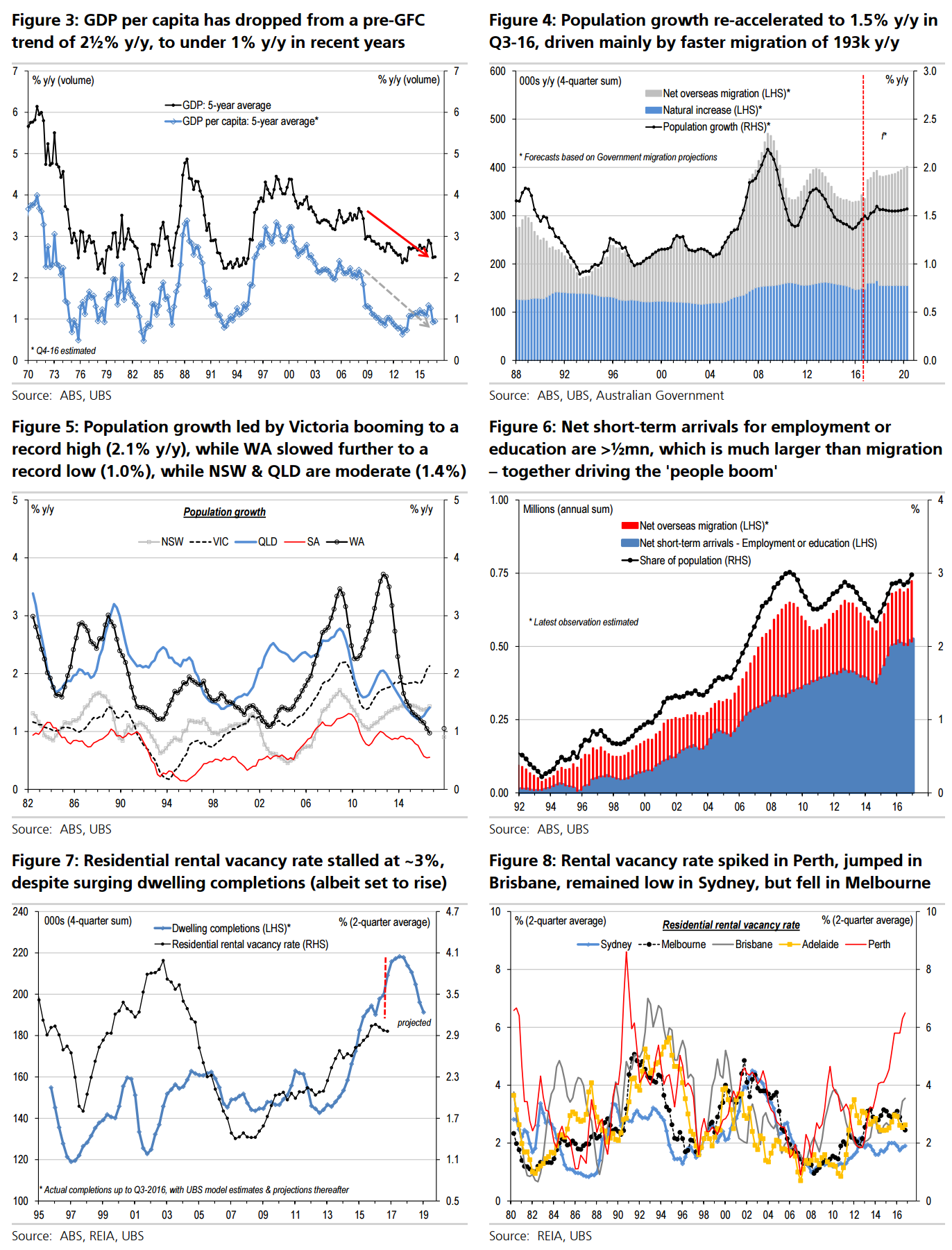

Q3-16 population picks up to 1.5% y/y (349k y/y), the highest in >2 years

Population growth lifted 0.4% q/q & 1.5% y/y in Q3-16, the equal fastest since Q1-14. This is still slower than the last population boom around the GFC & terms of trade peak, when growth hit >2% y/y (which was the fastest trend since the 1960s). However, despite a terms of trade & mining capex retracement over recent years, population remains well above the ‘pre-boom’ average of closer to ~1% y/y in the ~15 years to the mid-2000s. In Q3, population rose 349k y/y (to 24.2mn), the most since Q1-14. The larger driver was a rebound of migration to 193k, while natural increase was ~steady at 155k y/y (boosted by another ‘baby boom’ with record births of 315k).

Population growth set to accelerate a bit ahead, driven by higher migration

Importantly, Government migration department and Budget projections imply a further lift of migration in coming years towards 250k, the 2nd highest in history behind the record boom of 2007-2009. Assuming natural increase at current levels, this implies population growth will keep accelerating to ~1.6% y/y in the coming couple of years.

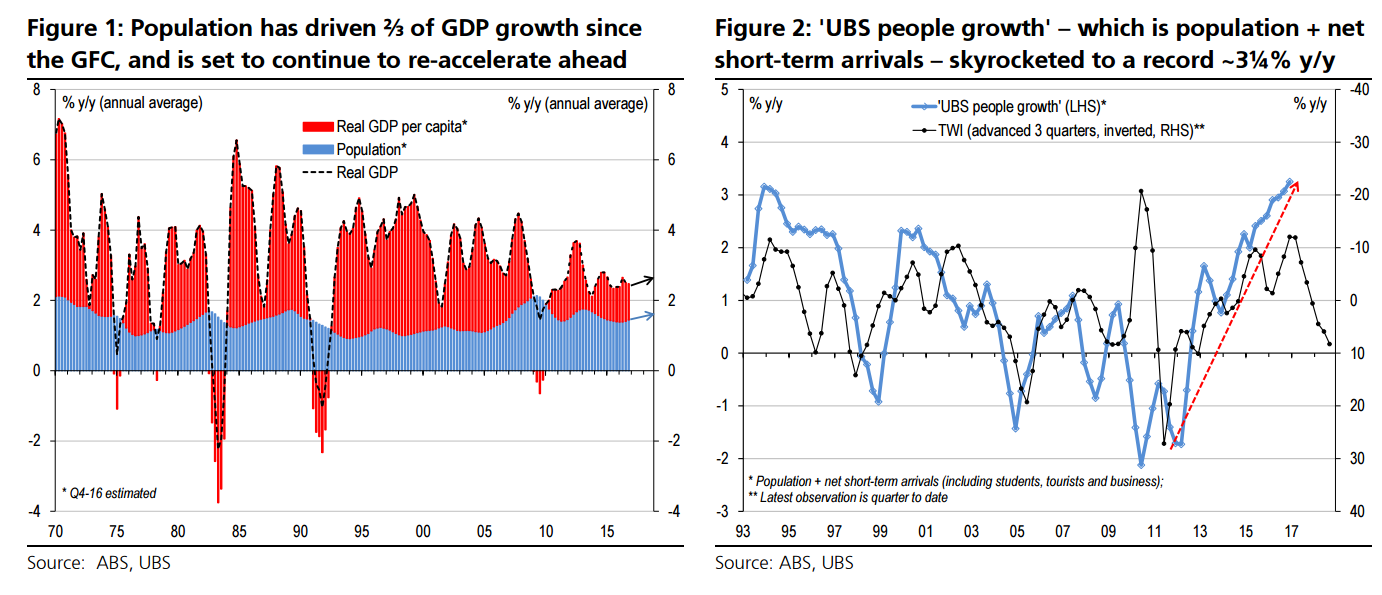

Population drove ⅔ of GDP since the GFC, partly offsetting a drop in per capita

Population is increasingly the key driver of Australia’s economic performance. Since the GFC, population growth (averaging 1.6% y/y) contributed ⅔ of GDP growth (averaging 2.4% y/y), double its contribution in the prior 15 years. Indeed, GDP per capita growth has dropped sharply from its pre-GFC trend of ~2½% y/y, to under 1% y/y now.

Meanwhile, helped by a sharp fall in the AUD over recent years, there was a coincident boom in net short-term (1-year or less) visitor arrivals. When combined with population growth, our estimate of ‘UBS people growth’ – those physically in Australia – skyrocketed >3% y/y, the fastest ever. Overall, this ‘people boom’ underpins our GDP outlook for a modest acceleration to 2.7% y/y in both 2017 & 2018. For housing, while a sharp lift in dwelling completions and consequent jump in vacancy (and weaker rents) likely still lies ahead, this ‘people boom’ may contribute significantly to softening the housing downturn (for details see our 81-chart housing deep dive and policy response).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.