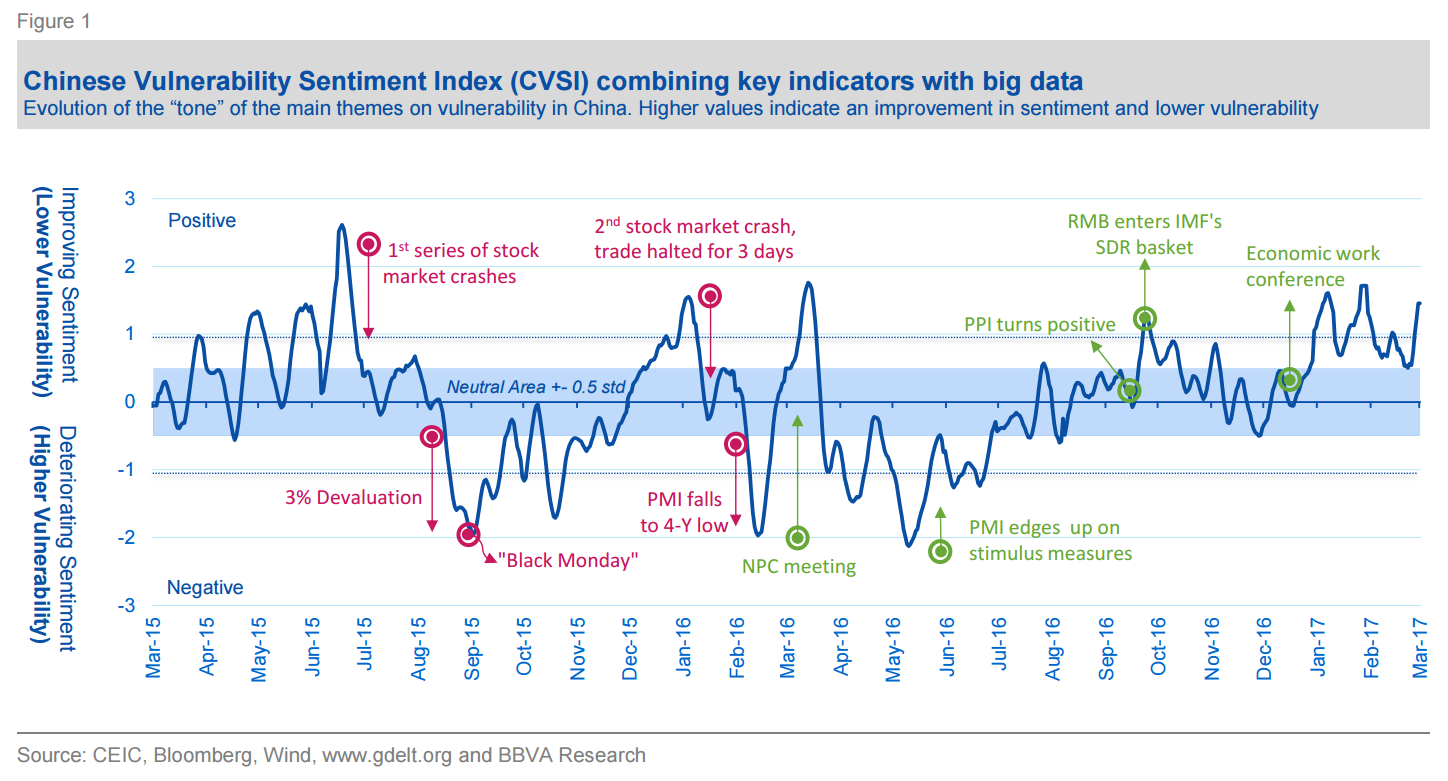

The China Vulnerability Sentiment Index (CVSI): Tracking risk in real time In a recent working Paper (Shiller, R. 2017)1 , the Nobel Prize winner Robert Shiller claimed that the use of new empirical research through textual analysis and Big Data should be extended empirically to analyze the role of narratives in Business Cycle Theory. In this watch and forthcoming paper, we take this into account to analyze Chinese vulnerability. Moreover, rather than focusing on measuring economic activity sentiment related indicators (i.e. animal spirits); we develop an index to track Chinese vulnerability sentiment in real time using Big Data. This could help us to identify key vulnerabilities in China using risk narratives, which have the potential to become self-fulfilling in either direction.

Our new China Vulnerability Sentiment Index (CVSI) combines daily time series on sentiment from a Big Data database called Global Database on Events Location and Tone (GDELT) with official statistics (hard data) and financial indicators, making it unique in its robustness and depth (Figure 1). GDELT2 is an initiative which aims to construct “a catalogue of human societal-scale behavior and beliefs across all countries” through the continuous analysis of news and events referenced in the media. Thanks to the use of high frequency Big Data series from GDELT, the CVSI enables us to “nowcast” vulnerability developments and identify early warning signals in real time, helping investors and policy makers to factor in risks ahead of time. Our index is unique in the sense that it enables us to track vulnerability and sentiment along a number of risk parameters. These were carefully selected to replicate the main vulnerabilities faced by the Chinese economy, as reflected by the four main components of the CVSI, outlined in more detail below.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.