Iron ore price charts for March 17, 2017:

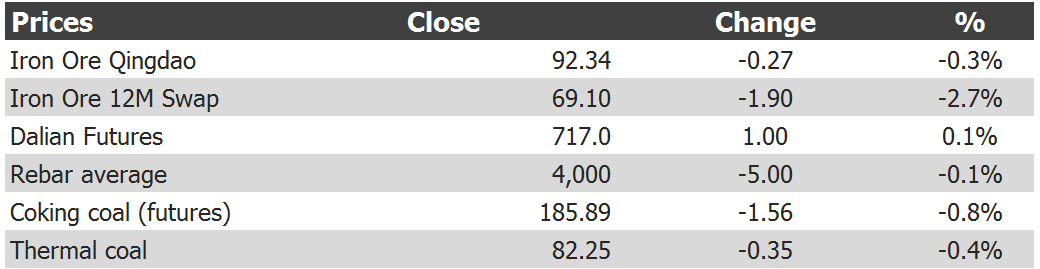

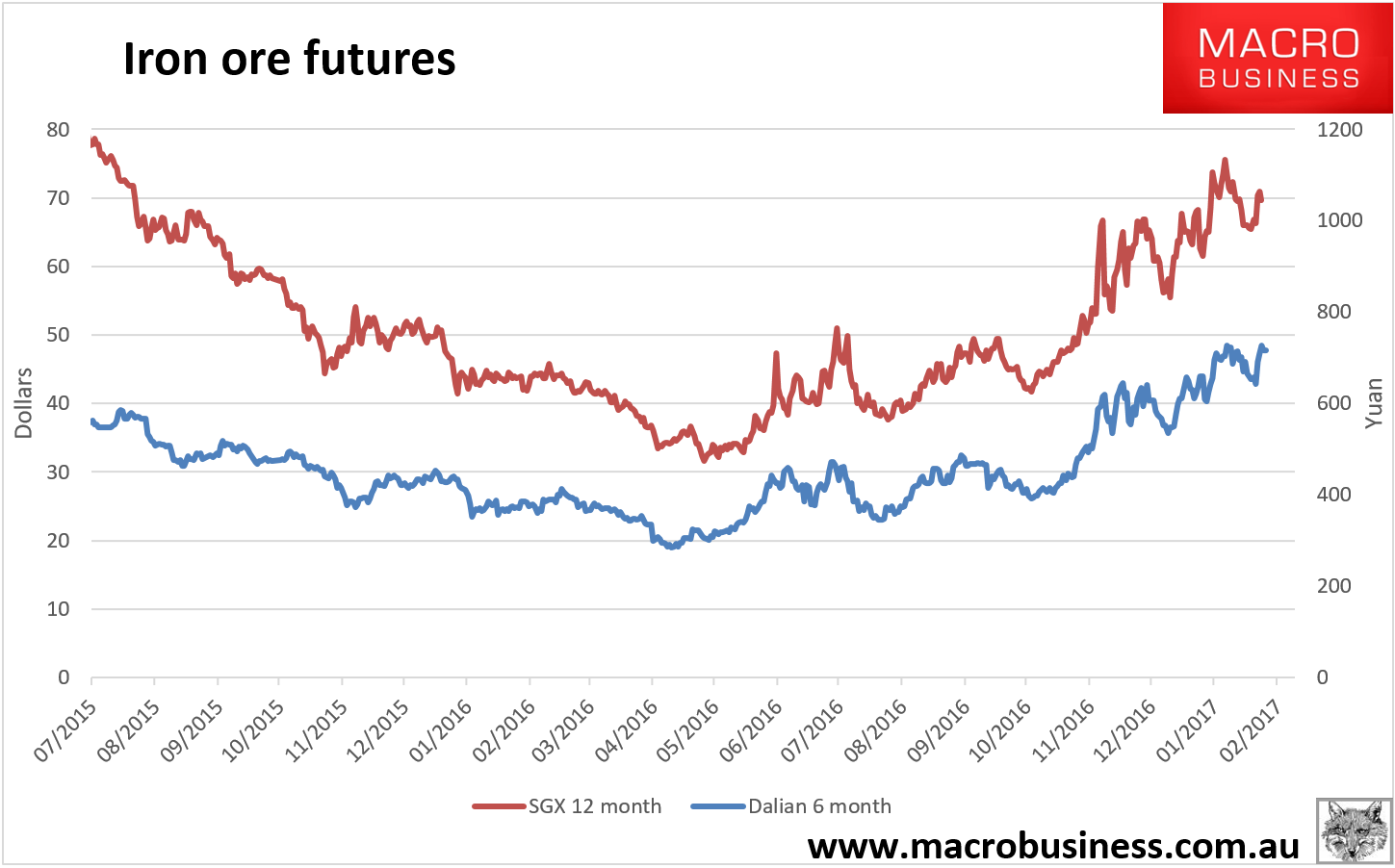

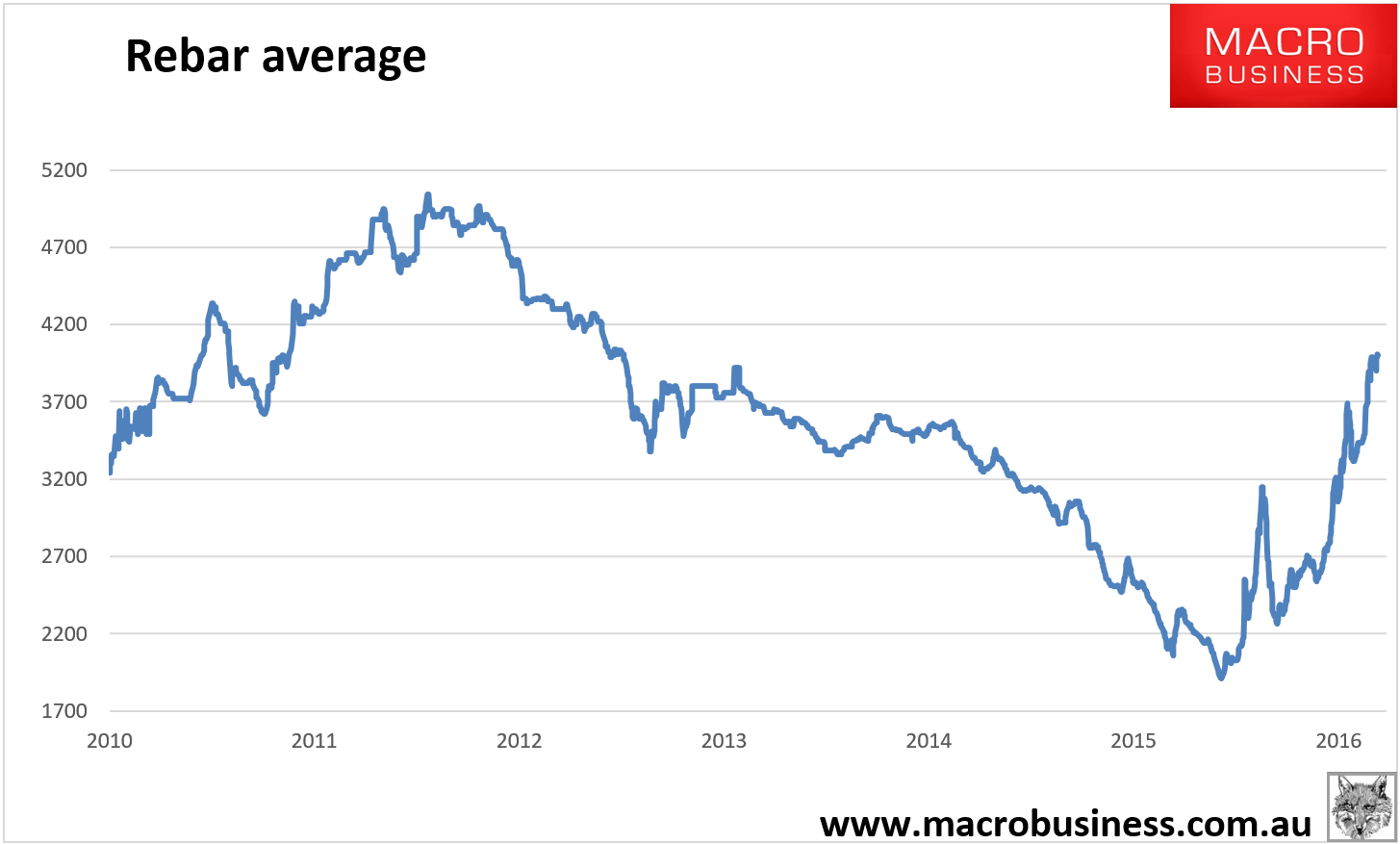

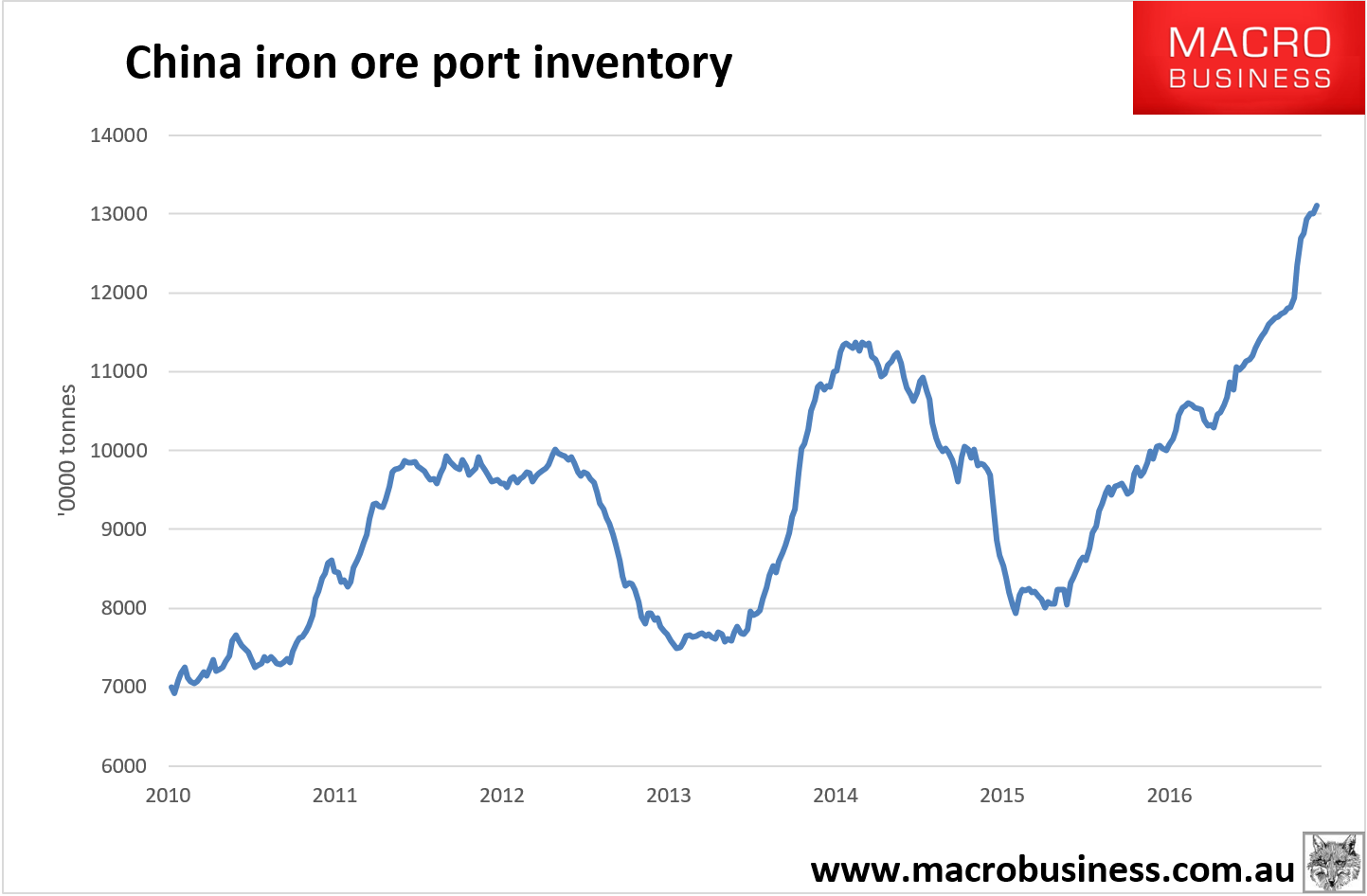

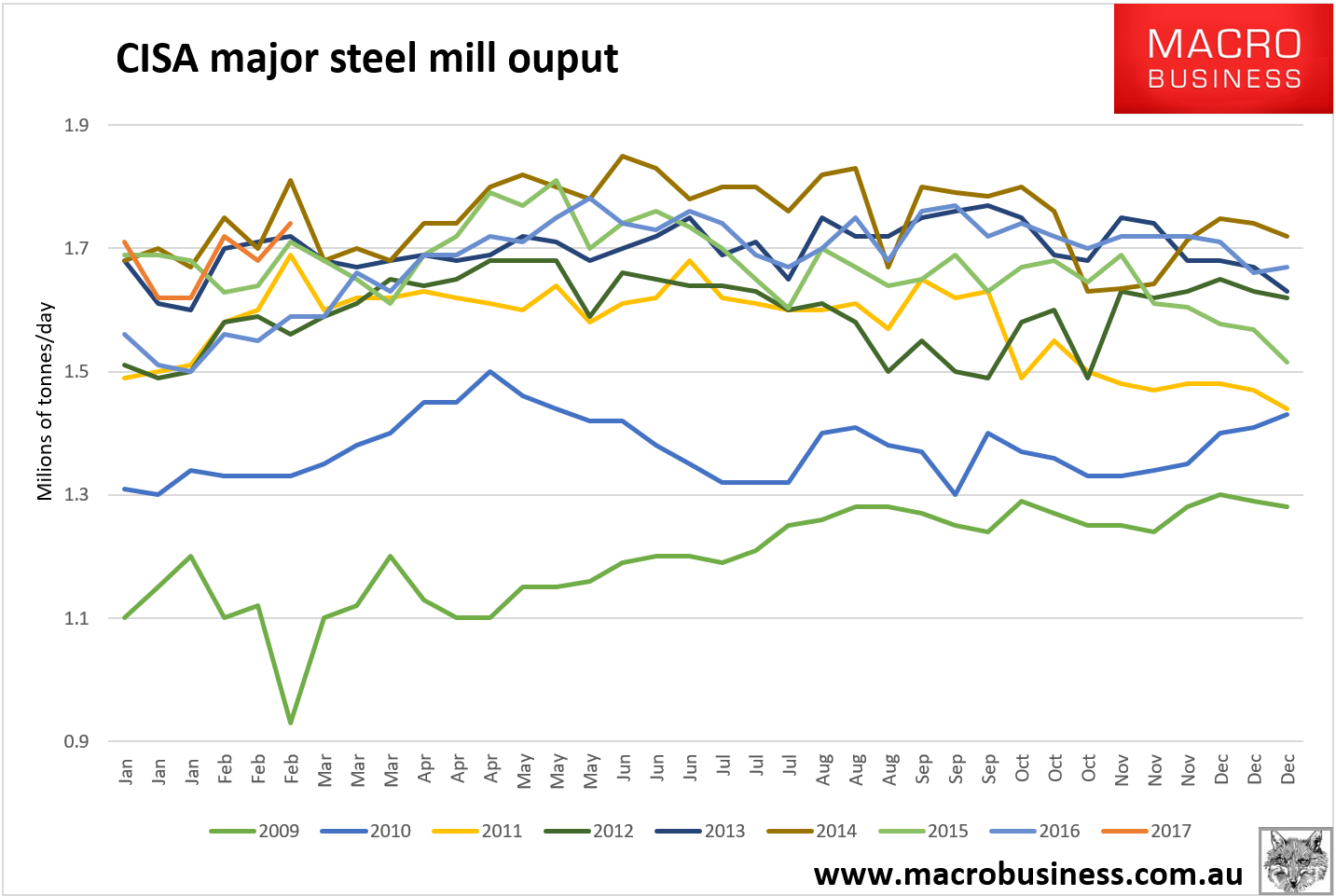

Spot was down a little. Paper was flat overnight. Steel too. Coals faded. Chinese port stocks added another one million tonnes last week to hit a new all-time record. CISA major mill output was up 3.5% in late February to 1.72mt per day. This remains 2.3% below the peak year of 2014 and if annualised indicates 804mt for the year. This would be down a little year on year from 2016’s 808mt. It’s bang on my thoughts and it is in no way enough to justify current iron ore prices. The difference is restocking and hoarding.

So the major question that anyone needing to predict prices this year must ask is when does that restocking pulse end? Given abundant inventories for steel and the huge pile of iron ore, we can safely conclude that there is nothing now holding up the restock other than sentiment. That pulse appears to come under pressure whenever we are above $90 and to keep it there inventories have to keep building too.