Towering steel prices have opened fat cash margins for steel mills

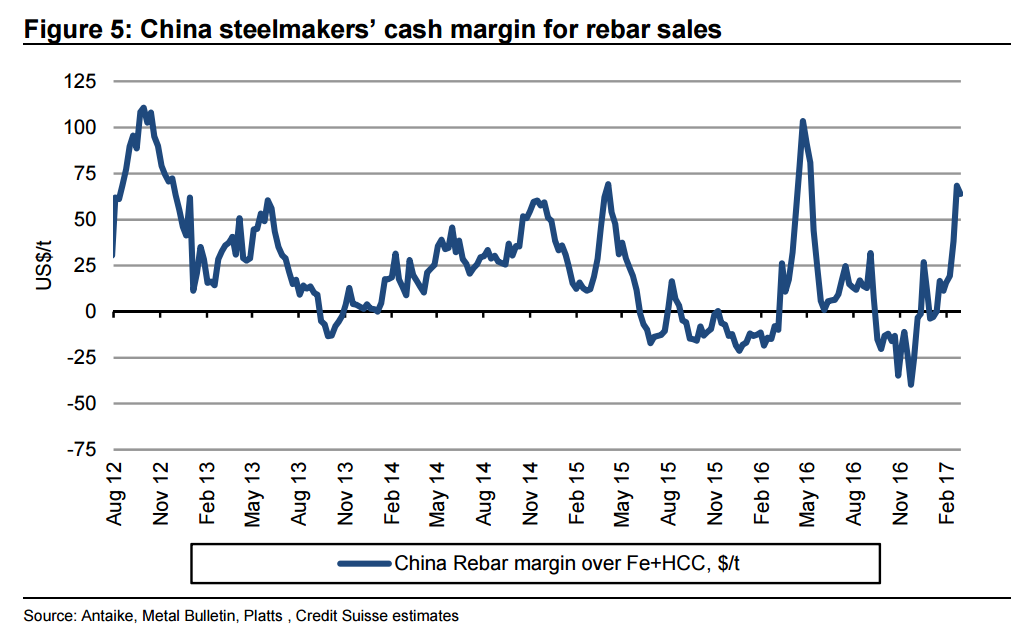

The towering steel price is delivering fat cash margins to China’s steel makers (Figure 5). Earlier challenges to profitability from high HCC prices are dissipating, but the steel price has continued to climb, widening the margins. And this has occurred ahead of the spring construction season in China. Understandably, steel mills are stocking up with raw materials to run blast furnaces flat out, and seeking high grade iron ore to maximize output. So right now it’s steel prices alone driving iron ore prices, because steel mills remain in a restock mode and are buying raw materials while margins are wide.

So what is behind China steel’s remarkable bull run?

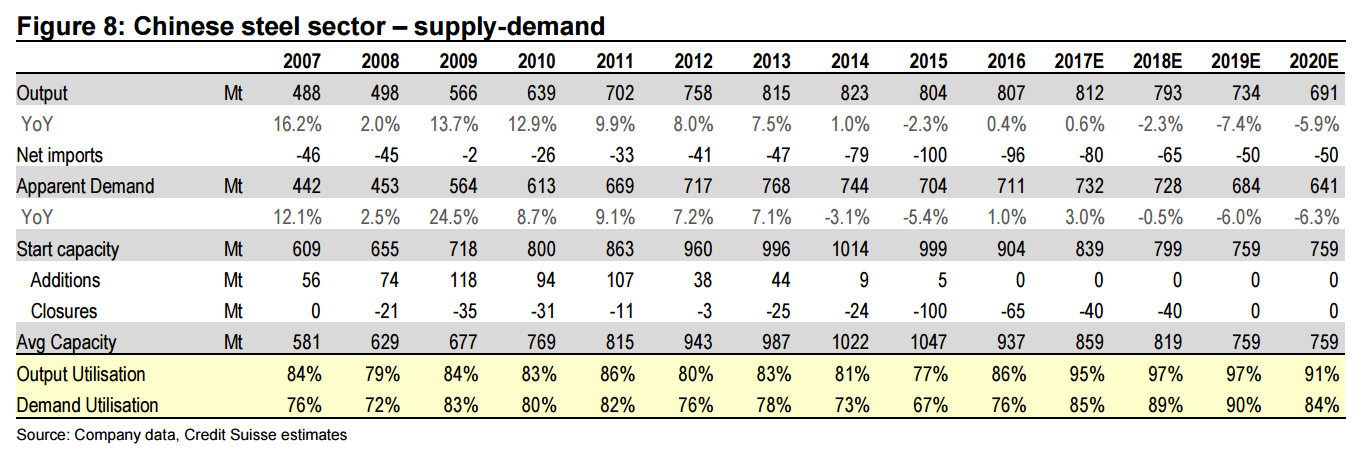

China steel prices are powerful because demand is solid, and are expected to become stronger again in the construction season, and supply remains fairly tight with mills operating at high capacity utilisation. We examine these points in more detail below. China steel demand to remain 3-4% Trina Chen, leader of our China Basic Materials team, maintains a view that China’s steel demand should rise by ~3-4% in 2017, led by infrastructure, and supported by stable property construction. That demand lift is largely offset by our estimate of lower steel exports, so the increase in China’s steel production is only 0.6% (Figure 8). Our team remains less bearish about property than the market. We expect growth of a couple of percent, largely from lower tier cities. The construction market is not strong, but it is stable. We believe there has been no deterioration in construction since the Government applied constraints on purchases in higher tier cities in October. Further out, our China team is more cautious about demand in 2018. In that year we believe demand growth may fall a couple of percentage points as infrastructure projects wind down. The sign-up of new projects appears to be slowing as the Government subsidies required to advance the projects are proving expensive.

Steel order books remain full

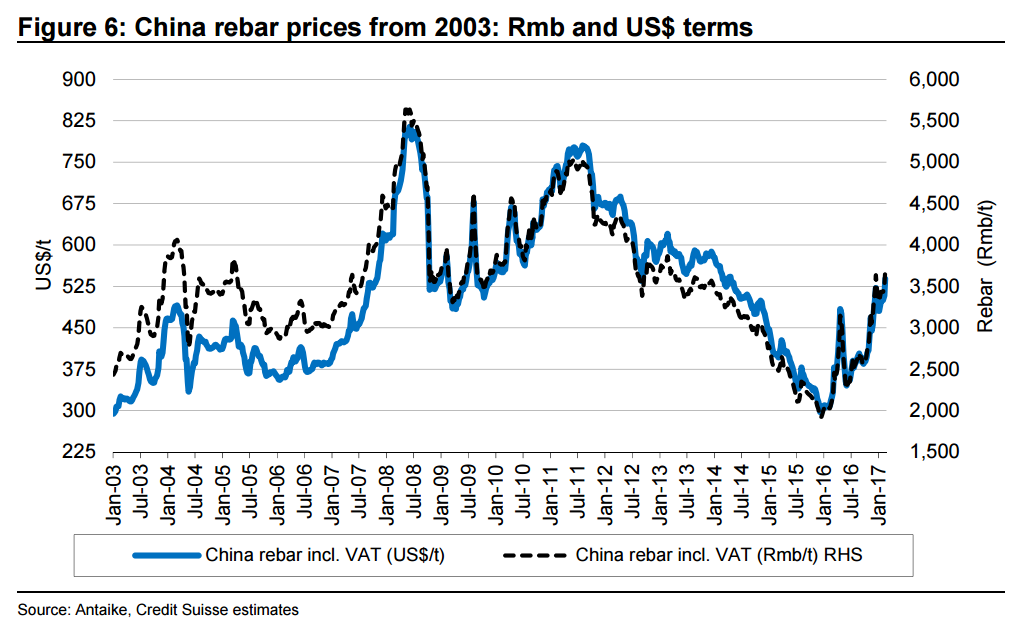

Trina Chen’s latest China Basic Materials Monthly – February 2017: Full orderbook again of 23 February reported that channel checks suggested order books for large and medium sized steel mills remained firm. Order books for February are full and March looks full also. Channel checks on downstream order books also showed improving end-use demand. Trina points out new infrastructure is a highlight while property construction remains stable. How high can steel prices go? If steel is at the highest levels since 2013, is it peaking? We plot rebar steel prices in both Rmb and US$ terms over 14 years (Figure 6). The currency has an affect because China’s FX has changed markedly over this period, from 8.3 yuan per US$ in 2003, down to 6.1 in Jan-14 and subsequently back up to 6.9 currently. From the 14 years of price history for China rebar, two things immediately strike us:

■ Current rebar prices look normalised in Rmb terms; and

■ The rebar price of Jan 2016 was extraordinarily low.

Current rebar price not remarkable in historical terms The current price is not markedly higher than the low reached in the GFC of 3Q-08 to mid- 2009. So while the steel price has enjoyed a very strong rally, it was from an extraordinary low – so low in fact that almost all steel companies in China recorded very large financial losses in 2015. Now, steel mills have returned to profitable production, but steel is not yet exhibiting a super-spike, such as 2007-08 or 2010-11. It was the super-spikes in steel prices that previously lifted iron ore prices to the heights of +$150/t in 2010-2011 (Figure 7).

Current steel demand looks insufficient to drive a super price spike

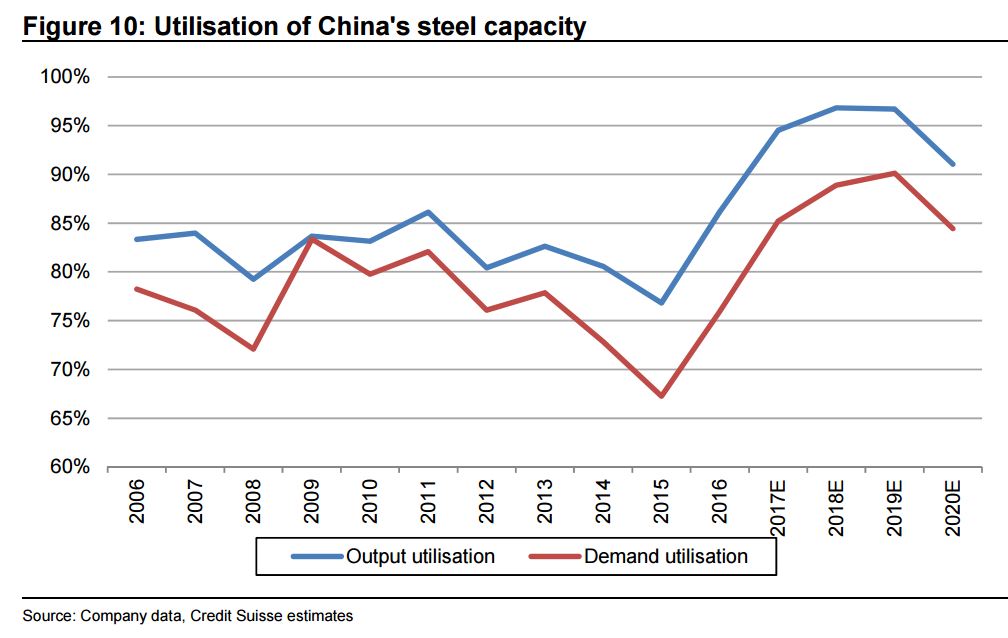

The current modest demand growth of 3-4%, and less than 1% for steel production, suggests a super-spike in steel pricing is unlikely. Infrastructure and housing construction are lifting steel demand, but it is clearly at a different rate to the frenetic pace of construction that occurred before the Global Financial Crisis or in its aftermath under the Chinese Government stimulus. China’s steel mill capacity utilisation should allow stronger prices However, demand is not the only factor controlling steel prices; another is capacity utilisation of steel mills. Capacity utilisation matters because at high levels (~85%), it provides producers with pricing power. With high output, there is insufficient latent capacity for over-production and discounting by producers that seek market share. Instead, consumers become more anxious about supply and willing to pay list prices. Trina Chen constructed the capacity factors for China’s steel sector in her 2017 Outlook presentation, which we have copied and updated with more recent data (Figure 8). In 2010-11, when the steel price spiked, the capacity utilisation of steel mills was 83% and 86%. 2013 was another strong year for steel and again the utilisation was 83%. In contrast, 2015 was an awful year for steel and capacity utilisation of the steel output dropped to 77%. But the situation was even worse than that. China’s demand was so weak in 2015 that steel mills were forced to dump discounted steel overseas, so exports surged. If we look at apparent demand against capacity, the utilisation fell to 67% in 2015, from 78% in 2013 and 82% in 2011.

Capacity utilisation now climbing

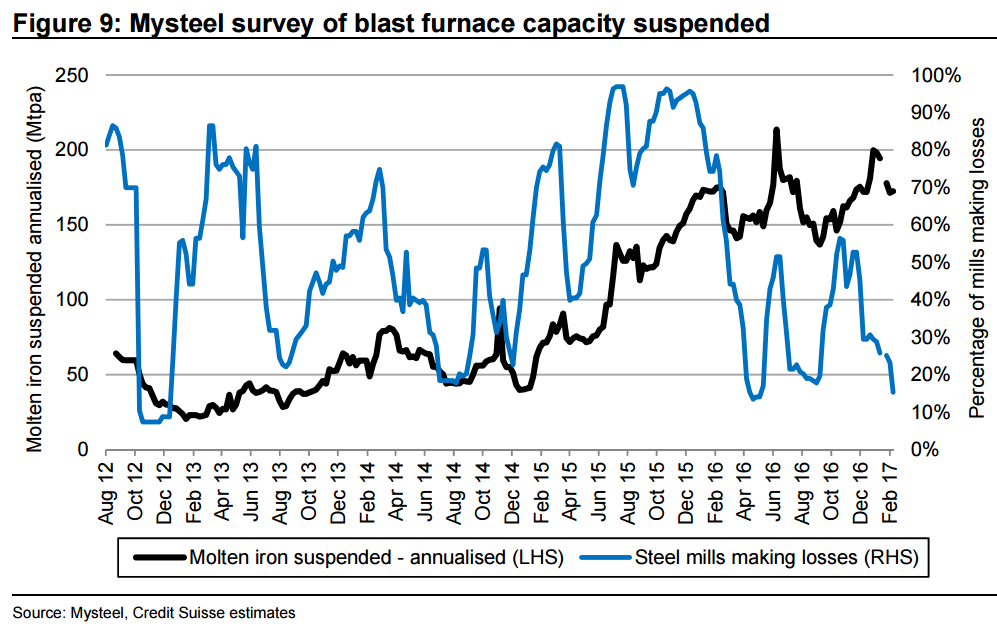

The viewpoint of capacity utilisation gives us hope that prices could be stronger in future than previously. Steel mills have been forced to close, because of both financial reasons and Government intervention, and these closures are lifting the capacity utilisation of the survivors to high levels. In 2016 steel prices were far stronger than 2015, even though output and apparent demand lifted barely 1% over 2015 (Figure 8). What did change was output utilisation lifted to 86% because 100Mt of steel capacity was closed due to very large losses in 2H-15. Trina Chen has pointed out that Mysteel surveys show this capacity did not restart in 2016 even as steel prices climbed (Figure 9), because finance was not available for private steel mills.

In 2016, NDRC set out to cut 45Mt from steel capacity and ended up cutting 65Mt according to Premier Li Keqiang. The NDRC plans to have cut 140Mt before 2020, which probably means higher capacity utilisation again in 2017 and 2018 (Figure 10). On our estimates, it is not until 2019 and 2020 that steel mill capacity utilisation may fall, as that is when we expect China’s steel output to fall sharply.

We don’t claim capacity utilisation is the whole story, but we do believe it has an influence and may ensure that steel prices do not slump to the lows of 2015 again. This in turn provides a stronger outlook for iron ore prices into the future.

China supply cuts – Emerging risks of overshooting supply cuts

The original supply cuts in 2015 were delivered by market forces – extremely low prices forced shutdowns by private mills that did not have the seemingly endless borrowing capacity of SOEs. In 2016, the NDRC added to those capacity cuts in an organized fashion to prevent over-production and give relief to banks with heavy loan exposures to the industries. But there were also other temporary steel supply outages during the year enacted to control air pollution. These actions look set to increase and be formalised by the Ministry of Environmental Protection. Following the extreme levels of pollution in Beijing in the past winter, air pollution prevention has become a top priority for the government. Aggressive strategies are being devised by agencies to reduce the winter pollution.

Trina Chen now sees overshooting on supply cuts as an emerging risk on the supply-side of basic materials, including steel. Trina considers that multiple government agencies are operating in an uncoordinated and potentially irrational manner following individual agendas, so there is a high risk that cutbacks in production will be over-zealous.

The NDRC has not finished with its capacity reduction. More closures are planned to permanently improve the steel sector by eliminating outdated, poor quality and obsolete facilities. But with pollution now jumping to the top of the list in the Government’s policy priorities, winter cutbacks in a range of industries including steel have apparently been approved, in a bid to clear the air around Beijing. 50% steel capacity cuts have been ordered for the winter in four cities – Tangshan, Shijiazhuang, Handan and Anyang.

Reuters estimated one third of China steel production came from this region, so with a 50% capacity cut, we estimate 17% of China’s production capability would be curtailed over the winter. Over four months, this may amount to 40-50Mt of lost production for the region. Presumably this would be made up by other steel mills running harder, but it seems highly likely to tighten prices over winter. The first run of this new policy is likely to start next November.

If too much capacity is cut, steel (and iron ore) could be the next coking coal

If Trina’s concern is realised and agencies have cut too much steel capacity, there is a risk that steel prices could rise sharply to new highs. Bloomberg cited a Mysteel analyst pointing out that the three cities in Hebei province targeted for steel cuts in winter have 70- 80% of the province’s capacity. A 50% supply cut over four months is a very big loss and “may lead to short-term tightness in steel”. The risk of overshooting on cuts and driving a steel price spike may seem remote at present, but it happened with coking coal last year, so it cannot be dismissed. And if the steel price shoots upwards, the iron ore price would likely go with it.

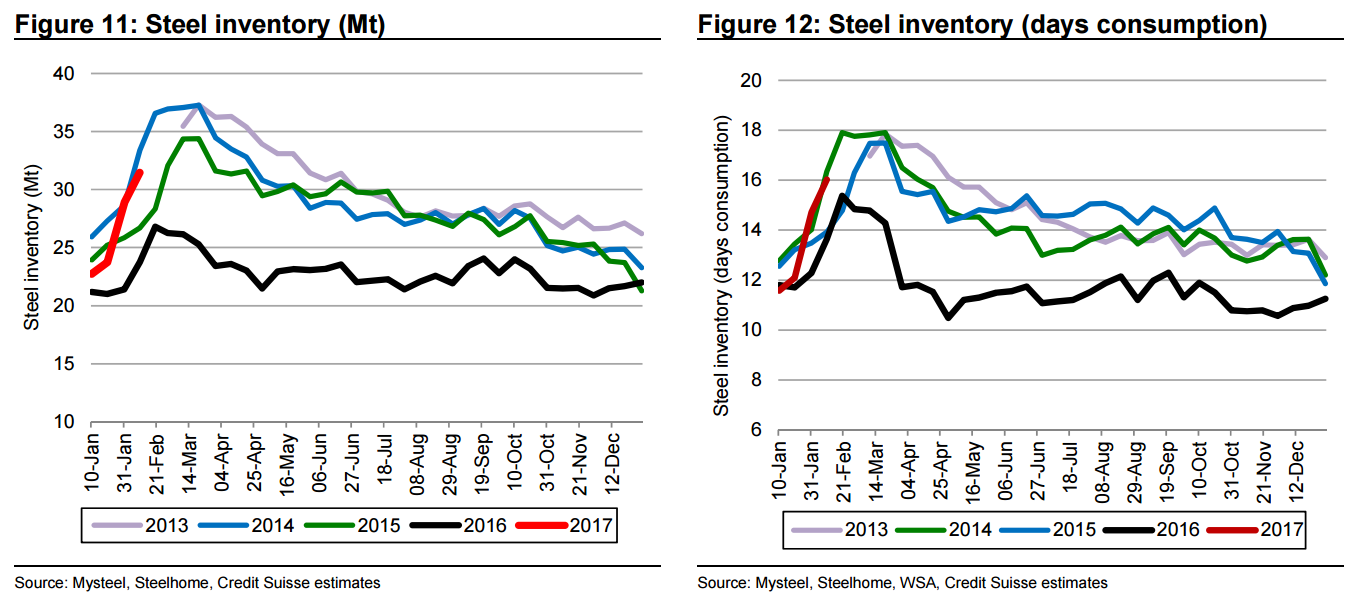

Restocking – largely complete

According to our China steel stock model, China was depleted in steel all through 2016 (Figure 11). However, in early 2017, the restock is well underway. By early February, China steel stocks were on trend with 2014. All the stocks we include have risen (CISA members finished stocks, Tangshan billet stocks in warehouse), but the largest rise is steel traders’ stocks.

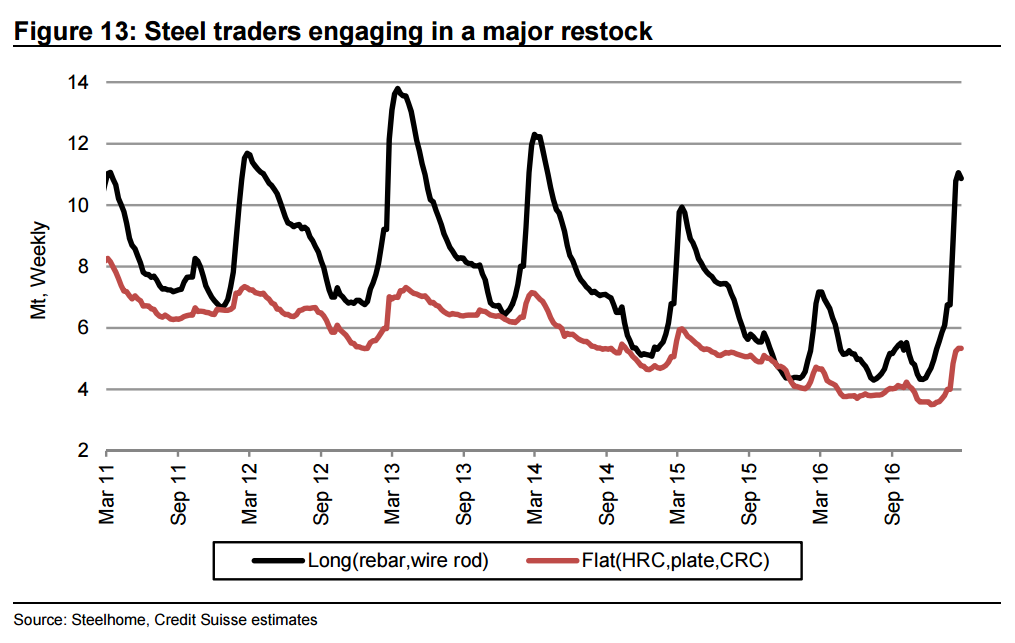

Traders expect another good year – built inventories early

Steel traders started rebuilding stocks early this season commencing in December 2016. Last season, the stock build only got underway in late January and never reached any heights because steel traders could not get hold of steel. Our sources said they believed steel mills were withholding steel last year, but we think the more likely explanation was that steel mills had cleared out inventory and forward-sold what they were producing. Nevertheless, the steel price rise in 2016 made the year highly lucrative for steel traders. So this year, they made sure they have steel secured ready for the construction season, and have enjoyed a price rise in their inventory through the early months of the year. It seems steel traders are expecting construction to look like 2014 at least. To date, 5Mt have been added to long product holdings.

Steel restock ending will no longer help steel prices

Low stocks throughout 2016 probably assisted demand and rising capacity utilisation is lifting steel prices through the year. And the rebuild of stocks has probably assisted in maintaining strong steel mill order books through the winter months, again helping steel prices. But now that stocks appear replenished, this source of demand should ease and will probably no longer help steel prices. In fact we believe they will be a headwind as, very shortly, steel traders will probably be selling as construction picks up pace, displacing sales from steel mills.

Very good. Macro should swing against steel by mid-year as housing slows. Then from 2018 onward we resume the great deflation, assuming a return to reform, or China’s pushes it on towards 2020 and eventually crashes.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.