As expected, the RBA Board decided to leave rates unchanged at 1.50% following its March meeting (Link to Statement).

Impact

Subtle shifts in language around investor housing growth reinforce the near term hurdle to further policy easing. Persistent lowflation concerns remain at odds, in our view, with the direction of market expectations. The Statement offers little to shift our view that direction of risk from the lopsided nature of the economy remains tilted towards a further reluctant cut, rather than hikes.

Outlook

On hold: The stronger-than-expected 4Q16 GDP outcome (Aus Econ – GDP – Phenomenal, but lopsided, 2016 finish) and robust labour market undertone (Aussie Macro Moment – Labour force: Better than it looks), will have provided the RBA with a degree of comfort to hold steady in the face of pockets of concentrated house price strength. Now’s the time to hold, but the RBA’s qualifications around the growth outlook remain. It’s too early to fold.

Too early to fold: Whether that comfort can be sustained over 2017 depends on how well the commodity-price-driven income surge flows through to domestic spending, and hiring. Fiscal channels are blocked, capex remains a way off. Hiring intentions and job ads are firm, but the underlying investment by non-mining firms needed to deliver more than just an ‘alleviation of the mining downswing’ remains elusive (Capex – Still missing in action).

House prices leave no room to run: Phil Lowe recently discussed the view that rates could be lowered to boost the questionable domestic backdrop behind the strength in commodity prices, and mining profits (our base case). For households, an already stretched borrowing channel, and “brisk” Sydney and Melbourne house price rises, are the key counterpoint. Current strength in investor lending has raised the prospect that further macro prudential policy measures may be needed to free up monetary policy for macro stabilisation.

Except to Qld: The path of least resistance for policymakers is to let nature take its course, and let the relative extremes between Australia’s major capital city property markets play out through shifts in population flows. This alternate channel to further macro prudential tightening is an emerging multi-year theme we highlighted in Aussie Macro Outlook – Northern Exposure.

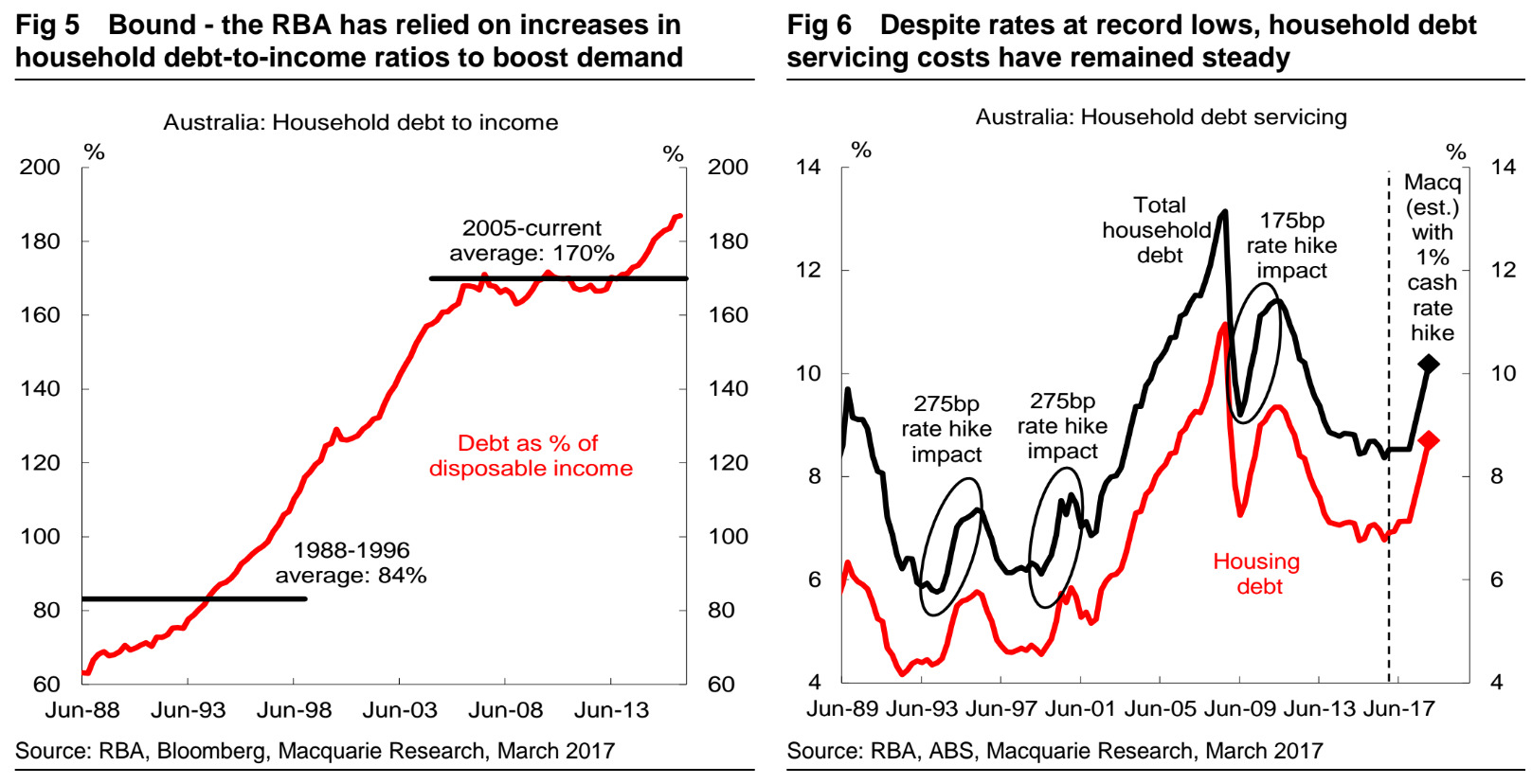

Rate rises – How far, and fast, can the RBA move? We don’t think the RBA will be raising rates until February 2019. But whenever they do, the path of future rate rises will be more constrained, and finish at a lower level. A wider spread between the cash rate and mortgage rates (from 180bp to ~375bp) is one factor.

The lift in the household debt-to-income ratio is another. Given households’ higher levels of debt, we estimate that a 1%pt increase in the RBA cash rate would – in the absence of further increases in bank borrowing rates – push the household debt servicing ratio beyond 10% (see figure 6). The lift in the debt servicing ratio the RBA achieved with 275bp tightening cycles through the mid and late 1990s could now be achieved with just over 3 rate hikes.

Three hikes to a tight cash rate. Sounds about right. Which raises the specter of secular stagnation, according to the BIS:

As long as inflation does not rise much during booms, partly held back by the tailwinds of globalisation and by central bank credibility, a monetary policy focused on near-term price stability has little incentive to tighten to restrain the build-up of financial imbalances. But then it has every reason to ease aggressively and persistently if the economy weakens and inflation declines further.

Over long horizons, asymmetrical policies across successive financial cycles – failing to constrain their expansion but easing aggressively and persistently during busts, with monetary and, to some extent, fiscal policy – could lead to a sequence of episodes of serious financial stress, a loss of policy ammunition and a debt trap.

Such a sequence imparts a downward bias to interest rates and an upward bias to (private and public) debt that at some point makes it hard to raise interest rates without damaging the economy. The accumulation of debt and the distortions in production and investment patterns induced by persistently low interest rates hinder the return of those rates to more normal levels.

Defining the natural or equilibrium rate without reference to its financial stability implications is arguably too narrow. It has encouraged the view, sometimes put forward by proponents of the secular stagnation hypothesis, that the interest rate could be at its equilibrium value and yet cause damaging financial and macroeconomic instability down the road.

I take this not so much as pointing to an inherent tension between financial stability and macroeconomic stability – there cannot be – but as reflecting what is missing in the standard models, ie the incorporation of financial instability in the first place. In models that did so, a more useful definition of the natural interest rate would also call for the financial side of the economy to be on an even keel – in equilibrium – so that financial imbalances do not build up.

In short, it is central banks that have killed central banks and we need to allow the system to clear once in while. An important insight from Austrian economics.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.