Ah yes, capitalism just can’t stand an area of excess profitability. From Credit Suisse:

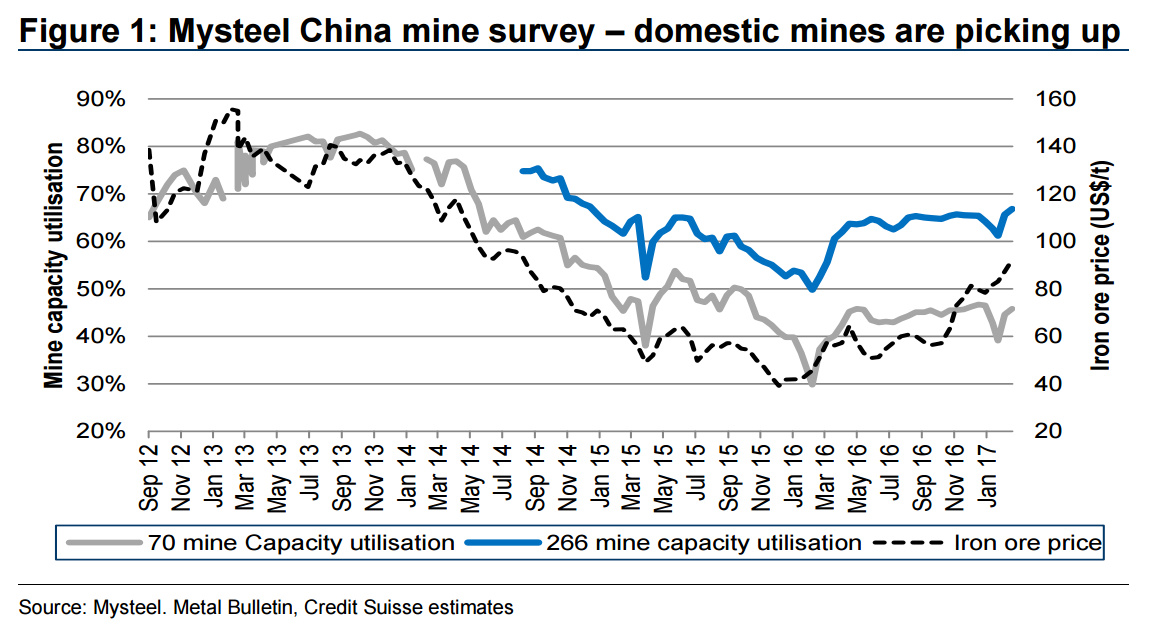

■ The lofty iron ore price is stimulating China’s iron ore mines to restart – confirmed by the latest Mysteel mine survey. The 266-mine survey came in at 430kt/day of concentrate – a capacity utilisation of 66.8% – the highest since Dec 2014. And it is very early spring, so mines should further expand just on seasonal factors. Platts provides supporting anecdotal evidence: a privately owned miner in northeast Liaoning province confirmed he started mining again in early Feb after CNY holidays, but the finished concentrates would only be available around the end of March. Extra domestic supply will divert mills from bidding for spot cargoes; so the negative influence on pricing is greater than additional overseas supply in the seaborne market.

■ Coal policy reversal. No 276 work-day policy for China coal for just now, despite lots of market chatter and “well-informed” sources recently telling McCloskey it was returning in mid-March. It seems the situation was fluid and there was a late change. We previously pointed out that thermal stocks were low, and the thermal price of Rmb610/t was above the target range. The NDRC apparently believes tightening supply now would be unwise. Spot coking coal prices lifted from mid-Feb on the 276 day view, as China snapped up cargoes. That $12/t HCC price gain is likely to be shed.

■ The press was wrong about Coal. So what other policy drafts may yet change? We have in mind the 30% winter cuts for alumina and aluminium. Reuters said this has been signed off. Where is the confirmation? A Platts trader source noted “We haven’t seen any documents, but we heard a government official has confirmed an announcement is ready to be made public soon; so let’s see. There is so many policies now we need to see it before we can be certain.” Hard to argue with that.

Mysteel has two domestic mine surveys that it undertakes – one in detail with 70 mines, and a larger survey of 266 mines but with less detail. It is the larger survey that shows the growth. The utilisation rate in early March was a little higher than Dec – in fact the highest production rate since Dec 2014. More striking is the fact that it occurred so early in the season. Normally mines slowly restart through March as the winter freeze dissipates. This time, the high price and early Lunar New Year holidays have allowed mines to limit the size of the February production dip and crank up output rapidly. With the price holding at high levels more starts are likely. Nobody knows what the cost base of Chinese iron ore mines are – particularly as every mine is unique and will have an individual cost base. However, a common estimate for the mines that previously closed and may reopen is somewhere in the vicinity of $70-$80/t. Certainly it seems an iron ore price exceeding that seems to be getting action while a price of $60-$70/t in 2H16 seemed not to achieve much. However, we don’t know how much production will restart yet.

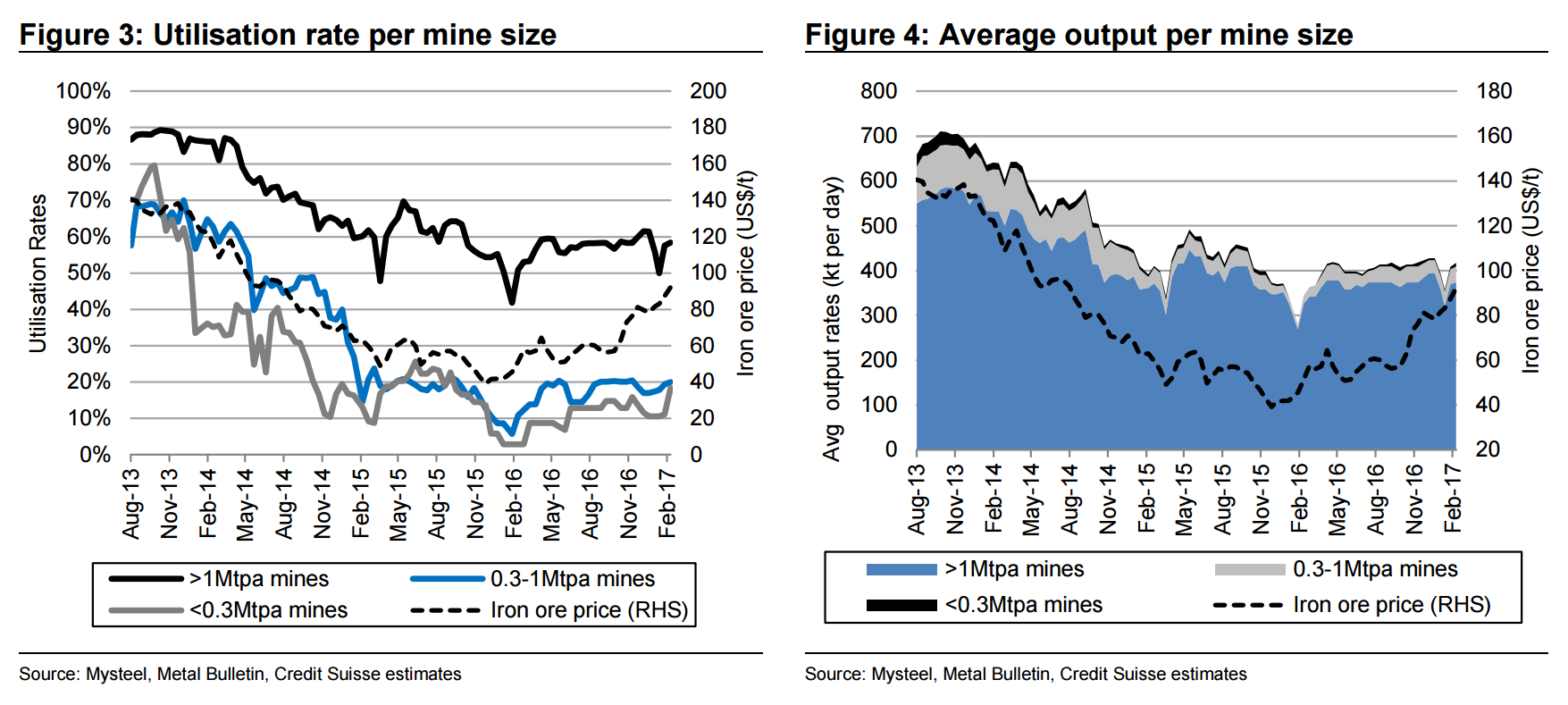

The 70-mine survey breaks mine up into three size categories. One interesting feature is that mid-size (300ktpa-1Mtpa) and small mines (300ktpa) seem to be picking up faster than the larger mines (Figure 3); these smaller mines were essentially gone in Feb 2016, but utilisation rates have now picked up to 20% of the historical maximum capacity. That is obviously a long way from the 70-80% of late 2013, but it is a start. And when we think about it, a small mine needing little equipment should be fast and easy to start whereas larger operations would take more time. It took three months to change the output rates at coal mines last year; so a closed mine should take at least that long. So perhaps there will be “big” (+1Mtpa) operations joining the mine restarts in a few months’ time. And big mines should make a difference. Figure 4 clearly illustrates the disparity in output by mine size. About 11 medium-sized mines would be needed to equal the output of one large mines, or perhaps 70+ small mines. So it is the larger mines we really need to be concerned with.

It took an iron ore price of $38 to knock them out last time and the yuan is -10% since then…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.