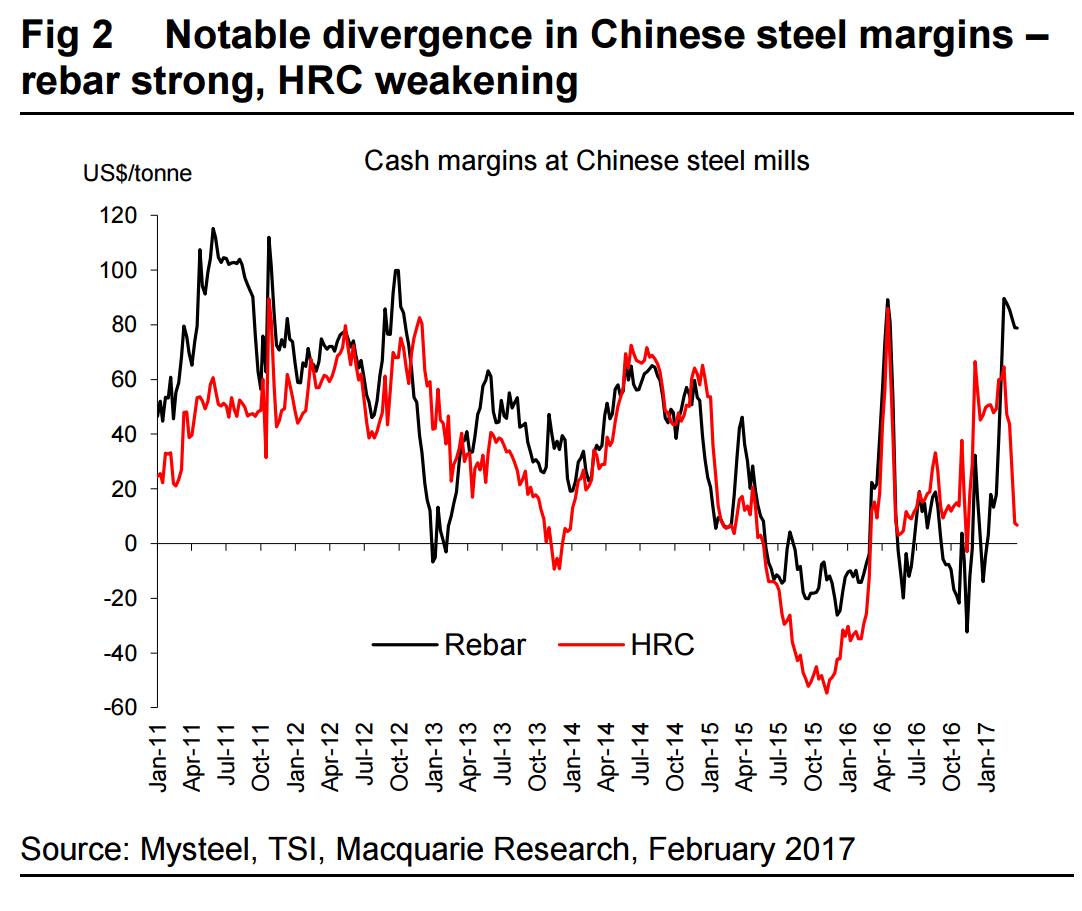

Our steel survey published at the start of last week was interesting in term of order books. Overall domestic orders were strong, but this was clearly led by construction and infrastructure. In contrast, orders from the white goods and machinery sectors were more sanguine. This disconnect is playing out in Chinese steel margins, with recent strength in rebar prices (coupled will falling iron ore) helping margins jump to levels last seen at this time last year. With steel trader inventory still drawing fast, at present there is clearly good demand from the construction sector. Towards mid-year, we think this could morph into a different story, as the effect of property tightening weakens sequential construction activity.

For HRC margins however, these are falling fast. And this is solely down to the falling domestic steel price, which has dropped ~300RMB/t ($35/t ex VAT) over the past two weeks. With Asian export market prices also falling, there is no easy out for Chinese flat product producers – unless inventory starts dropping quickly output will have to be curtailed. The relative weakness in flat products also suggests some of the Chinese strength seen during Q4 and early Q1 was down to restocking at downstream sectors. It is always hard to disaggregate the effect of this, but certainly the strong recovery in industrial profits has allowed some additional steel purchasing in expectation of better order books.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.