Home Capital Group Inc. extended declines after the Canadian mortgage lender reported additional deposit withdrawals, prompting one of its biggest rivals to seek a C$2 billion ($1.5 billion) credit line to stem any contagion across the country’s financial markets.

Home Capital fell 13 percent to C$6.96 in Toronto, bringing its two-week drop to about 69 percent, on concern that redemptions of guaranteed investment certificates by nervous investors would worsen a cash crunch. High-interest deposits have declined about C$1.6 billion, or 80 percent, over the past month to C$391 million, the companysaid Monday.

“They could be at risk,” said Jaeme Gloyn, an analyst at National Bank Financial Inc. “If investors are pulling their high-interest savings accounts, it’s natural to think that other clients would also be looking to pull their GIC investments.”

The selloff in Home Capital’s stock and bonds, sparked by allegations that it misled investors about its mortgage book, are raising concern that its funding woes may spread to other mortgage lenders. That could derail a red-hot housing market that’s been a key driver of growth for Canada’s economy, accounting for as much as a fifth of output.

Equitable Group Inc., another alternative mortgage lender, said Monday it took out a credit line with a group of Canadian banks after it started seeing “an elevated but manageable” decrease in deposit balances. Customers withdrew an average C$75 million a day between Wednesday and Friday. The withdrawals represented 2.4 percent of the total deposit base. Liquid assets remained at roughly C$1 billion after the outflows.

Let’s set the scene with comments from two blog dogs sitting on opposite sides of the real estate maelstrom. First a poster we’ll respectfully call Dick:

“People, don’t listen to Turnster, he knows nothing about nothing. If you bought into RE 1 year ago, 2, 5, 10, 15, 20 you are golden no matter what. Open your eyes and see for yourselves – RE in Canada will always be of value and will never go down in price. NEVER! There ain’t no bubble here. RE prices simply have caught up with the levels where they should have been in the first place. TO is a major cultural and economic city. I bought last years and it’s gone way up! And always will. And everyone will want to live here. The demand for RE will never dry up. NEVER!”

And here’s a further update from Derek, the dude who blissed out last month when his house went in a bidding war for lots more than he expected: $2.25 million. Then the buyer got cold feet while the other bidders fled. Lawyers are fighting. Derek’s in a funk.

“Well the shit show continues. Buyers did not even respond to our lawyer. We had hoped maybe they would come to their senses but have waited long enough. I just can’t believe peoples mentality. Stick your head in the sand and hope it goes away. So it looks like we are relisting on Monday.

“Really nervous that the market has changed and we will be at a terrible disadvantage now. Dealing with all this and maybe having to sue them is really not the way we had planned on having this happen. Most people I talk seem to feel that I will win if this is the outcome but obviously we are nervous.”

And finally, another dog who just sold for far less than anticipated after an attempt to create a bidding war failed. No offers – even for a detached in prime 416.

“At the beginning of April in this area there was a boat load of sales, before Ontario dropped the hammer. Since then, just four sales. Listings have tripled. Bidding wars being held, but no offers. Condos listings exploding. Now I just got to find a desperate owner willing to take a haircut on rent.”

Yeah, everyone sees reality through their own lens of experience. The guy who bought recently wants nothing more than validation for having made a sacrifice – which is exactly what it takes to buy into a bubble market. So he pumps, gloats and pumps harder. The person who wants to sell and can’t, sees nothing but disaster looming. The guy who swallowed a lump pf pride and took less, rationalizes the action. It’s impossible to know if the market switch has flipped from ‘Insane’ to ‘Scared,’ but something is afoot.

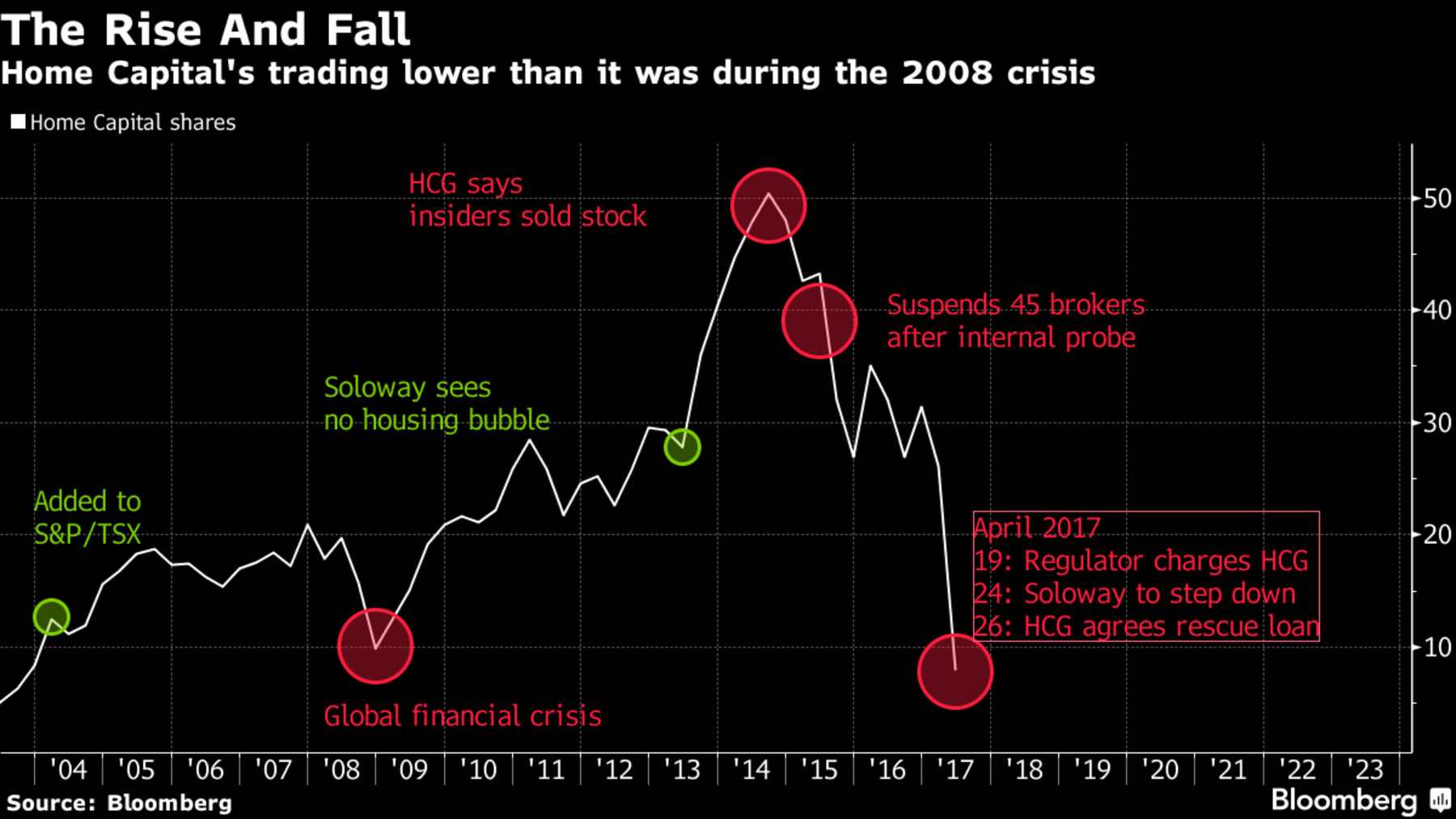

Days ago the savvy investment wonks at Mawer money managers sold almost three million shares in Home Capital Group, squeaking out the door before it shut behind them. The loss would be staggering, and now the company’s chief investment officer, Jim Hall, is saying some serious things about what the collapse of Home Cap might suggest about the whole mortgage financial business and even (gasp) the Big Banks.

Could the looming death of Canada’s biggest non-bank lender cause a run on deposits at other institutions as depositors start to understand their money went to finance a housing market that could blow up?

“The probability has gone from infinitesimal to possible — unlikely, but possible.” He told the Financial Post. “If depositors or bondholders start to lose faith in their banks, well then that becomes systemic.”

Yikes. Spooky words from a guy who manages $40 billion in assets. And while Home Cap’ mortgages represent just 1% of the entire Canadian home loan business, even little wounds are serious when you’re dealing with a system built on confidence. People blindly put their savings into the GICs and high-interest accounts of outfits like EQ Bank and Home Trust because they got a little more interest and were too trusting to ask when the cash went. (Most of it was loaned out to home-buyers who required high-ratio mortgages and didn’t qualify at the bank.) Now many depositors are desperate to get their cash back – and Home had to borrow $2 billion at usurious rates from an insider to stay alive. As a result, its stock plunged and the corporate carcass is now for sale.

See how it works? Not pretty. And fast.

There’s little doubt our big banks are secure, despite their jaw-dropping exposure to residential real estate. (If you want to worry, fret about the credit unions.) But the residential real estate market is just as susceptible to sharp U-turns in sentiment as GIC-holders in operations like Home or EQ.

On Friday US ratings agency Fitch hoisted a red flag over the GTA’s runaway, but conflicted, market. Ontario’s recent 16-point plan will bite, it says, and it could all start with those universal rent controls – since that market (as we’ve been telling you) has become dominated by speckers.

“The proposed rent controls could dampen price growth in the condo market if the rent investors can charge tenants is limited. Investors who are highly leveraged may be forced to sell, which could begin downward momentum that leads speculators to follow suit. Further, if all measures are passed, municipalities will have the power to introduce a tax on vacant units to encourage sales or rentals of unoccupied units, which may discourage speculators from holding onto vacant properties.”

Well, make up your own mind about what comes next. Dick has.

Advertisement

And from John Hempton comes some damn good advice:

Home Capital Group is an aggressive Canadian home lender that has hit a very rough patch. If you want a history Twitter will do it well. They have been fighting with Marc Cohodes (a very well known short seller) and you will find a timeline of the unfolding disaster by following Marc’s tweets. [Disclosure: I have known Marc for 17 years and we are friendly.]

The crisis came this week when Home Capital Group entered into an emergency loan. The press release is here – but the salient points are repeated below:

TORONTO – April 27, 2017 – Home Capital Group Inc. (“The Company” TSX: HCG) today announced that its subsidiary, Home Trust, has secured a firm commitment for a $2 billion credit line from a major Canadian institutional investor.

The Company also announced it has retained RBC Capital Markets and BMO Capital Markets to advise on further financing and strategic options.

The $2 billion loan facility is secured against a portfolio of mortgages originated by Home Trust.

Home Trust has agreed to paying a non-refundable commitment fee of $100 million and will make an initial draw of $1 billion. The interest rate on outstanding balances is 10 per cent, and the standby fee on undrawn funds is 2.5 per cent. The facility matures in 364 days, at the option of Home Trust.

The facility, combined with Home Trust’s current available liquidity, provides the Company with access to approximately $3.5 billion in total funding, exceeding the amount of outstanding High Interest Savings Account (HISA) balances.

Home Trust had liquid assets of $1.3 billion as at April 25, plus an additional portfolio of available for sale securities totalling approximately $200 million.

Access to these funds is intended to mitigate the impact of a decline in Home Trust’s HISA deposit balances that has occurred over the past four weeks and that has accelerated since April 20. The Company will work closely with the lender to have the funds available as soon as possible.

This on the face of it is an extraordinary loan. It is secured by giving the collateral and costs something between 15 and 22.5 percent depending on how much is borrowed.

Its also extraordinary because of what it does not mention. It does not mention who the lender is and it does not delineate what the precise capital is.

But we know that this is being used to pay High Interest Savings Balances. We know there is a run on the bank here here and the run is several hundred million dollars per day.

This is desperation financing. They are securing mortgages (average interest rate below 5 percent) to borrow funds that cost 15 percent or more. The negative carry is huge. A financial institution cannot stay in business under these terms.

The stock reacted – dropping 60 percent in a day. The Canadian exchange busted some trades about $8.20 (because it thought that they were done in error). Mine were amongst the busted ones. I was perfectly happy to sell at that price however in their wisdom the exchange thought that mine was a fat-finger trade. [Disclosure – transaction to sell 30,000 shares at 8.19 was reversed.]

But it is extraordinary because it gives the following details.

a). The loans are secured by 200 percent of their value in mortgages (which makes the investment almost riskless – and Mr Keohane goes to some lengths to describe how low the risk is), and

b). Me Keohane says the deal is more akin to a “DIP deal”. DIP stands for debtor in possession and he is thus saying the deal is bankruptcy finance.

This is an extraordinary position for Mr Keohane to take. He was an insider to both institutions (a true conflict of interest).

What he is saying is that he isn’t taking any risk because he has taken all the good collateral and he expects Home Capital go go bankrupt.

And note that he will make 15 to 22.5 percent return (more if the loan is repaid early in a liquidation) whilst taking no risk.

I have two words to say to this: fraudulent conveyance. In a rushed deal (one that truly surprised the market) done with undisclosed insiders up to four billion of the collateral and maybe three hundred million dollars of book value has been spirited away. And at basically no risk the recipient of all this largess.

Wow that was audacious. More audacious than just about anything I have ever seen on Wall Street.

Jim Keohane seems to recognise what he has said because almost immediately he says that he doesn’t know what the acronym DIP stands for.

That surprised me: Mr Keohane uses the phrase DIP Financing precisely and accurately and in context and then says he doesn’t know what it means. You should note that Mr Keohane is a very sophisticated fixed income player. (If you want a guide to how sophisticated read this…)

The position of the Canadian Government

The Canadian Regulator is put in an extreme bind. Up to $300 million of value has been spirited away from a highly distressed institution.

The regulator however has guaranteed a very large amount of funding of Home Capital (guaranteed deposits). They should be alarmed at up to $4 billion in collateral being spirited away to HOOP. This effectively subordinates the insured depositors and in the event of Home Capital’s failure will cost the taxpayer several hundred million dollars.

This is not an idle concern. The funding itself indicates that it is very likely Home Capital will collapse. And a former director described this as akin to DIP Financing.

If I were the regulator

If I were the regulator I would be doing my duty here. My duty here is to protect the taxpayer.

Very rapidly Home Capital needs to find a buyer to assume the government insured obligations. It does not matter if this happens at 20c per share. Indeed from a regulatory perspective it is better if it happens at a low share price because it gets rid of claims of bailouts inducing moral hazard.

If Home Capital cannot find a buyer then it should be liquidated. Immediately. And the transaction with HOOP should be reversed under standard bankruptcy rules for reversing fraudulent conveyance. There is no reason that taxpayers should accept subordination to a loan yielding 15-20 percent.

Indeed regulators have a duty to stop that sort of thing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.