The AUD was strong against developed market currencies last night:

And emerging:

Gold was firm:

Brent weak:

Base metals weak:

Big miners weak:

EM stocks stable:

High yield bogged down with oil:

US bonds sold:

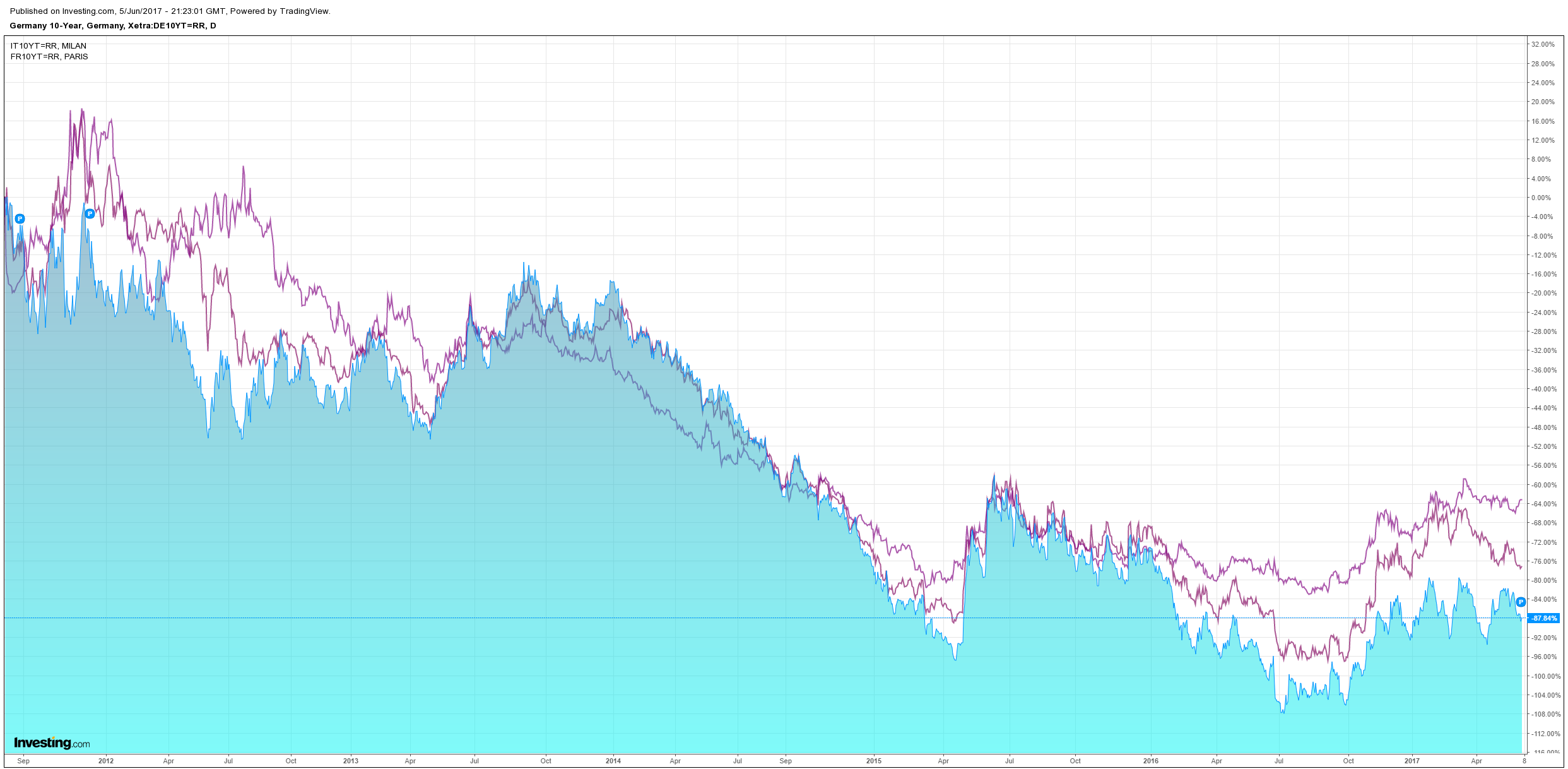

European spreads were stable:

And stocks eased:

Deutsche takes a useful look at where global markets are poised:

…[it] seems to be a perfect storm of so so growth and falling inflation, enough for the Fed to tighten modestly but being at risk of over doing it. The net impact is for financial conditions to ease via the soft dollar as term premium is tied down. And it is hard to see the Fed either taking a time out or accelerating tightening for fear of same said error.

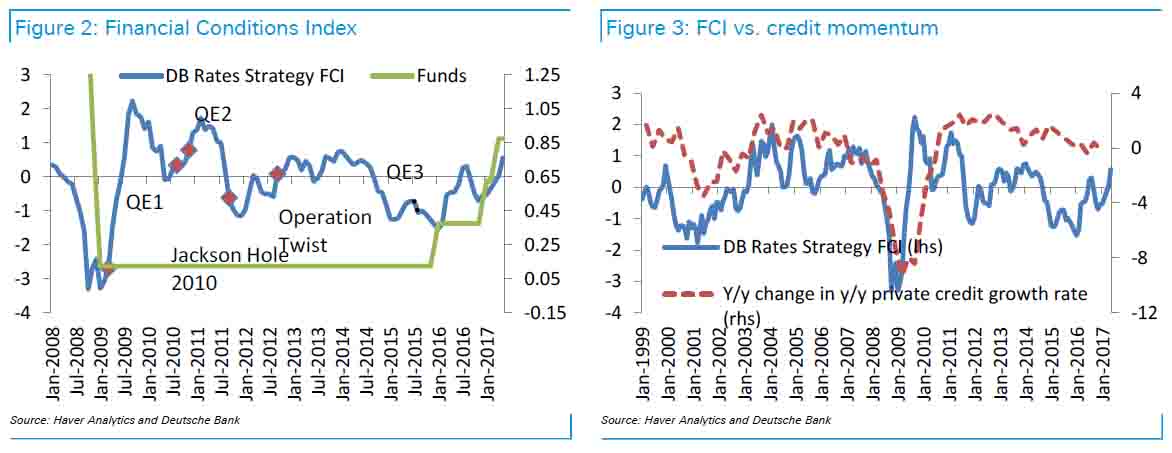

We think equities continue to move higher and bond yields lower. Financial conditions continue to soften. Our index was at peak tightening in January 2016, the index level was at -1.53 with the previous peak tightness -1.73 in February 2011, before twist and -3.29 October 2008. The recent local peak softness was November 2016 (-0.71). Since then the softening has been driven mainly by dollar weakness, contributing 47 percent of the easing in financial conditions. Mortgage spread narrowing and some recovery in FX reserves have each contributed another 20 percent or so in softer conditions while equities 7 percent. The irony is that faster Fed tightening has neatly coincided with an easing of financial conditions. One might be tempted to suggest that if the Fed wants to tighten financial conditions for fear of overheating the economy, it is going about it the wrong way. The logic here is that the (rates) market remains fearful that the Fed’s push for normalization runs the risk of lower inflation and weaker real growth that will undermine equity valuations. The self-inoculating response is therefore lower rates (5 years and out) and as we wrote last week, bonds act as a crutch to equities – equities are anyway cheap and whatever is good for the bond market at least since 2008 has never been sustainably bad for the equity market

Ironically, if the Fed wants to tighten financial conditions two possibilities would be an overt policy error to be much more aggressive and short circuit the mild expansion but without the smoking gun of inflation – that should see equity declines despite lower long dated yields with spread widening. Ironically the dollar might weaken as an offset. Or go the other extreme and take a time out to be more overtly behind the curve and allow higher inflation expectations via a steeper curve that might raise the dollar, soften equities and spreads (hunt for yield dissipates). Neither of these directions is necessarily guaranteed to succeed nor appear particularly appealing – and arguably the recent faster pace of tightening was supposed to look a bit like the former but is clearly back firing. The conclusion is that the Fed can’t do a lot that appears credible to the market. The path of least resistance is therefore a soggy dollar, low yields and robust equities.

We buy that so long as the fiscal hand-off remains. Especially so given falling commodities will keep deflating the global inflation pulse as China slows which means Australia misses out big.

The MB Fund pilot is allocated accordingly. Relative to MSCI:

- overweight European stocks;

- underweight US stocks;

- underweight Australian stocks;

- overweight Aussie bonds (creeping out the curve now);

- no property!

The MB Fund is launching July 1 2017. Those pre-registered will be invited in a little earlier. Register your interest today (if you have not already):