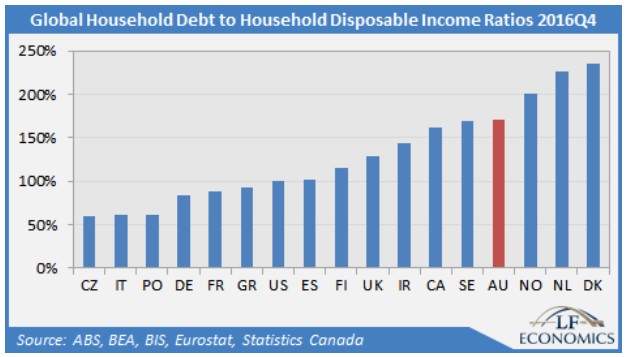

After taking the silver medal globally on household debt-to-GDP and bronze on aggregate principal and interest repayments to income, Australia has missed out on a medal and come in at fourth place globally on the measure of household debt to household disposable income, according to new research from LF Economics:

…our economy is like a drug addict. As the body becomes used to the drug, an increasing amount is required to achieve the same effect. With anaemic economic growth, policymakers cannot risk households deleveraging, which explains why the banking regulator APRA’s first and second rounds of macroprudential controls were very weak.

While the focus of household debt is in relation to GDP, household income is more accurate. Interestingly, all nations toward the higher end either have or had housing bubbles. In Australia’s case, this is unsurprising, given it currently has the world’s 2nd highest household debt to GDP ratio, the 3rd highest debt service ratio (DSR; measuring aggregate debt payments to income) and 4th highest debt to income ratio…

With the last round of productivity-enhancing policies implemented back during the 1980s, successive governments have relied on the mining boom, the FIRE (finance, insurance and real estate) sector boom and extreme population growth to artificially grow the economy. As the economic stimulus from investment relating to the mining sector subsides, policymakers have only the latter two elements to rely upon…

Economists have also yet to understand that it only takes a tiny percentage of mortgages to become non-performing to topple banking systems, as central bank research indicates. Focusing on the aggregate, median or average borrower is misleading as it is the small number of overleveraged borrowers at the margin that generates systemic risks.

Unfortunately, the political economy has mutated to such an extent it is impossible for policymakers to reverse the economy’s addition to private debt without causing severe withdrawal symptoms. It appears the nation may have to wait till the next recession or GFC 2.0 to deal with our problems, cold turkey style.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.