The Australian dollar kept on keeping on last night against both USD and EUR:

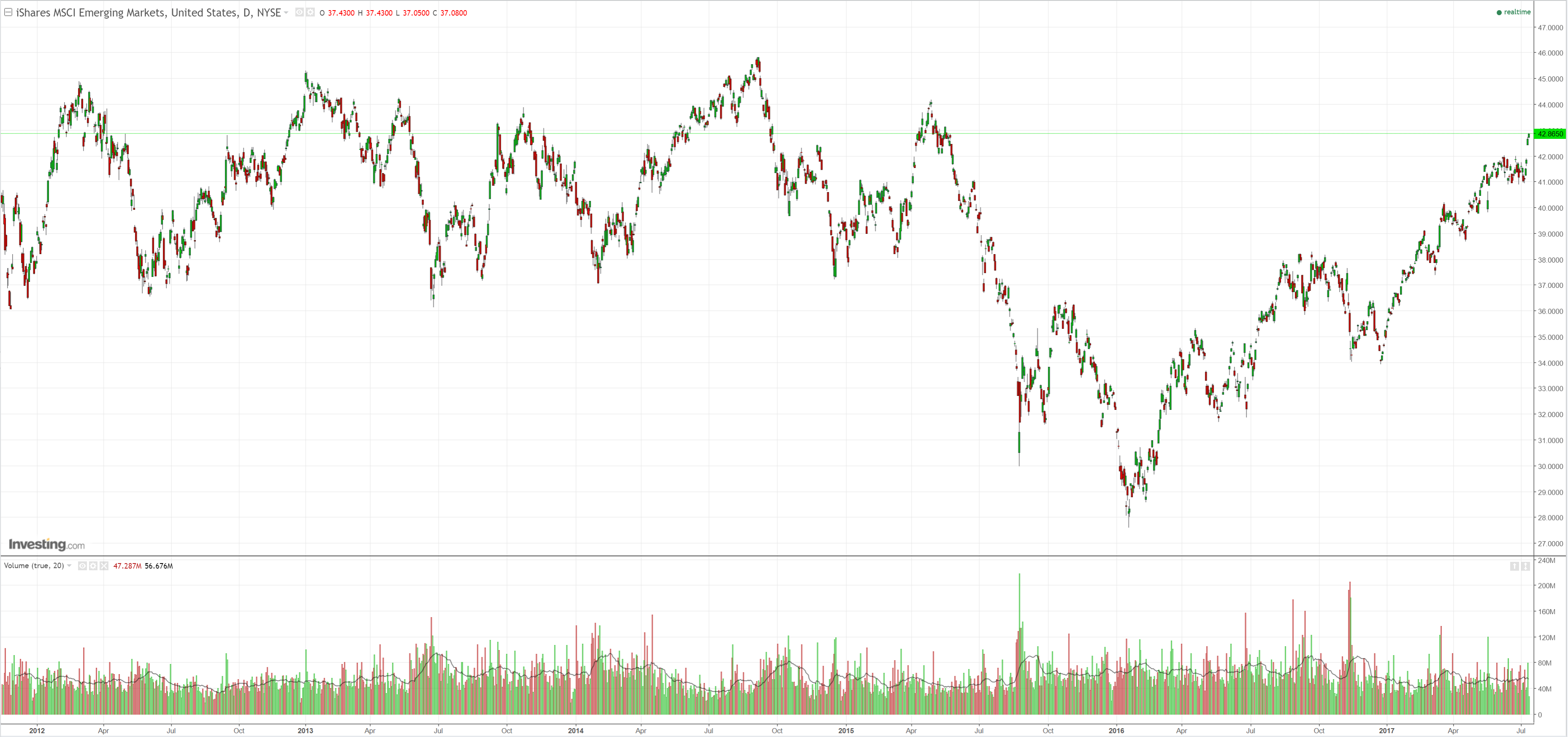

Against EMs it was mixed:

Gold caught a bid:

Advertisement

Brent too:

Base metals fell:

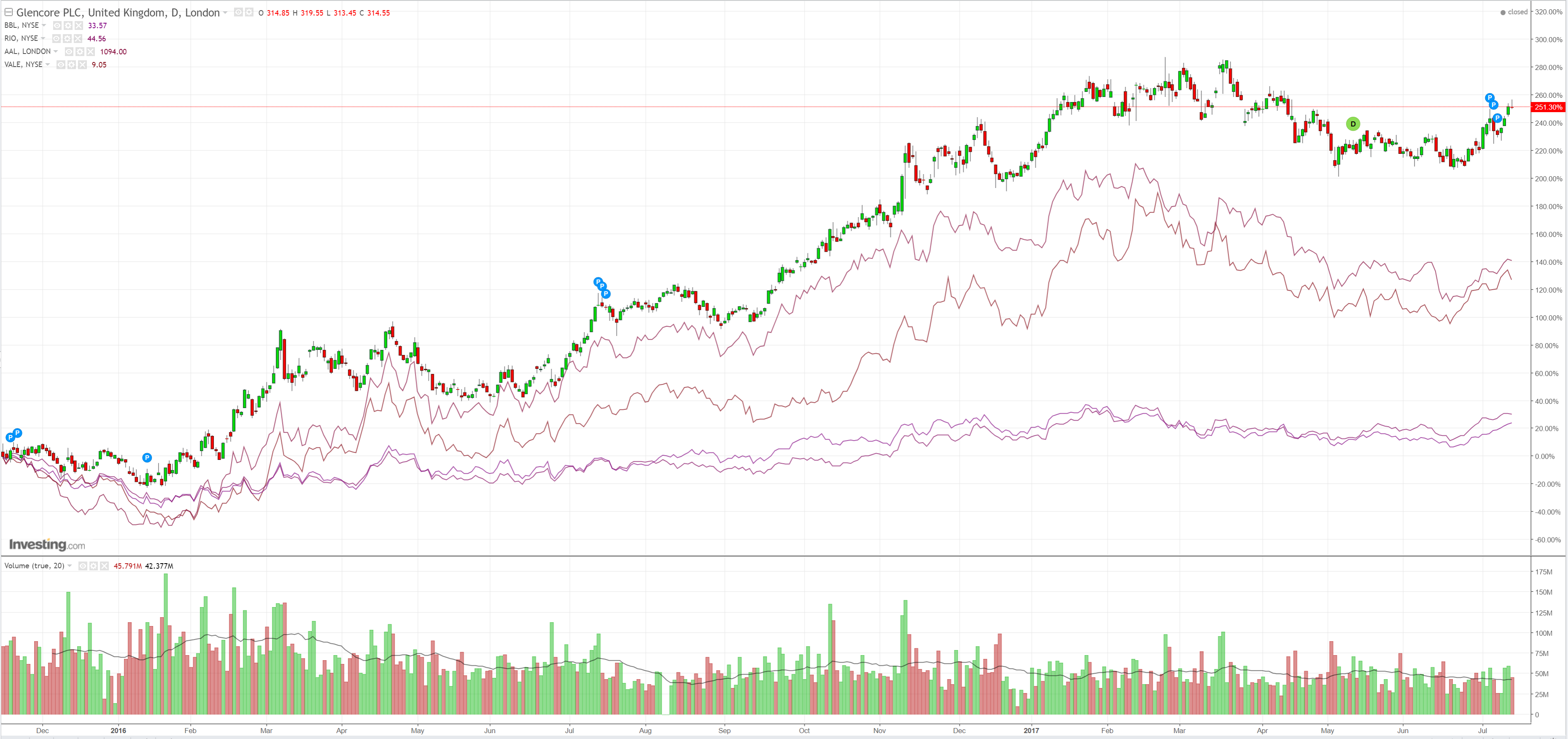

Big miners were mixed:

Advertisement

EM stocks took off:

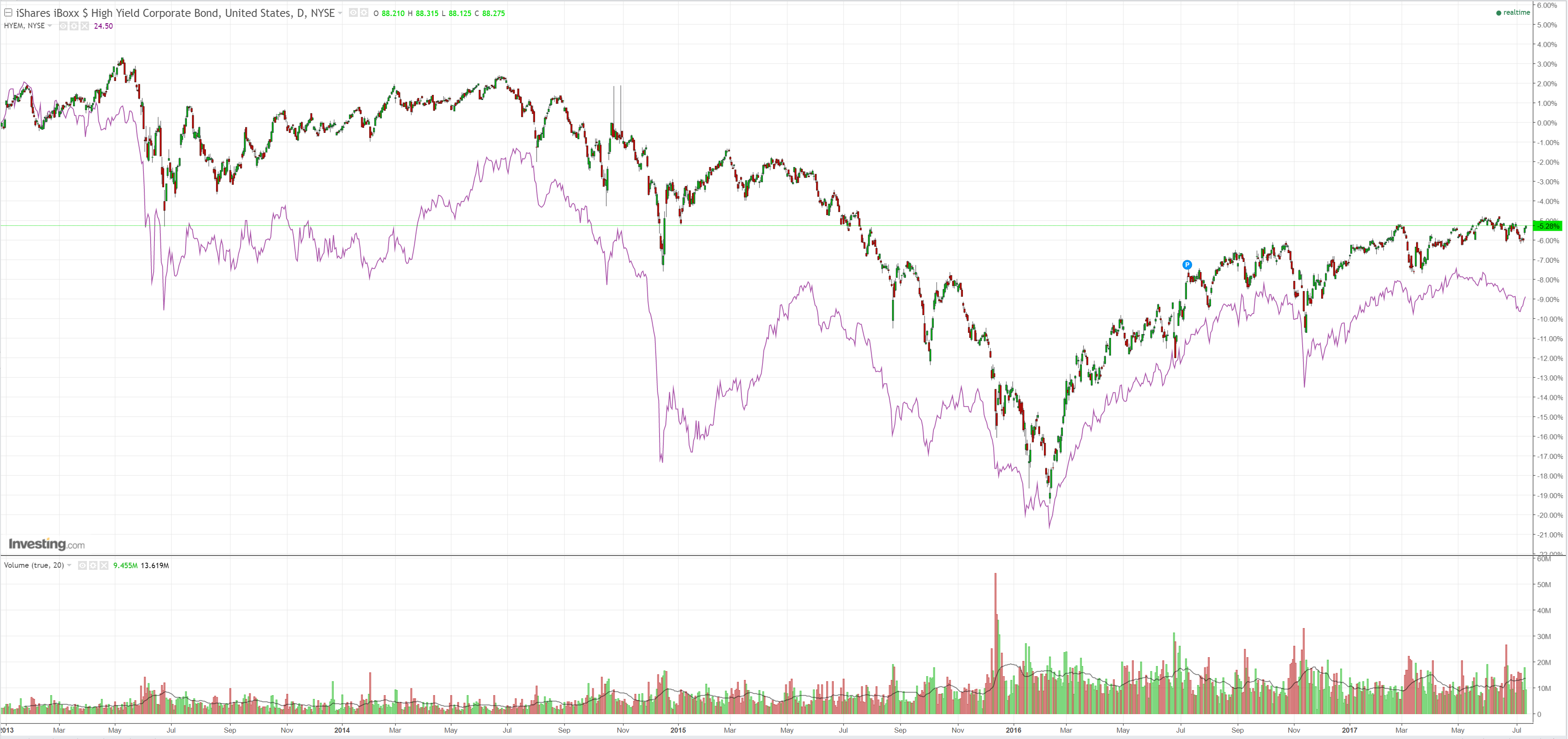

As high yield rebounded:

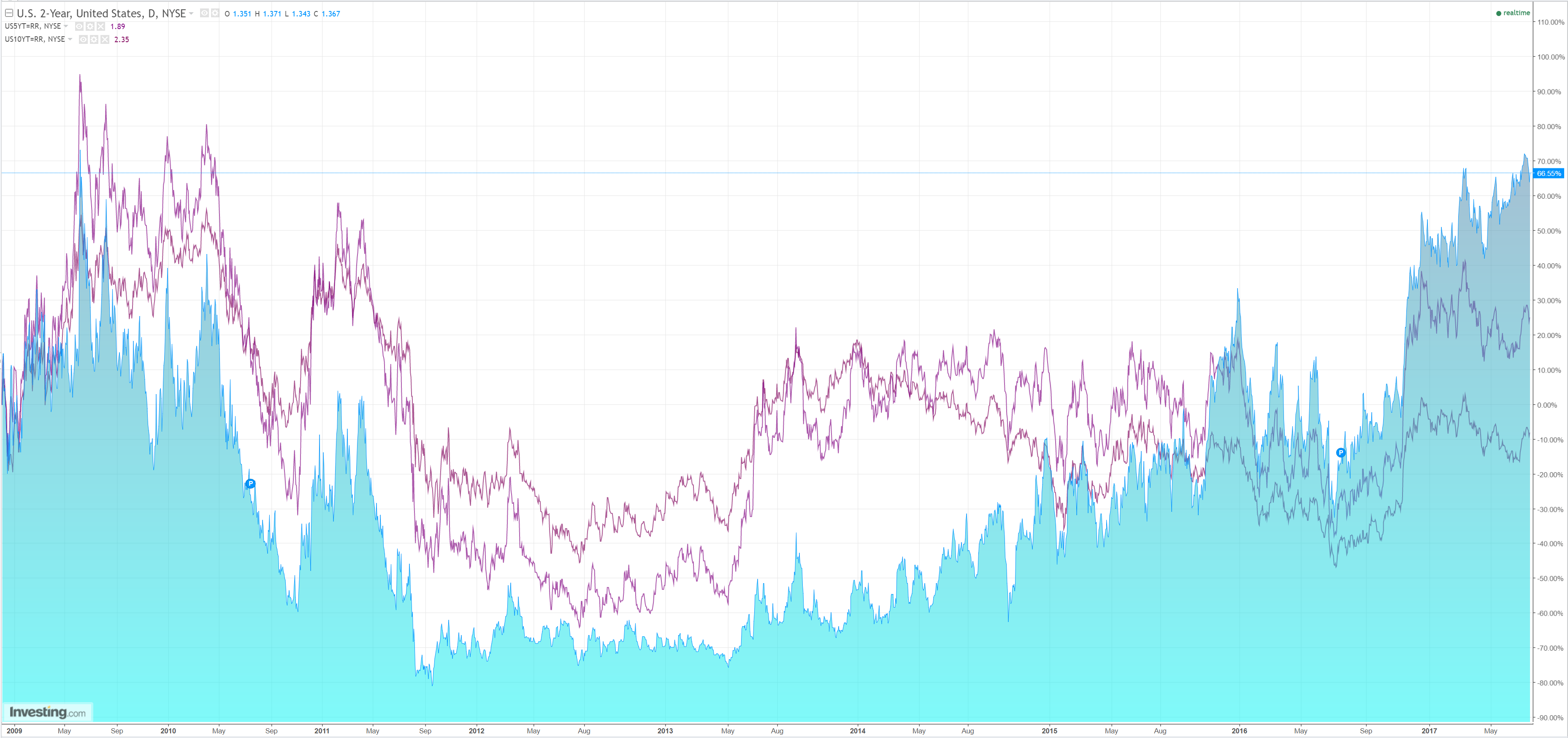

US bonds were sold:

Advertisement

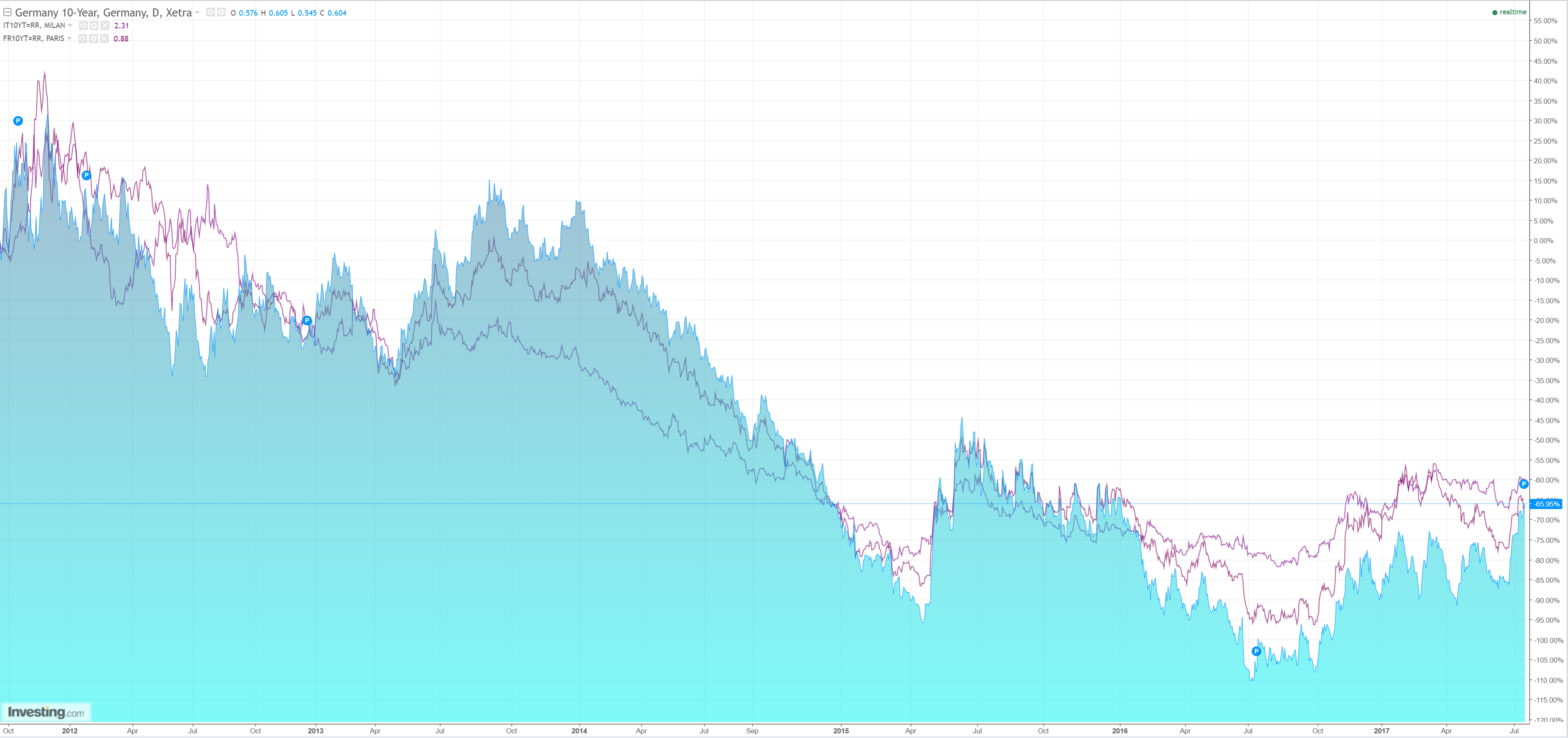

And European spreads all but disappeared as bunds were bashed:

Stocks firmed:

Advertisement

So, how high can the Aussie dollar fly? We’re an odds on chance of breaking above the 78 cents range for a little while. Soc Gen explains it nicely:

The main point of speculation about Fed Chair Janet Yellen’s semi-annual testimony to Congress may be about whether it was the shortest on record or not. The Fed plans to start reducing the balance sheet relatively soon (this year). “Additional gradual; rate hikes are likely to be appropriate over the next few years” told us very little. Neutral. Rates are very low but they will probably edge higher from here. I thought the observation that the fed isn’t interested in changing its inflation target but is keen to hit the target was perhaps the most interesting statement. This sounds a bit like a “cri de coeur”. Most of all, Chair Yellen’s testimony doesn’t support a lurch higher in real bond yields or in expectations about terminal fed Funds. The market has spent months guessing that the Fed will get rates above 2% but not as far as 3% and I didn’t hear anything to challenge that conclusion. So TIPS yields have once again made a short-term peak, are drifting in a range, as are nominal yields, and supporting risk sentiment across asset markets in general.

Jason Daw’s EM Strategizer sums it up. “It’s pretty simple…..don’t overcomplicate it…As long as US interest rates consolidate and fears about a move to well north of 2.5% remains in check, the positive tone in emerging markets that prevailed prior to mid-June should resume”. All I can add is that this as true of credit, equity and the broader FX market as it is of emerging markets. We get round two today, with the same (short) prepared remarks and a different set of questions.

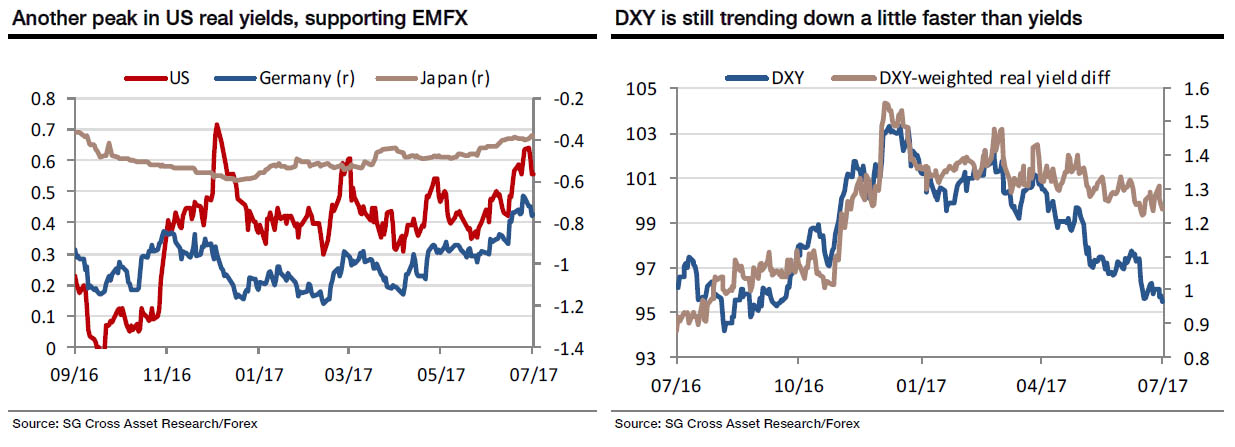

The divergence between US real yields and the dollar continues. DXY peaked at the same time as DXY-weighted relative real yields did, and both are falling. It’s just that the dollar is falling a bit faster than a dumb regression would suggest. That has now been true for just over three months and isn’t likely to change quite yet. The softer tone to US yields caps USD/JPY, but puts a floor under EUR/USD. EUR/JPY has drifted down a bit but not dramatically and while Japanese politics bears watching, we remain bullish for a move towards 140, with the next leg up probably coinciding with another leg up towards 1.16 in EUR/USD.

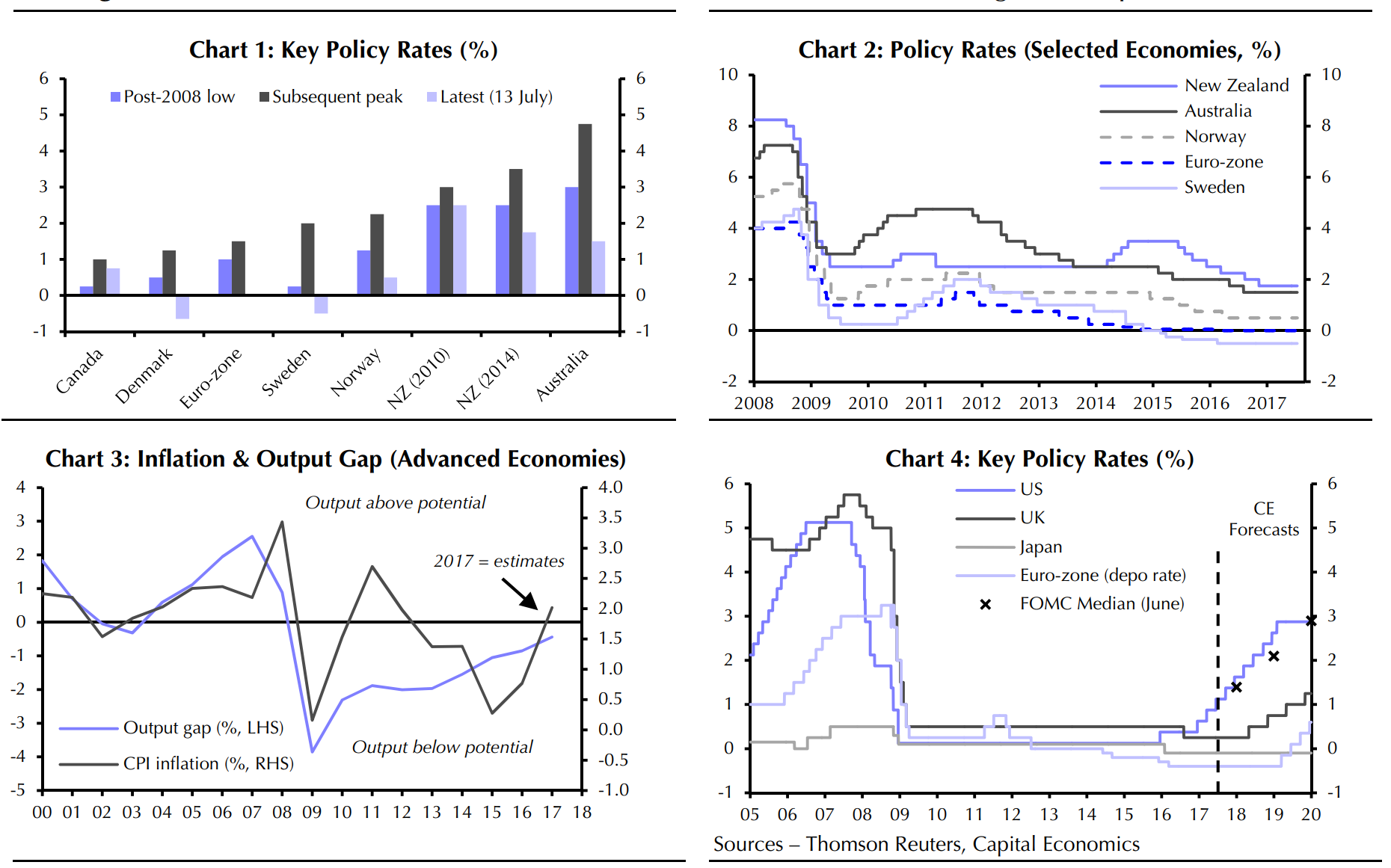

At some point the USD is going to stabilise but it has had too much monetary tightening priced given US shale is coming off, low wages growth and inflation and the fading fiscal hand-off. Conversely, not enough is priced in other jursidictions, from Capital Economics:

We suspect that the Bank of Canada will reverse yesterday’s rate hike next year, because we anticipate that the bubble in the country’s property market will burst. But there are good reasons to think that many other central banks will begin a more sustained tightening cycle, following the US Fed rather than the Bank of Canada.

The risk of policy reversal has diminished because there is a lot less spare capacity than a few years ago. The IMF estimates that the output gap in advanced economies was close to 2% of GDP during 2010-13, but is now much smaller. (See Chart 3.) And unemployment in many countries is close to the natural rate.

With this in mind, we expect most major advanced-economy central banks to raise rates before the end of 2019. Outside the US, policy-makers in the UK and Sweden are likely to start hiking rates in the second quarter of 2018, followed by Australia, the euro-zone, Denmark, New Zealand and Switzerland in 2019. (See Chart 4 and our latest Global Central Bank Watch for detailed forecasts.)

The pace of rate hikes is, however, likely to be slow. Core inflation has fallen sharply in Canada in recent months, and the Bank of Canada acknowledged that this has provoked “a lively debate…in many countries, about the appropriate interest rate settings.” We doubt that rate hikes in other economies will be reversed. But if inflation remains below target, policy tightening will be exceptionally gradual.

We can add that China is still sailing along OK, boosting all of the above ‘risk on’ narrative for EMs and commodities. In short, this is an echo of 2016’s commodity pain trade without oil.

But! It is not going to last very long. China is still set to slow at the margin by year end. It’ll be a slow slowing but will be led by construction so it will weigh materially on bulk commodities. We still think that next year will see more reform and further slowing. Europe cannot endure a higher currency for long before its externally-led growth eases and its inflation craters. And Q4 brings on ever more oil deflation as we pass through demand peak season with Libya, Nigeria and the US still raising output.

Thus, by year end it is probable that the US will resume its position as the growth and monetary tightening leader of the cycle and the USD firm up while the EUR stabilises and commodities, as well as EMs fall away. The one sticking point in this is the rising political risks around Donald Trump. His fiscal hand-off looks dead in the water today. Even so, with a lower currency and oil, US activity should be firm enough for its labour market to lead other DMs.

So, the rising Aussie dollar may well be a curse today for the economy but not necessarily for you. As it oscillates around its range highs, now remains a terrific time to get your money out. Over due course, we expect Australia to follow Canada into the housing downturn, and for the local economy to decouple from the global bounce triggering ASX under-performance, bond out-performance and a resumption of a weakening the currency.

This is a “carve out” of the International part of the above portfolios.

It is a core holding, designed to have a broad, diversified exposure to the world’s large capitalisation stocks.

Its intended for investors who wish to do their own asset allocation, and can use this fund to get exposure to higher quality and cheaper stocks.

Investors have the option to put an ethical overlay over this portfolio.

The minimum investment is $70k.

This fund maintains minimal cash balances – i.e. the tactical funds above will reduce share weights when stock markets are expensive or risky, whereas this fund will remain fully invested. It is up to the investor to manage the asset allocation when buying this fund.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.