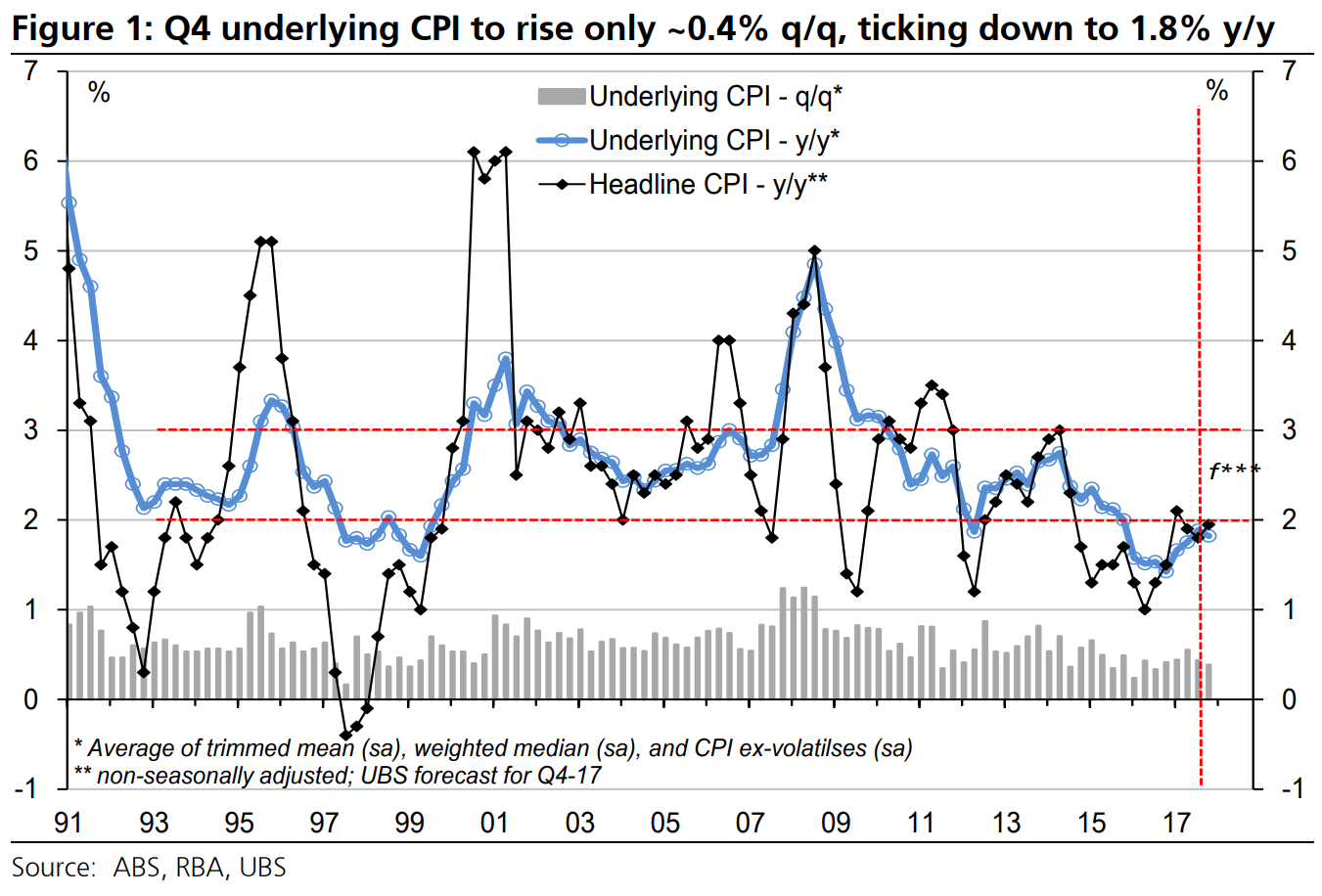

Based on our proprietary inflation survey, we are revising up our long-held topdown forecast for Q4 headline CPI (due on January 31) to an increase of 0.7% q/q (was 0.6% q/q initially). While this is the equal largest q/q since 2013, it is the same q/q rise as a year ago, and came after downside surprises in Q2 and Q3.

Our survey found that a few key swing factors, which are mainly to the upside, are driving higher headline inflation. Firstly, it appears that after Q3’s larger than expected decline, fruit & vegetables prices rebounded only modestly (+2%, +0.0%pts). Secondly the increase of the tobacco excise (+12.5% on 1 September) see’s tobacco (+7%, +0.2%pts) contributing strongly to CPI, despite a reduced weight in the 17th series. Thirdly, a strong rise in petrol of ~+8% q/q adds ¼%pts to CPI (Figure 5). Finally, domestic holiday travel & accommodation (+6%, 0.2%pts) rose strongly, in line with seasonal factors and the rise in oil prices.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.