By Gareth Aird, Senior Economist at CBA

Key Points:

- Strong employment growth, a lift in consumer sentiment and lower job security fears, as well as a recent pickup in retail sales suggests there are some green shoots to the outlook for consumer spending.

- But these are tempered by household indebtedness, weak wages growth and a saving rate with little room to move lower.

- We expect another year of modest consumer spending growth in 2018 which means a rate rise is unlikely to arrive until Q4.

Overview:

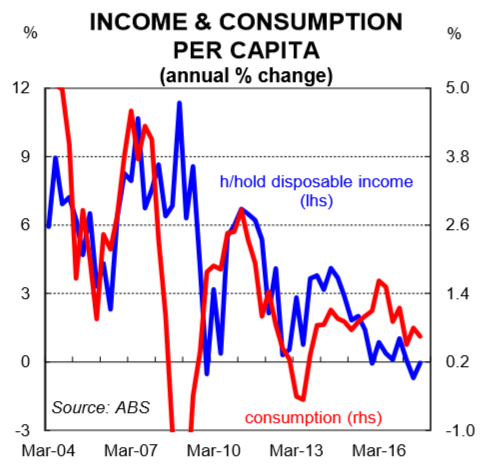

Last year was a relatively tough one for the Australian consumer. Despite very strong population and employment growth, overall spending growth was modest, primarily due to weak income growth (chart 1). Materially higher energy prices didn’t help either, particularly for households at the lower end of the income spectrum.

The hard data on households aligned with measures on consumer sentiment which suggested that confidence was brittle for most of 2017. This was in stark contrast to the business surveys which indicated the outlook had improved significantly. Indeed corporate profit growth was solid which differed from weak wages growth.

Over the past few months there have been some green shoots in the data with respect to the consumer. A few decent monthly retail numbers point to higher spending over Q4 2017. And consumer sentiment printed at its highest level since late-2013 in January. In addition, data on the labour market has continued to be strong. As a result, market pricing for a rate rise has firmed.

Ultimately household expenditure is driven by both the desire and the capacity to spend – the will and the way. Central to these outcomes for most households is: (i) having a job and feeling secure in it (i.e. employment); (ii) feeling confident about the economy and future earning prospects (i.e sentiment); (iii) income (i.e. wages) (iv) the level of indebtedness; and (v) wealth (largely influenced by dwelling prices).

Each factor is covered in this note under the umbrella of ‘the Good, the Bad and the Ugly’. Dwelling prices are considered the X factor to the outlook for consumer spending in 2018.

The Good

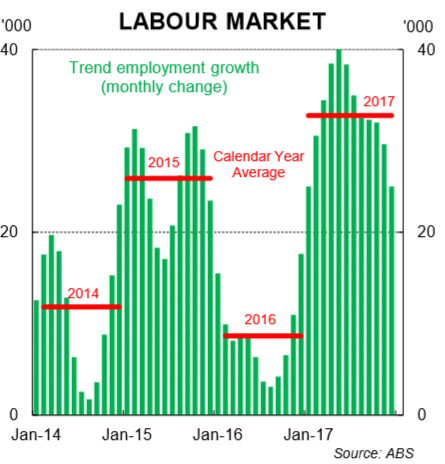

Labour market trends: Employment growth was phenomenal in 2017. The December employment report, published two weeks ago, capped a remarkable run of monthly job numbers. Over 2017 the ABS reports that employment rose by a staggering 403k (chart 2). Full-time employment (i.e +35hrs a week) rose by a whopping 303k while those in part-time employment rose by 100k. These are very strong numbers. And from a consumption perspective, more people in employment (both in absolute terms and as a share of the population) means more spending, all else equal

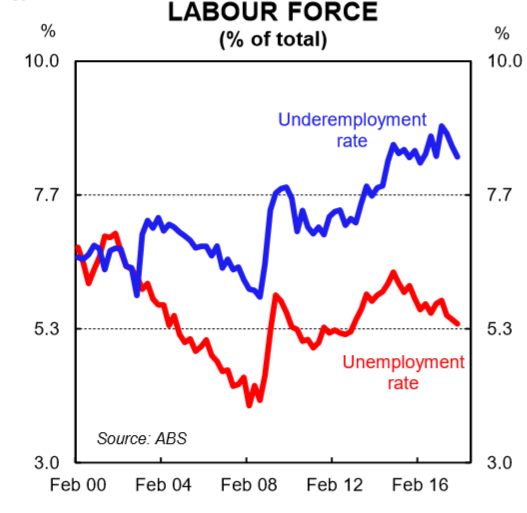

Very strong growth in employment, especially for full-time workers, has meant that labour market slack is receding. Both unemployment and underemployment rates fell in 2017 (chart 3) despite a strong lift in participation. A lower jobless rate is also positive for consumer spending.

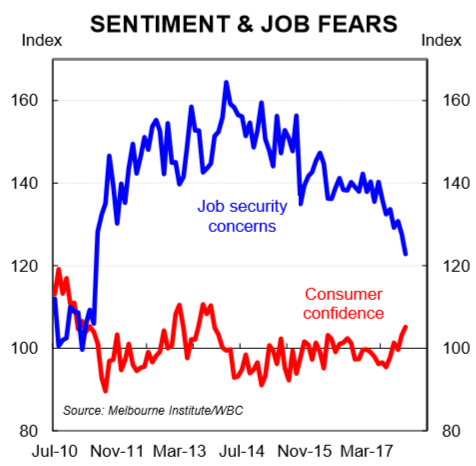

Consumer sentiment: The improvement in the labour market has propelled consumer sentiment higher and job security fears lower. The Westpac Melbourne Institute index of consumer sentiment rose by 1.8% in January to its highest level since November 2013 (chart 4). And the Unemployment Expectations Index fell to a 6½ year low (a lower read means a decline in job security fears). While the headline index isn’t suggesting consumer euphoria, it’s certainly an encouraging result.

The lift in consumer sentiment has narrowed the gap between business and consumer confidence (chart 5). Over time, divergences between consumer and business confidence tend to be ‘ironed out’ and the results converge. While it’s still early days, it may be that we are seeing the most desirable convergence – a lift in consumer sentiment rather than a fall in business confidence. On that score, the next few monthly reads on confidence will be telling.

The Bad

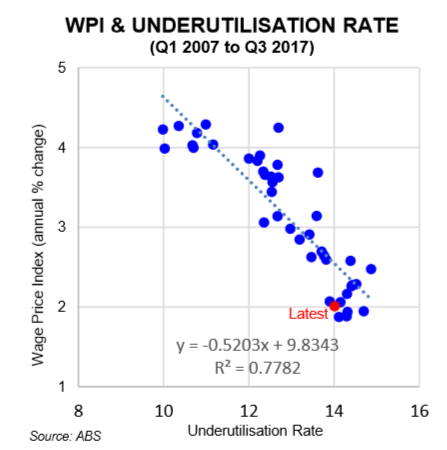

Wages: Growth in wages remains weak in Australia. The Q3 Wage Price Index (most recent) rose by just 0.5%. It was a particularly disappointing result given a solid lift in the national minimum wage of 3.3%, up from 2.4% the previous year, was supposedly in the figures. The gradual tightening in the labour market has not yet generated a lift in wages growth. Notwithstanding, wages growth is not too far below the rate that we should expect given the current level of labour market slack (chart 6).

Our forecast is for a modest lift in wages growth in 2018 as underutilisation continues to recede (both unemployment and underemployment are expected to grind lower). But it looks like that process will take time and as such, soft wages growth is expected to continue to be a handbrake on consumer spending (CBA expects a modest 0.6% q/q lift in the Q4 WPI).

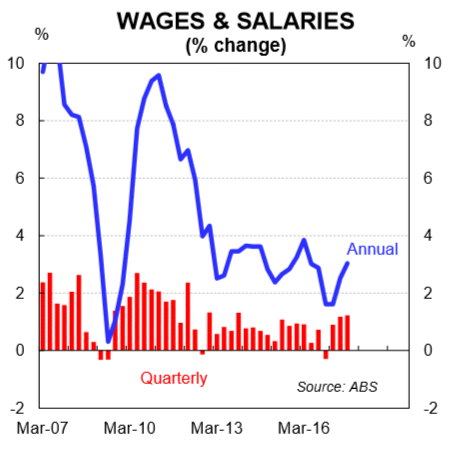

Having said that, the news on wages is not entirely all ‘bad’ when considering the lift in the number of people in paid work. The latest data on total employee earnings (i.e the total wages bill) is not as weak at the pure wage inflation figures. Compensation of employees rose by 1.2% in both Q2 and Q3 which annualises out at 4.9% (chart 7). The lift is being driven by headcount and therefore hours worked.

The data is essentially telling us that wages inflation has not yet lifted but total employee earnings have risen because there are more people in paid work. The latter provides some overall support to household consumption.

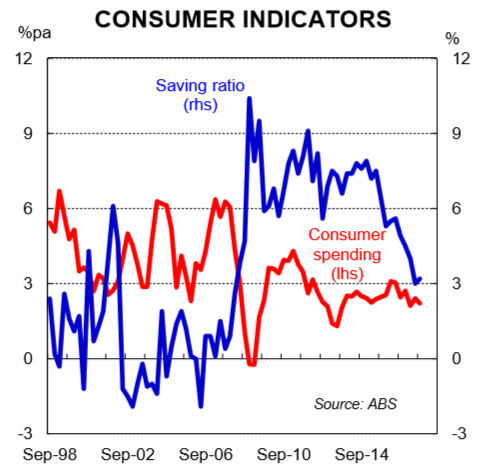

Saving rate: The savings patterns of households can be a big driver of consumption. In Australia, the saving rate1 has been trending lower since mid2014 (chart 8). This means that expenditure growth over that period has outpaced income growth. The saving rate is currently around 3% which means that households have very little scope to further reduce the proportion of income saved. Indeed, it is unlikely that the saving rate will fall much further given a softening in dwelling price growth (see page 3). This means that household income growth and consumption growth will converge.

Now it may be that household income growth will lift as the labour market continues to tighten. This would mean that consumer spending would be driven by an uplift in earnings rather than a fall in savings. Time will tell. But certainly from a starting position, the low level of the saving rate is suboptimal.

The Ugly

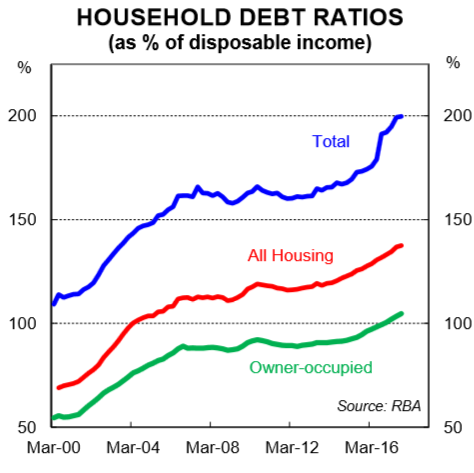

Household debt: “Ugly” is probably a little strong. But Australia has one of the most indebted household sectors globally and that’s certainly not an attractive trait. Debt to income has risen from around 148% in mid-2012 to a record high of 200% in Q3 2017 (chart 9). This measure includes all households regardless of whether they actually have a mortgage. For households that have a mortgage, that figure is significantly higher. It has increased steadily as interest rates have come down despite lower rates making it easier to repay debt. Basically growth in the net flow of credit (i.e. new credit less repayments) has been higher than growth in income thus pushing up leverage.

A high debt burden relative to income acts as a constraint on future household consumption growth. The “ugliness” of having a highly indebted household sector comes from the fact that interest payments as a share of income are higher than otherwise. And of course the principal must be paid too. This leaves households with less income that can be spent on goods and services. And it means that households have a much greater sensitivity to interest rate changes. From a demographic perspective, it is younger households feeling the debt burden most acutely.

Basically, an increase in debt relative to income means that the household sector has borrowed from the future to consume in the present. If debt is to fall as a share of income then households will need to reduce consumption as a share of income in the future. And since lower consumption means lower income (spending generates income) that’s a problem. In short, the future path of the Australian economy will have to contend with the headwind of a highly indebted household sector for a very long time.

The X Factor:

Dwelling prices: Changes in dwelling prices have an impact on the spending decisions of households via the wealth effect (the notion that changes in demand are influenced by changes in the value of assets). The theory states that when the market value of assets rise, it leads to the feeling of being wealthier which should encourage spending and reduce savings.

In Australia, the falling saving rate is evidence that a wealth effect has been in play. Now it may be the case that the saving rate declined simply so that households could maintain a modest level of consumption growth in the face of falling income growth. But the point to note is that firmer dwelling price growth gave those households that own property greater scope to reduce savings given their balance sheets were optically strengthened. Certainly there is a high likelihood that the reverse would be true and households would rein in spending if dwelling prices were falling.

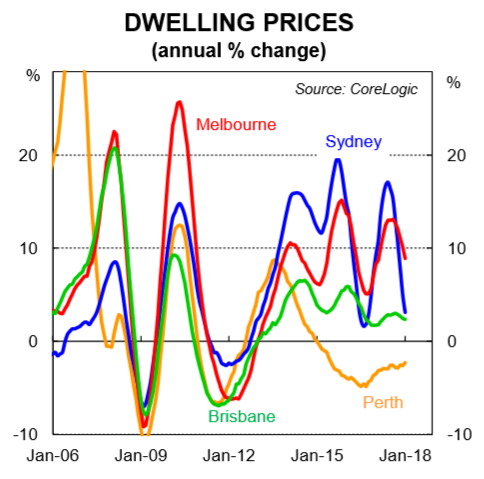

And that is the key X Factor in 2018. Dwelling prices nationally inched lower in late 2017 and annual rates of growth have slowed (chart 10). The risk of a further softening in dwelling prices looks higher now than it has been for a long time given: (i) rental yields are at historic lows; (ii) mortgage rates have lifted a little due to tighter lending conditions; (iii) credit growth has softened; (iv) auction clearance rates have been trending down; and (v) dwelling supply is in the process of lifting quite significantly in some jurisdictions.

A soft correction in dwelling prices would probably have no material negative impact on consumption. But there is a risk that a harder correction in prices (a fall of 10-15%) could weigh on consumer spending via a negative wealth effect. As such, the most desirable outcome from a macroeconomic perspective is for dwelling prices to move sideways over 2018. Indeed, that is our central scenario.

The Outlook

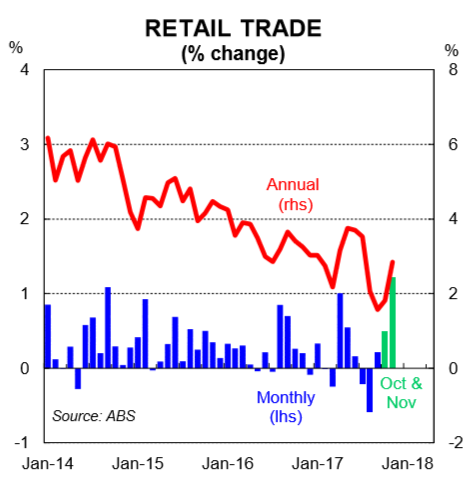

The October and November retail trade reports are the partial consumer spending data that has so far been published for Q4 2017. These reports were strong. Sales growth lifted by a robust 0.5% in October and a very large 1.2% in November. While iPhone and “Black Friday” sales were behind the November spike, the combined lift in sales over the two months points to a solid and welcome quarter for the retail sector. Recall that retail spending fell by 0.2% (nominal) in Q3.

The key question is whether the two most recent retail trade reports are a turning point or just some noise in the data. We think that it’s a little premature to say that it’s a turning point given we saw a similar five months of retail data at the beginning of 2017 (a weak Q1 followed by two big rises in April and May). But the data is certainly encouraging. And this time around it’s been accompanied by a lift in sentiment.

Overall, there are some green shoots in the data. But the backdrop of a highly indebted household sector is here to stay. The labour market has tightened, but we are still waiting for a lift in wages growth. As a result, we expect another year of modest household consumption growth in 2018. We have a lift of 2.2% in our forecast profile (the same as our expected outturn for 2017).

Other parts of the economy have picked up, notably business and public investment, but that isn’t enough to warrant a monetary policy response. Our view on rates continues to be aligned with the consumer and as such we don’t think a rate rise is likely until late 2018. Current market pricing ascribes a 50% chance of a hike by August. A rate rise is fully price in by November.