Because nothing says safe haven like a North Korean hack, via Quartz:

North Korea is no stranger to cryptocurrencies: The rogue regime has been accused of launching a global ransom attack to raise bitcoin, hacking South Korean exchanges, and mining crypto both within its borders and secretly on your computers. Now, it has become a suspect in the world’s largest crypto heist, Reuters has reported.

South Korea’s national spy agency told a parliamentary committee on Monday that North Korean hackers may have been behind the theft last month of about $530 million worth of digital tokens from Japanese exchange Coincheck, according to the Reuters report, which cited anonymous sources.

On Jan. 26, Tokyo-based Coincheck said someone hacked into its digital wallet and made off with more than 520 million units of a digital currency called XEM, affecting some 260,000 customers.The company admitted that they weren’t using all the necessary security measures, and promised to use its own money to reimburse customers. Japanese authorities announced that they would investigate all local crypto exchanges for security gaps following the breach.

North Korea is believed to be using cryptocurrency to get hard cash amid UN sanctions that are likely putting pressure on its cash reserves.

According to a September report from security firm FireEye, North Korean hackers targeted at least three South Korean crypto exchanges with the suspected intent of stealing funds last year, and one of the attacks was successful. When Seoul-based Youbit filed for bankruptcy after losing 17% of its assets in a cyberattack in December, South Korean investigators also looked into North Korea’s possible involvement in the hack.

The South Korean agency also briefed parliament on Monday that North Korea’s theft of cryptocurrency from the South last year was on the scale of tens of millions of dollars. According to Korea Herald and Chosun Ilbo, citing a lawmaker, North Korea used bogus job application forms to hack customers’ passwords.

The hacking at Coincheck is so far the biggest cryptocurrency theft on record. Tokyo-based Mt. Gox, which filed for bankruptcy in 2014 after lost about $480 million in a hack, was previously the largest heist.

More new lows last night before a bounce:

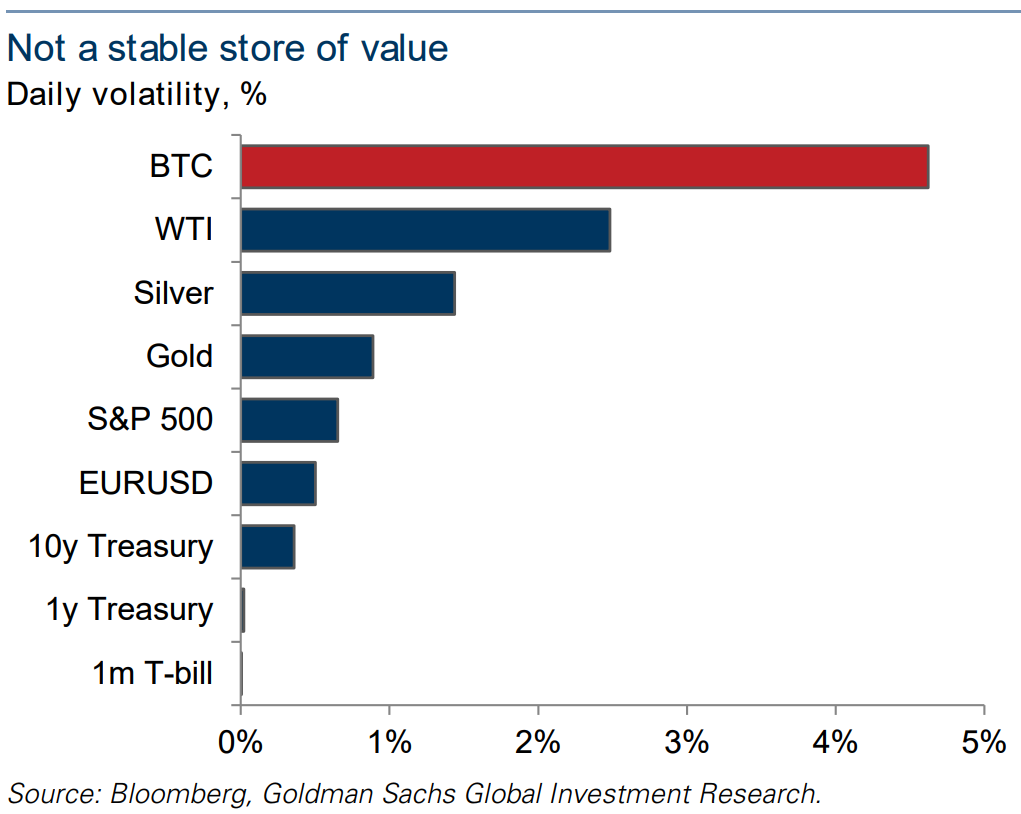

I think we can safely say at this point that BTC is neither virtual gold, a safe haven nor a store of value. Given it’s not a medium of exchange, either, then that leaves it looking pretty naked.

Advertisement

The US SEC is closing in. SEC Chairman Jay Clayton said in a Senate committee yesterday:

…Many of these assertions that the federal securities laws do not apply to a particular ICO appear to elevate form over substance. The rise of these form-based arguments is a disturbing trend that deprives investors of mandatory protections that clearly are required as a result of the structure of the transaction. Merely calling a token a “utility” token or structuring it to provide some utility does not prevent the token from being a security.

…It is especially troubling when the promoters of these offerings emphasize the secondary market trading potential of these tokens, i.e., the ability to sell them on an exchange at a profit. In short, prospective purchasers are being sold on the potential for tokens to increase in value – with the ability to lock in those increases by reselling the tokens on a secondary market – or to otherwise profit from the tokens based on the efforts of others. These are key hallmarks of a security and a securities offering.

Hello securities regulation. Goodbye ICOs.

Advertisement

Even the Great American Bubble Machine is turning against it, via Goldman:

Here, we dig deeper into the key question for investors currently contemplating the space: What is the value of cryptocurrencies themselves? The answer should help determine whether cryptocurrencies are a speculative bubble in the midst of bursting, or an innovation so transformative that its value is not yet reflected in the market price.

We begin by sitting down with Dan Morehead, founder and CEO of Pantera Capital, an investment firm focused exclusively on cryptocurrencies and one of the largest institutional investors in crypto to date. Not surprisingly, Morehead is a diehard crypto aficionado who believes that cryptocurrencies have enormous disruptive potential across financial services and money transmission. He sees cryptos as competitors to correspondent banks, credit card companies, conventional stores of wealth like gold, and fiat currencies. Assuming bitcoin captures some market share from each of these incumbents, he estimates its fair value could be roughly $500,000 (no, we did not mistakenly add zeros).

In Morehead’s view, it is therefore difficult to call recent cryptocurrency price action a bubble. And the potential for new market entrants in the form of institutional investors—which are essentially non-existent in the space today—gives him confidence that the price of cryptos will be substantially higher a year from now. What could quash his enthusiasm? Adverse regulatory action.

In a nutshell, we are more skeptical on the fair value of bitcoin and its peers. For one, Charlie Himmelberg and James Weldon of the GS Global Markets Research team argue that cryptocurrency price action and investor behavior fit the classic definition of a speculative bubble. In contrast to Morehead, they see the contagious enthusiasm for crypto among mainly retail investors as a telltale warning sign—the equivalent of daytraders buying anything ending in “.com” in 1999.

And while some observers have argued that the recent launch of bitcoin futures marks an important step in legitimizing cryptocurrency investing, GS Capital Markets Analysts Alex Blostein and Sheriq Sumar point out that futures alone cannot address some of the key market structure barriers facing crypto investors, particularly at the institutional level. Establishing reputable custody services, ensuring central clearing in the spot markets, and addressing connectivity risks—among other issues—will take time.

Steve Strongin, Head of GS Global Investment Research, thinks institutional investors should be worried about more than just bubble risks or market structure. In his view, the more important question is whether today’s cryptocurrencies will exist five or ten years from now. His answer? It’s possible but not probable, for the same reason that almost all of the first internet search engines are now defunct: Something better replaced them. That doesn’t mean blockchain technology—or some successor to it—won’t eventually play a larger role in the economy; in fact, we see potential applications for blockchain across industries (see pgs. 18-19). But in Strongin’s view, it does suggest that the cryptocurrencies that don’t survive are likely to trade to zero—a risk that seems broadly underappreciated in the market today.

But even if that ends up the case, is there any way of knowing which cryptocurrencies—current or future—will have more staying power than their peers? GS Payments and IT Services Analyst James Schneider argues that different crypto use cases could provide some insight. For example, it is almost certain that only a very small number of coins could succeed as media of exchange, given that success depends on widespread acceptance. On the other hand, special-purpose tokens being developed for various distributed applications could probably co-exist in greater numbers.

All that said, the above begs the basic but crucial question of whether any cryptocurrency could actually derive value from acting as a currency or a commodity—the key to understanding its ultimate potential. In our view, this depends on what economic problem cryptocurrencies solve. As a currency, GS co-Head of Global FX and EM Strategy Zach Pandl and co-Chief Markets Economist Charlie Himmelberg argue that in most places where well-functioning fiat currencies and banking systems exist, there seems to be no obvious problem to solve and thus limited use for cryptocurrencies. But they do conclude that in corners of the world where this is not the case, cryptos may be a viable alternative.

As a commodity, GS Head of Global Commodities Research Jeff Currie and team also find some instances where cryptos solve an economic problem—if that problem is efficiently storing wealth outside of the established banking system. But that use case is likely to be most valued, again, in places with unreliable banking systems, as well as in dark markets. When it comes to acting as a store of value in regulated markets, gold remains superior to bitcoin and its peers, in their view. And a long list of hurdles remains for that to change.

Honestly, if you can’t interest the Squid to leverage into a bubble then you are way off the reservation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.