March was all about interpreting widening interbank credit spreads, and making guess work of trade protectionism. The mainstream view seems to be that trade protectionism is the fat tail risk driving markets at present, and that interbank credit spreads will settle down soon, because US Treasury bill issuance is in the process of peaking out. But what if spreads in aggregate do not settle down? Will analysts then pull the trigger and start talking about a broader liquidity crisis?

In recent notes, we argued that tightening USD liquidity conditions are the clear and present danger to global markets, with trade protectionism rhetoric almost acting as a smoke screen. We also suggested that tightening USD liquidity conditions may actually be a smoke screen for deeper credit issues in Australia.

Here, we update our models to demonstrate that the emerging USD shortage is getting worse – and not just for portfolio reasons. Rather, the US trade deficit is in the process of peaking, irrespective of what happens with trade policy. The marginal supply of USDs to the broader world via the US trade deficit is about to shrink, adding further pressure on economies and institutions abroad dependent on USD funding.

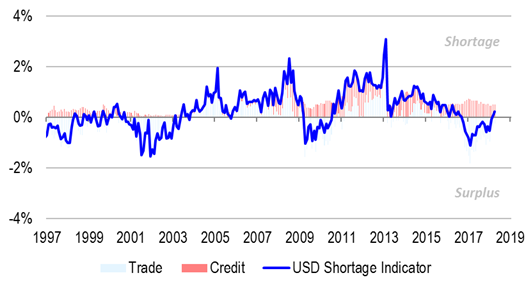

USD shortage is getting worse

Our proprietary USD shortage indicator is based on two variables:

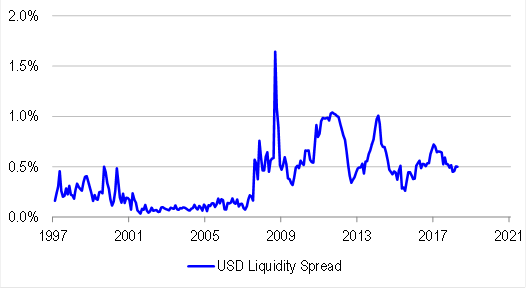

1. A GDP-weighted average USD liquidity spread based on US LIBOR-OIS and cross-currency basis swap spreads.

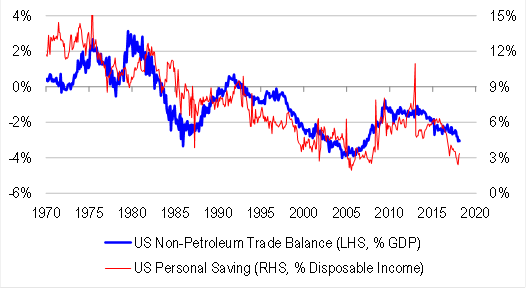

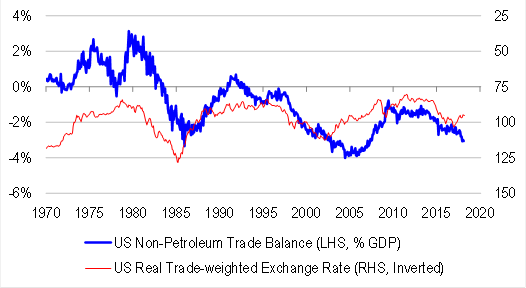

2. The projected change in US trade balance based on leading indicators (such as the real exchange rate and saving rates).

Recently, the indicator has moved further into shortage territory because the US trade deficit is in the process of peaking:

1. The US trade deficit has become larger. From the higher starting point, it is harder to grow.

2. The US household saving rate has risen, even after removing the impact from delayed tax refunds. Higher saving and weaker consumption is consistent with weaker imports demand and a smaller trade deficit.

3. The impact of previous USD weakness is starting to mechanically reduce the trade deficit by making exports more competitive relative to imports.

In other words, the future marginal supply of USDs via trade is likely to be smaller than it is today, contributing to tighter USD funding conditions. At the same time, spreads remain elevated. Therefore, our overall indicator has tightened further to its highest level since mid-2016.

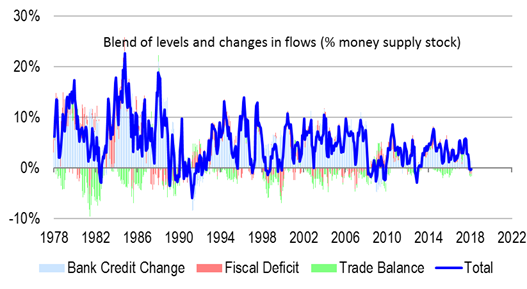

Australian credit impulse is still negative

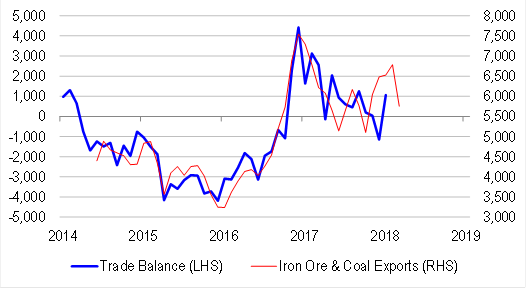

The most direct way that a USD shortage can impact Australia is via the trade balance. A shortage usually puts pressure on Chinese demand for commodities, weighing on the trade balance. Timely partial indicators suggest that the Australian trade balance is in the process of peaking, at much lower levels than it did in early 2017. This is because commodity prices have fallen sharply, while volumes have started to deteriorate in response to weaker demand.

A weakening trend in the trade balance represents a tightening of financial conditions because national accounting identity, private sector saving must equal the sum of the trade balance and fiscal deficits. In other words, if the trade balance is deteriorating, the private sector is saving less in foreign currency terms, contributing to a cashflow squeeze.

At the same time that the trade balance is deteriorating, fiscal policy has tightened. Federal government officials are celebrating an early return to budget surplus. But the flipside is that the government is creating less AUDs for the private sector to use, because when it (deficit) spends, it does so on “overdraft-like” terms with the RBA. This too represents a tightening of financial conditions.

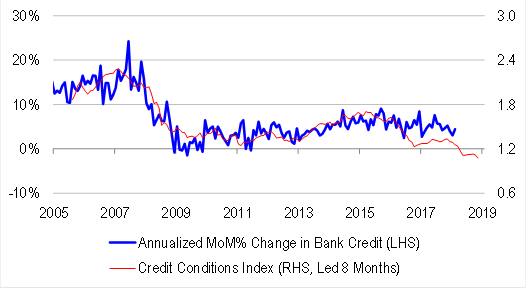

In the background, private sector credit growth remains moderate. Going forward, tightening funding conditions are likely to weigh on business credit growth, while macro-prudential tightening is yet to fully impact housing credit growth. We expect to see slower credit growth going forward, compounding the recent tightening of financial conditions.

Our proprietary credit impulse indicator aggregates trade, fiscal and credit developments at the margin. Levels and changes in the credit impulse matter, and so we present our blended measure. In early February, the (blended) credit impulse was slightly negative, consistent with relatively tight financial conditions and slower growth. For further discussion of our credit impulse indicator, please see our recent article “Credit impulse turns slightly negative” dated 5 March 2018.

Investment implications

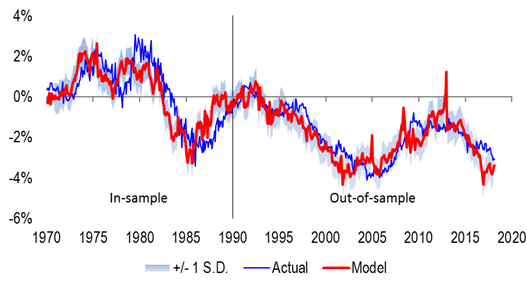

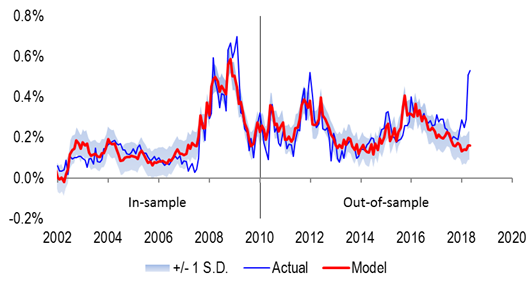

We are wary of an emerging USD shortage at the same time that the Australian credit impulse is deteriorating. We worry about latent de-leveraging risks. Indeed, AUD-denominated interbank funding conditions remain very tight, with spreads hitting new and “unexplained” highs. The Australian 3-month bank bill-OIS spread is now at 53bps, the widest level since the financial crisis. Importantly, the spread cannot be explained by conventional macro factors, such as the slope of the yield curve, corporate credit spreads or stock market volatility. Indeed, the spread of spreads to model is at historical highs (for further discussion of our interbank credit spread model, please see our recent note “Unusual money market tightening”, dated 12 March 2018). Nor can it be explained strictly by tightening USD funding conditions, because AUD-USD cross-currency basis swap spreads are very healthy (at positive, rather than negative levels), and in any case, banks do not strictly need USD funding.

But what we cannot explain using conventional factors, we can explain using unconventional factors. The deviation of credit relative to bank lending standards (both in level and change terms) is a powerful leading indicator of the residual in our spread model. With credit growth remaining positive against the backdrop of much tighter lending standards, credit has become excessive, even relative to bank’ own standards, and interbank pricing has started to respond.

More optimistic commentators argue that it has been the surge in secured lending rates (repo rates) that has driven unsecured lending rates (BBSW) higher, and that this is all a temporary phenomenon. But these same commentators offer no explanation for why secured lending rates have gone higher. To be sure, they do point to increased foreign demand for Australian government bonds, making it harder to obtain these bonds for secured lending purposes. But why has foreign demand for Australian bonds risen? We suspect that foreign investors are expressing an unusually negative view about local growth dynamics.

Regardless, we worry about the fact that interbank credit spreads remain very wide, impairing the monetary transmission mechanism, and reinforcing de-leveraging pressures. In a de-leveraging environment, asset prices drive fundamentals rather than the other way around. Naïve value factors stop working as a result. Instead, higher multiple, quality stocks tend to outperform as investors search for safety.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.