Forget Universal Basic Income, just raise Newstart

Greens leader, Richard DiNatale, has been rubbished by economists for proposing a socialistic “universal basic income” (UBI) scheme in his Press Club Address yesterday. From The Australian:

Greens leader Richard Di Natale’s policy to abolish all existing welfare and introduce a “universal basic income” — a non-means-tested payment to all citizens — would require federal public spending to rise by $254 billion a year, or by almost 55 per cent…

Social researcher Ben Phillips — who modelled for The Australian the cost of paying all residents aged 15 and over $23,000 a year (the Age Pension) and children $5500 a year (the maximum rate of Family Tax Benefit A) — said the plan was “utopian”. On his analysis, all marginal income tax rates, including the current zero-rate on incomes up to $18,200, would need to rise by 33 percentage points to pay for the proposal, bringing the top rate on incomes above $180,000 to 78 per cent.

“One of the claims of UBI advocates is that they remove the high effective marginal tax rate,” Mr Phillips said. “To some extent that’s true but the majority of taxpayers move to even higher effective rates”…

Independent economist Saul Eslake said Senator Di Natale’s policy, announced at the National Press Club yesterday, was an “extraordinarily expensive way of seeking to address what may well be a few cracks through which a limited number of people fall”.

Peter Whiteford, social security expert at the ANU, said Australia already had the most targeted social security system in the OECD…

Privately, senior Greens conceded an effective UBI payment would need to be between $20,000 and $40,000 a year…

I think Saul Eslake’s comment that UBI is an “extraordinarily expensive way of seeking to address what may well be a few cracks through which a limited number of people fall” sums up the Greens policy perfectly.

The main shortfalls of Australia’s social security system are as follows:

- the Newstart (‘Dole’) allowance for the unemployed is highly inadequate and should be significantly increased; and

- the Aged Pension is too generous to those with significant wealth, but not generous enough to those with few means, thus warranting a shift in payments.

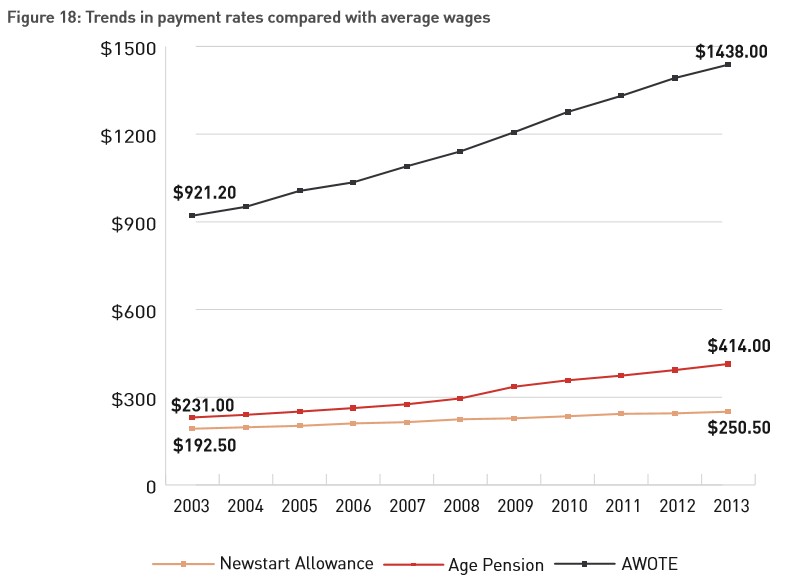

As shown in the next chart, the Newstart Allowance has not increased in real terms (i.e. above the Consumer Price Index) since 1994. This means that people who are unemployed have not shared in increases in living standards received by the rest of the community for more than 20 years.

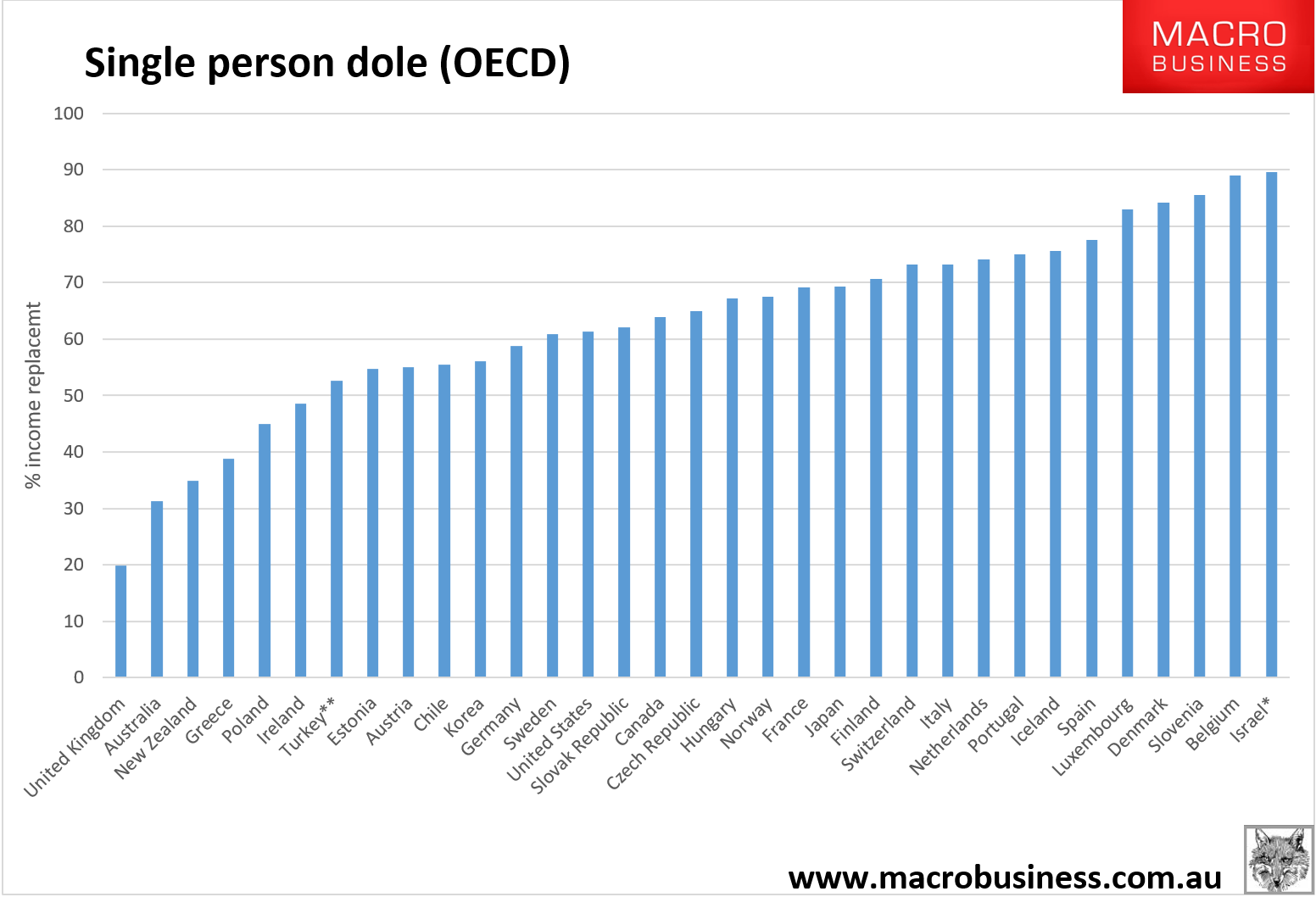

OECD comparisons also shows that Australia’s dole allowance is amongst the lowest in the world for singles:

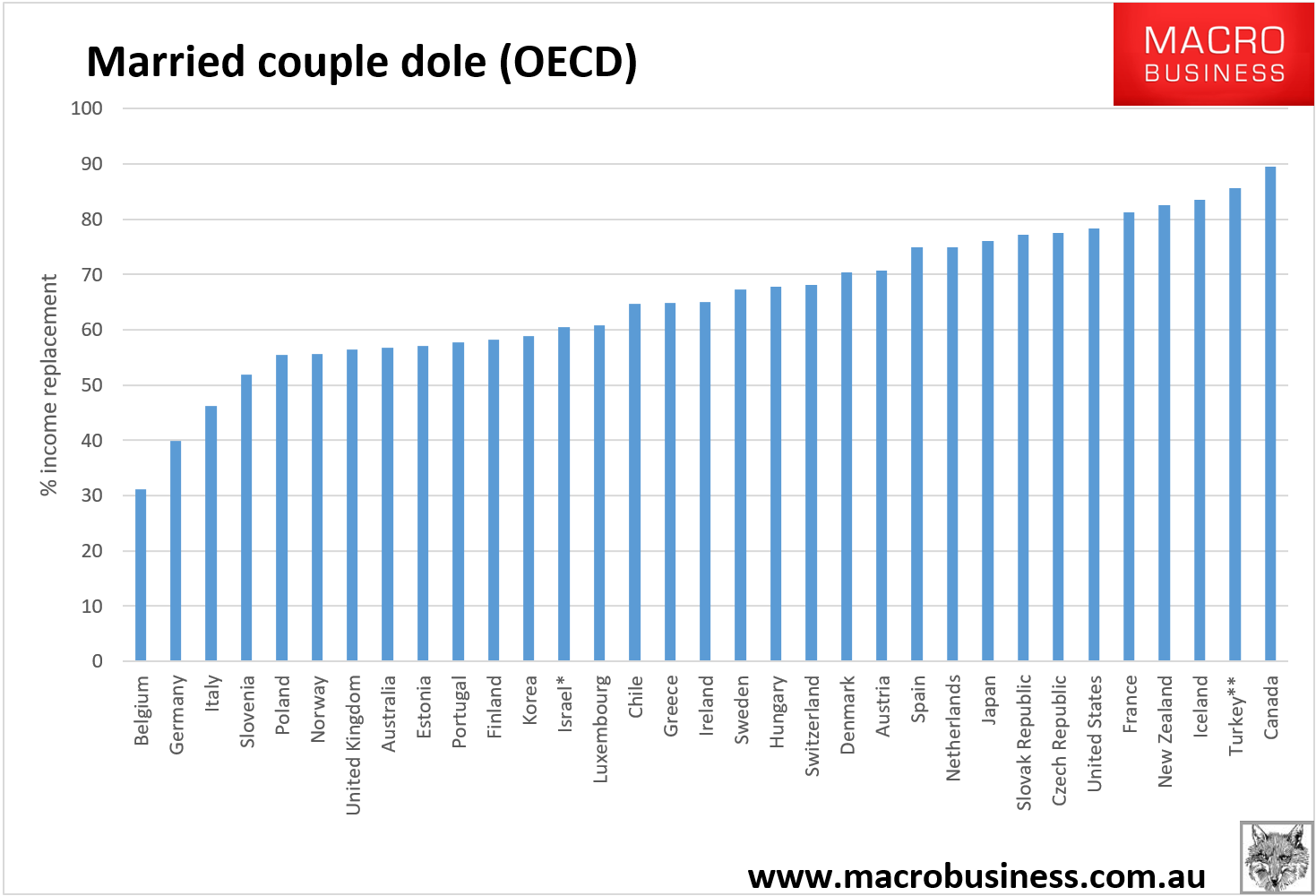

Whereas it’s only a little more generous for couples:

Whereas it’s only a little more generous for couples:

It’s also worth highlighting that the Business Council of Australia (BCA) has recently called for “increasing the inadequate Newstart allowance, arguably the most tightly controlled corner of the welfare budget”, as has KPMG, which has also described Newstart as “inadequate” and called for it to be raised by $50 a week.

When even the BCA is calling for Newstart to be raised, you know there’s a problem.

The problems around the Aged Pension relate more to its distribution. That is, while older Australians generally have captured an increasing share of Australia’s wealth:

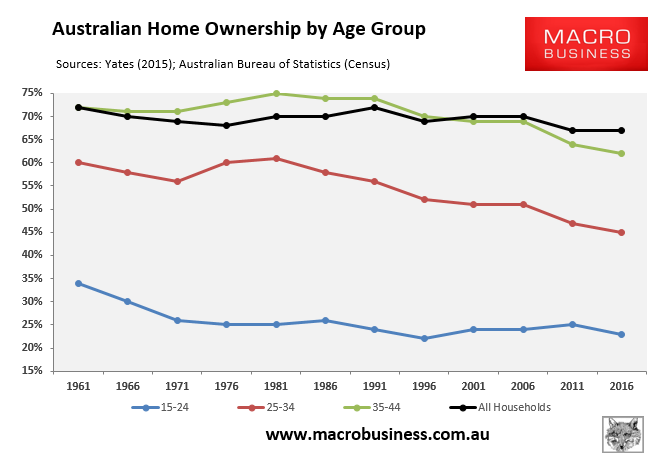

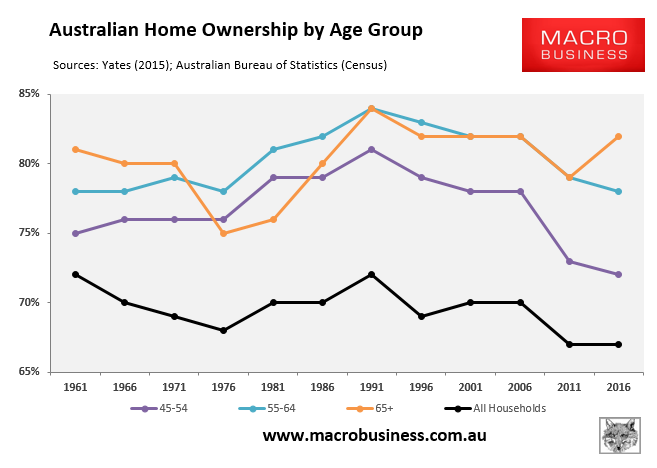

Largely because they have increased their home ownership rates over the past 55 years at the same time as home values have skyrocketed:

The situation is nowhere near as rosy for Australia’s renting pensioners, who are doing it increasingly tough, according to a recent reports from Mission Australia, The ABC. and the Swinburne Institute for Social Research.

Therefore, there is a clear case for broad reforms to both the housing and the Aged Pension systems.

On the housing side of the equation, there is a clear need for greater public investment in social and community housing, as well as reforms to taxation arrangements to boost affordable housing via targeting negative gearing at new builds (similar to Labor’s policy). We also need rules that give greater security of tenure to renters, like those that exist across much of Europe.

Regarding the Aged Pension, it should be reformed to provide less taxpayer assistance to wealthy home owners and more assistance to renters, via:

- Including one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Once implemented, raising the overall assets test for the Aged Pension, and the base rate as well.

- Extending the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive a regular income stream as they do now under the Aged Pension, but with less longer-term drain on the Budget and on younger taxpayers. At the same time, the circa 20% of renting pensioners would receive greater financial assistance – both via and expansion of the assets test and an increase in the base rate (see here for a detailed examination of this issue).

These are the types of social reforms that The Greens should be pursuing, not daft socialist plans like UBI.