Westpac: Political uncertainty to weigh on Australian jobs growth

From Bill Evans, chief economist at Westpac:

The Reserve Bank Board meets next week on August 7.

It is certain to keep the overnight cash rate unchanged at 1.5%.

While the decision will be accompanied by the usual statement from the Governor the more interesting development for the RBA will be the release of the detailed (around 70 pages) Statement on Monetary Policy on August 10.

The Statement is always interesting because it includes the Bank’s updated forecasts for GDP; headline and underlying inflation; and the unemployment rate.

In addition there will be an extension of the forecast period to cover the year to December 2020 from the May Statement which only covered forecasts to the end June 2020.

On GDP we expect the Bank will retain its upbeat forecast for growth to December 2018 of 3.25% (recall that the March quarter saw growth of 1.0%) – a view that is particularly underpinned by a positive outlook for employment. We discuss some risks below.

It is also likely to retain the 2.75% forecast for the year to June 2018 implying the Bank expects growth of around 0.6% in the June quarter. On the basis of the 1.6% for the first half of 2018 the second half will need to average around 0.8 percentage points per quarter to achieve the 3.25% forecast.

Westpac is more circumspect expecting 0.5 percentage points for the June quarter and an average of around 0.6 percentage points for the September and December quarters to achieve an annual growth rate of 2.7% for 2018.

Recall that the March quarter was boosted by a contribution from net exports of 0.35 percentage points whereas the partials are pointing to a notably smaller contribution from net exports in the June quarter.

From our perspective the more important structural signal from the March accounts was the choppy performance of household consumption (an insipid 0.34% growth in household consumption following a strong 1% in the December quarter).

By retaining the 3.25% growth forecast for 2018 there is no reason to believe that the Bank will be dissuaded from its 3.25% forecast for 2019.

The current forecast for the year to June 2020 is a modest slowdown to 3% presumably reflecting a peak in the boost from LNG exports and a likely modest drag from housing construction. We would expect the Bank to extend that 3% forecast for the full year to 2020.

So the important point is that the Bank is expecting GDP growth to be above potential for three consecutive years, with potential judged to be around 2.75%. A reasonable outcome from such persistently above trend growth would be to see the output gap close sufficiently to generate some lift in inflation and a marked fall in the unemployment rate.

In that regard the Bank’s forecasts are cautious. In May it forecast underlying inflation to remain “stuck” at 2% for 2018; 2019; and only reach 2.25% in the year out to June 2020.

With the June quarter Inflation Report confirming that annual underlying inflation remained “stuck” around 2% there will be no reason to change the inflation forecasts in the May SOMP with the forecast being extended to December 2020 and underlying inflation to end 2020 being forecast at 2.25% – that is finally inside the 2–3% band but still below the 2.5% “target”.

In the May SOMP, the Bank stated that “employment growth is expected to be a little above growth in the working age population over the next couple of years and spare capacity is expected to decline.” That “decline” in spare capacity is the dynamic supporting official forecasts that wages growth is expected to reach 3.25% by 2019/20, (Commonwealth Budget May 2018).

The Bank’s forecasts for working aged population growth are 1.7% for 2016 and 1.6% for 2019.

The forecasts for the unemployment rate in the May SOMP of 5.5% by December 2018; 5.25% by December 2019; and 5.25% by June 2020 are expected to be extended to December 2020 at 5.25%.

There is one serious dynamic that could well derail these comfortable jobs forecasts.

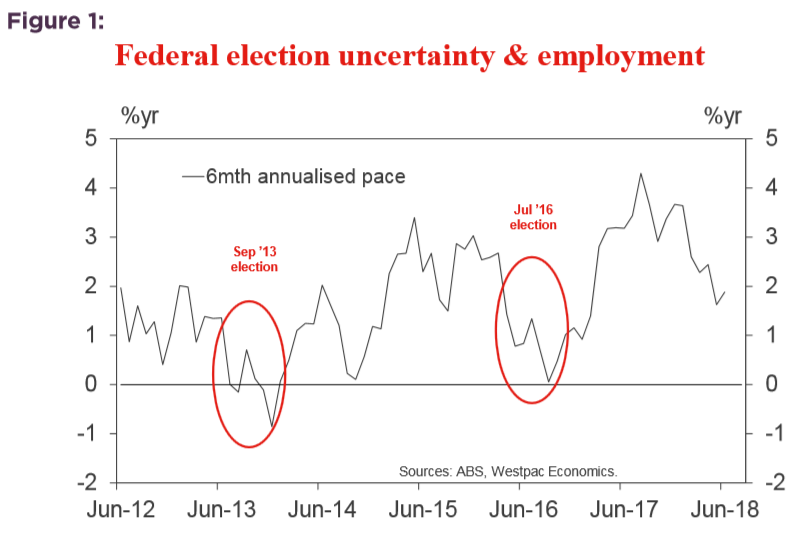

Figure 1, shows the profile of employment growth around the “window” of the last two Federal election campaigns. Note how over the nine month “windows” around election campaigns six month annualised employment growth collapsed – a far cry from the RBA’s assumption of “a little above working age population growth (1.6%)”.

It is true that such a pattern has not been apparent during some previous election campaigns but the evidence from 2013 and 2016 must be disturbing.

With the recent by-election results it now seems certain that there will be no early election. The latest possible date for the next election is May 18 2019 (assuming a simultaneous election for the House of Representatives and a half Senate election).

In the previous two elections (2013 and 2016) the election result was arguably more certain than in 2019. For the 2019 election the polls; the by-election results; and the government’s slim one seat majority all point to considerable political uncertainty.

If businesses acted cautiously during the lead up and the aftermath of the last two Federal elections then we cannot rule out a repeat in 2019. Certainly the Bank’s assumption of a healthy 1.6% – 1.8% jobs market over that period would be challenged.

We do not expect the RBA to incorporate any such effect in their forecasts but recent history around election periods raises significant uncertainty about the sustainability of the Bank’s employment forecasts and hence their expectation of above trend economic growth.