The Foreign Investment Review Board’s 2016-17 annual report, released in May, revealed a sharp contraction in residential real estate applications from foreign buyers, driven by a halving in applications from China:

This was followed in July by NAB’s quarterly property industry survey, which revealed a sharp contraction in demand from foreign buyers:

Especially in the migrant hotspots of NSW and VIC:

Now it has been revealed that the Chinese have become net sellers of US property for the first time in a decade:

Chinese insurers, conglomerates, and other investors have turned net sellers of U.S. commercial real estate for the first time in a decade. They have spent tens of billions of dollars to acquire hotels, office buildings, and vast swaths of empty land to build residential towers.

But Chinese investors sold $1.29 billion worth of U.S. commercial real estate in the second quarter, while purchasing only $126.2 million of property, according to data firm Real Capital Analytics. This marked the first time that these investors were net sellers for a quarter since 2008.

The more than $1 billion in net sales reflects how much the Chinese government’s attitude toward investing overseas has changed in recent months.

Chinese investors began scooping up U.S. real estate a few years ago after Beijing officials loosened restrictions on foreign investment…

Now, the Chinese government has changed course again, cracking down on certain types of outbound investment that include real estate in part to help stabilize the currency. Chinese companies like HNA Group and Greenland Holding Group are unloading prize properties to repay debt and to comply with regulatory and market pressures from home, analysts said.

“I was shocked,” said Jim Costello, senior vice president at Real Capital Analytics. “They really curtailed their buying and stepped up sales.”

There is good reason to believe that Australia could head the same way, with the Chinese becoming net sellers of Australian property.

First, with a falling CNY the Chinese authorities more likely than not will need to implement further capital controls to stem capital outflow:

Last year, China was burning through its huge pile of forex reserves at a rate of $100bn per month and if it continued then that bulwark of CNY stability would have become dangerously depleted.

Second, coming with the flood of foreign buyers came the developers, who launched a land banking and construction boom that succeeded in pricing out even many well-funded local builders. If “Chinese companies like HNA Group and Greenland Holding Group are unloading prize properties [in the USA] to repay debt and to comply with regulatory and market pressures from home”, then the very same thing could happen in Australia.

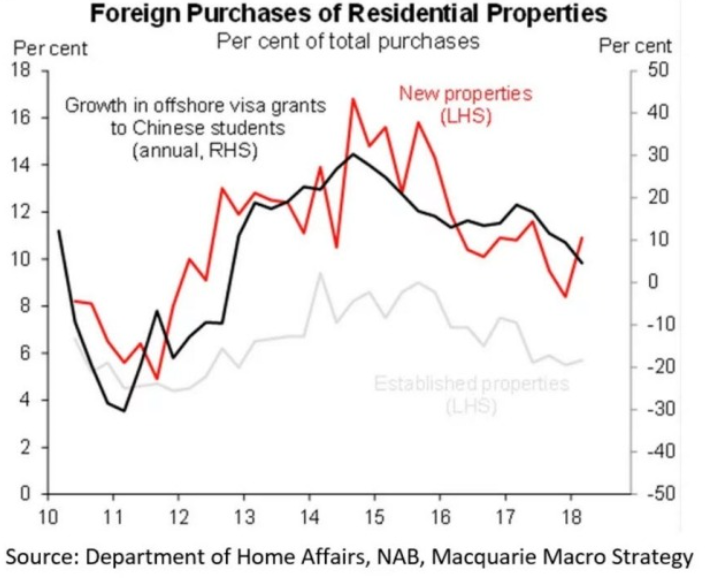

Third, there is increasing pressure in Australia to cut immigration which, if implemented, would obviously impact the Chinese given they are one of Australia’s biggest migrant groups. We know that foreign purchases of Australian property are strongly correlated with Chinese student visas. Therefore, a reduction in visas will most likely result in a reduction in property purchases:

Fourth, while the Australian Government is dragging the chain on implementing anti-money laundering (AML) rules pertaining to real estate gatekeepers, it has promised to progress these rules “over 2018-2019”. Once eventually implemented, Chinese buyers could be hit particularly hard, given they are the prime source of illicit funds according to the Financial Action Taskforce.

Finally, the Australia-China relationship has soured, which could lead to the Chinese shunning Australian property in favour of other destinations, just as it has done in the US. This could take the form of punitive action by the Communist Party or just the Chinese public voting with their wallets.

Even if the Chinese do not end up as net sellers of Australian property, as they have in the US, there is a very good likelihood that their demand will soften further.

unconventionaleconomist@hotmail.com