DXY firmed last night:

AUD bounced anyway with risk:

Gold is still stuck:

Oil was firm:

Base metals too:

Miners jumped:

Em stocks improved:

But EM junk sent another warning:

Treasuries were bashed:

And bunds:

Stocks popped:

Westpac has the wrap:

Economic Wrap

US homebuilder sentiment was unchanged in September, the National Association of Homebuilder’s sentiment index coming in at 67; below the 74.0 cycle peak late last year but still historically elevated levels consistent with decent momentum in housing construction.

China announced retaliatory tariffs on USD60bn of goods imported from the US, to take effect next week 24 September. A levy of 5% will be applied to 1600 products including aircraft, computers and textiles while a 10% levy will be applied to more than 3500 items including chemicals, meat, wheat, wine and LNG. The US administration earlier said they will pursue additional tariffs on USD267bn of Chinese imports if China retaliated against American farmers and industry and President Trump threatened additional tariffs via twitter after China’s retaliatory actions but no formal announcement has been made.

The GDT dairy auction saw prices fall 1.3% overall, with whole milk powder down 1.8%, skimmed milk powder down 1.1%, and butter down 0.1%. The result was not as weak as futures markets had earlier priced.

Event Risk

NZ consumer confidence (Westpac) for Q3 will be watched for any signs of Q2’s modest weakness accelerating. Q2 current account balance is expected to slip from -2.8% to -2.9% GDP (Westpac expects -2.8%). The current account deficit remains small relative to history, and current levels support a further improvement in New Zealand’s net overseas liabilities position.

In Australia we have the Westpac Leading Index, its growth rate having slowed materially since the start of the year, peaking at +1.31% in February. There’s also a speech from RBA’s Kent on “Money Creation” in Sydney.

In the Eurozone we have the July current account and a speech from ECB’s Draghi.

US data is second-tier – housing starts and the current account.

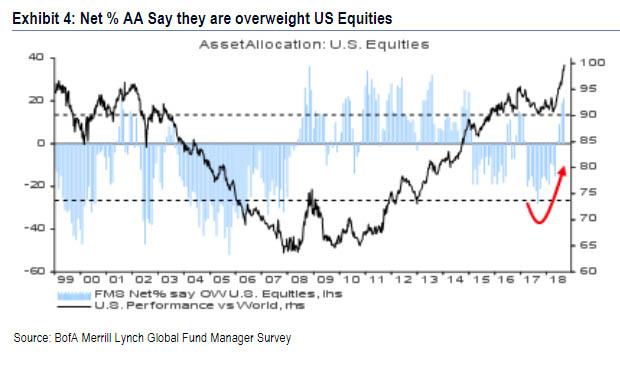

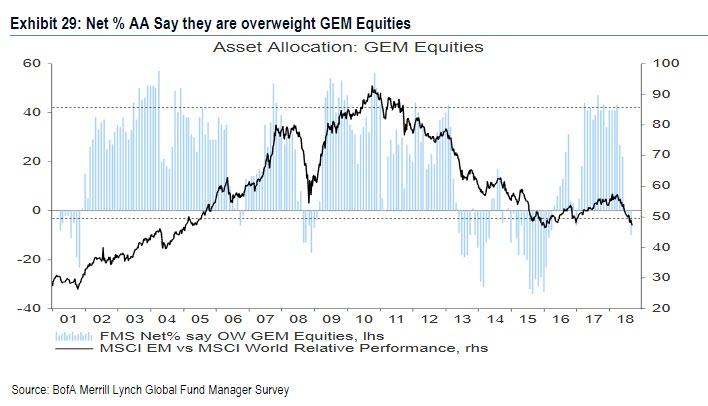

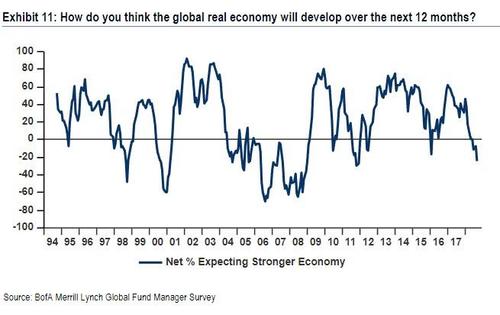

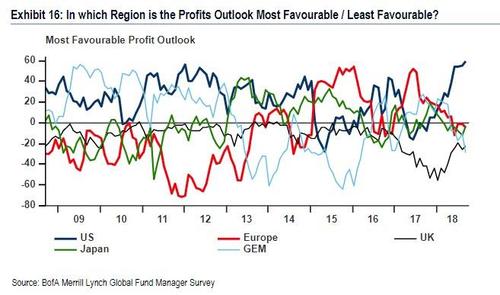

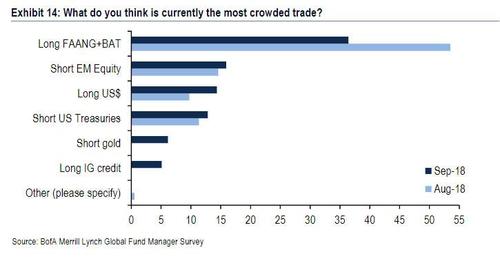

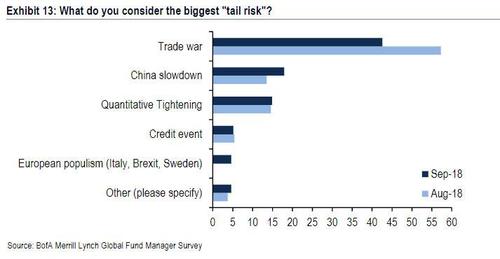

BofAML offered its monthly fundie survey. The investment world has now aligned completely with the MB Fund. Long US equities:

Short EM equities:

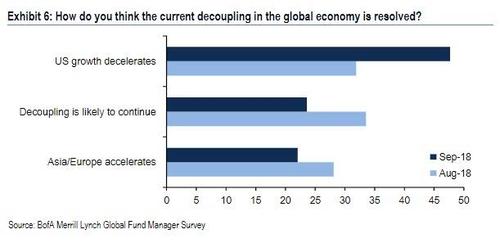

All about US decoupling (or “reverse decoupling” as we’ve called it, versus the 2007 experience):

Decoupling to wane:

Growth to slow:

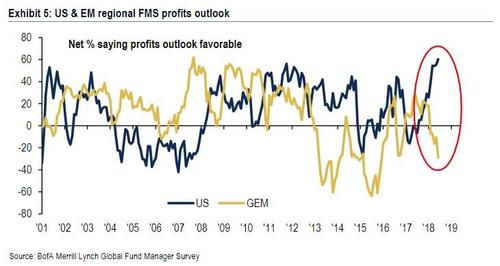

US EPS still off the chart:

FAANG and US long trades:

Risk is a big yawn:

I feel quite uncomfortable having the funds management world piled in behind me. Obviously positioning for this in advance is why we have delivered unusually good late cycle returns. The question is, with markets now long all of our positions, when will it reverse?

I still can’t see it as imminent. China is still set to slow before firming next year on easier credit. There is more juice in the US tax cut EPS boom yet. The trade war lifts both positions via slowing China/commodities and rising US inflation. There is still plenty of time for Trump to push for more stimulus post mid-terms.

There may be a rising risk of volatility as markets sort through the cross-currents and US growth comes under question but if the USD does begin to weaken on the prospects of a Fed pause then, equally, US stocks will likely be supported more than the AUD rises. The apposite chart remains this one:

Given it is late cycle and nobody knows how late, we remain conservatively positioned at only 60% equities but unless or until the US EPS boom rolls over we will stay that way.