Another reason to worry about Chinese commodity demand

Advertisement

There are reasons to be optimistic. More infrastructure is coming. But there are other, more powerful forces, that make it a worry. We know steel demand is being dented by the manufacturing recession and weak car demand. But the big one is realty. It always is, constituting 30-40% of steel consumption. This is a problem in the year ahead with sales already falling and starts tracking them lower:

Note that the weakest periods of bulk commodity prices have always coincided with real estate weakness.

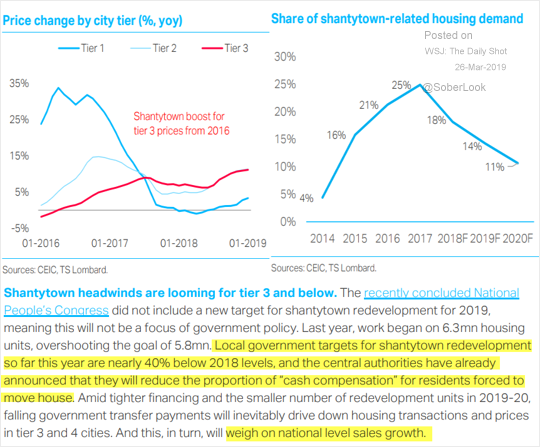

Then there is this from T.S. Lombard:

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.